Fitted values and residuals

Forecasting in R

Rob J. Hyndman

Professor of Statistics at Monash University

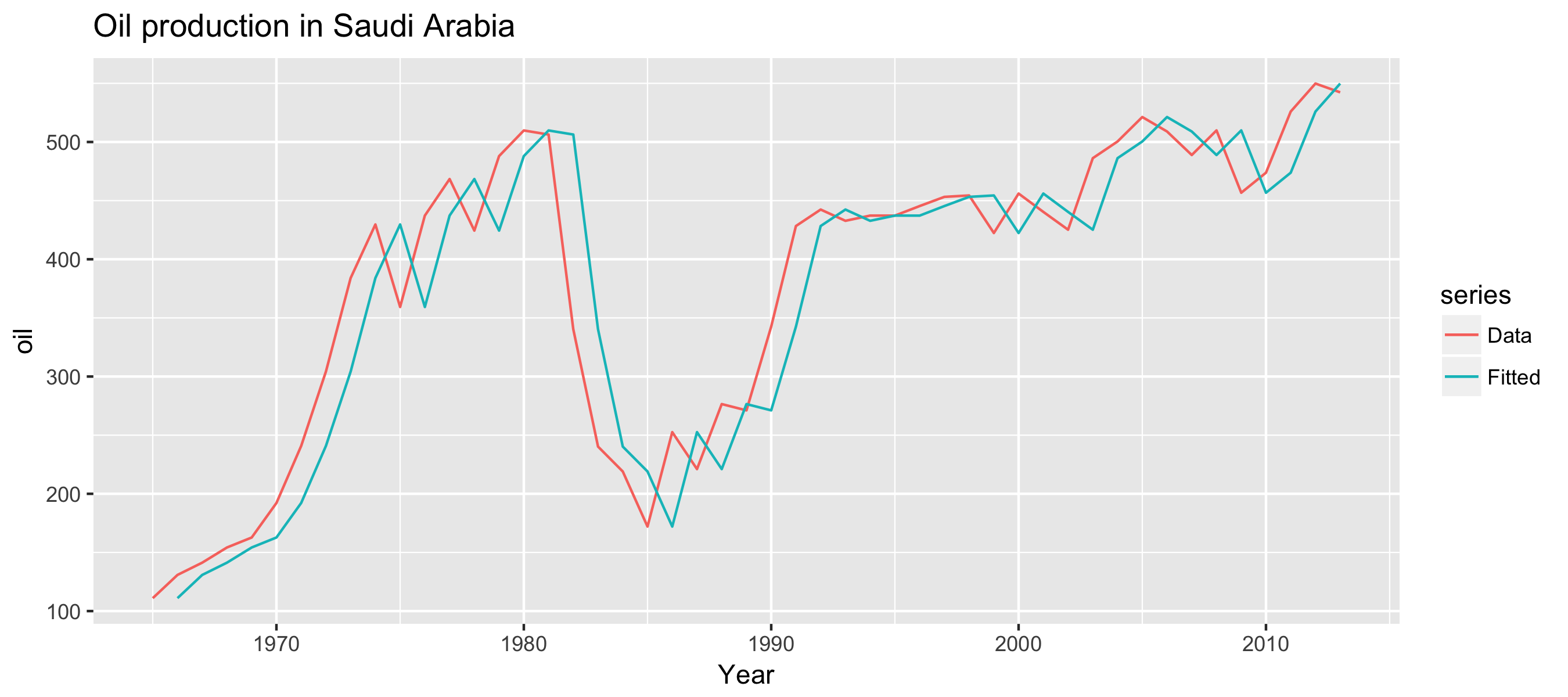

Example: oil production

fc <- naive(oil)

autoplot(oil, series = "Data") + xlab("Year") +

autolayer(fitted(fc), series = "Fitted") +

ggtitle("Oil production in Saudi Arabia")

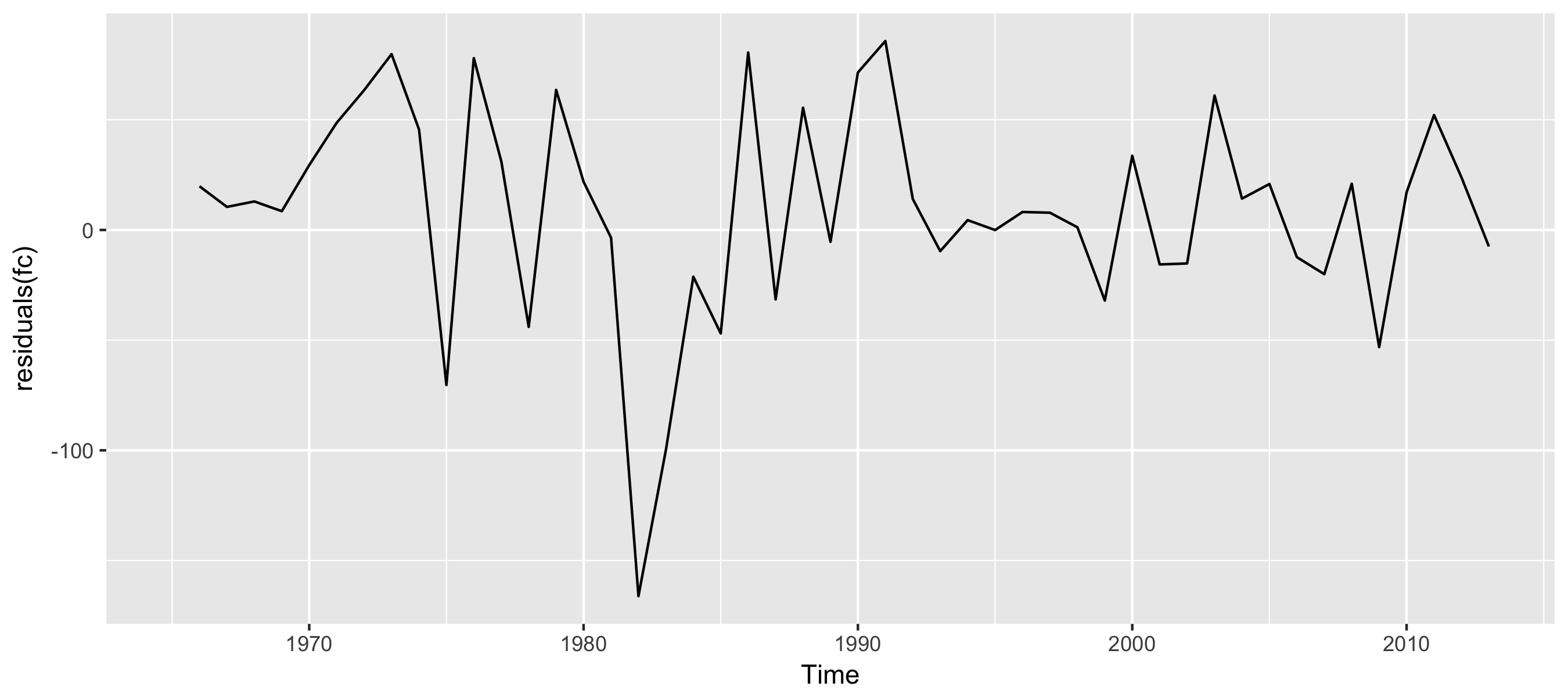

Example: oil production

autoplot(residuals(fc))

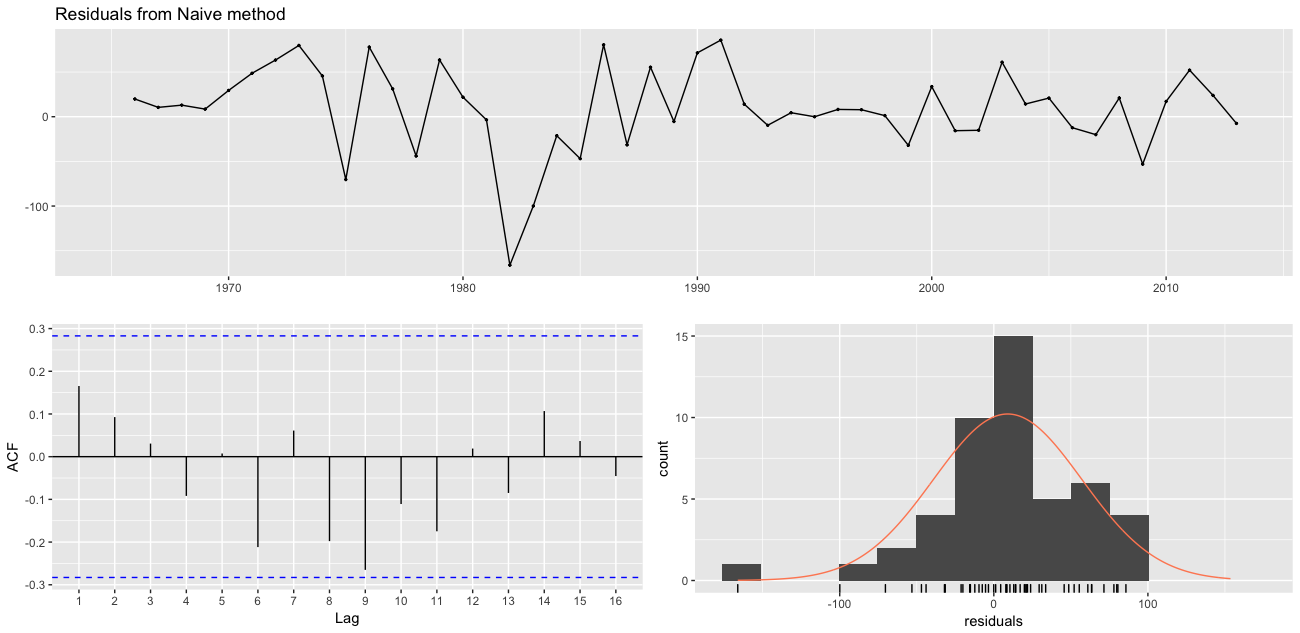

checkresiduals()

checkresiduals(fc)

Ljung-Box test

data: residuals

Q* = 12.59, df = 10, p-value = 0.2475

Model df: 0. Total lags used: 10