Dynamic harmonic regression

Forecasting in R

Rob J. Hyndman

Professor of Statistics at Monash University

Dynamic harmonic regression

Dynamic harmonic regression

$m =$ seasonal period

Every periodic function can be approximated by sums of sin and cos terms for large enough K

Regression coefficients: $\alpha_k$ and $\gamma_k$

$e_t$ can be modeled as a non-seasonal ARIMA process

Assumes seasonal pattern is unchanging

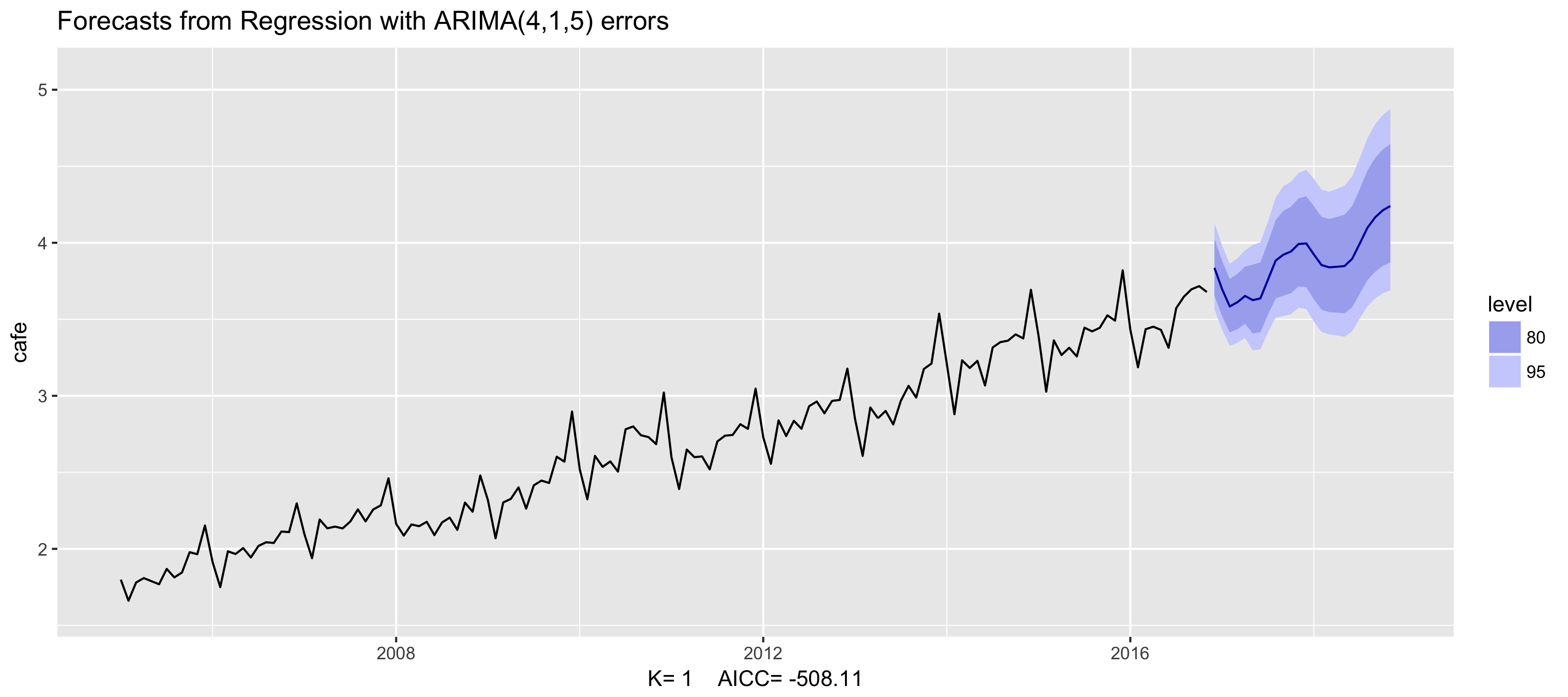

Example: Australian cafe expenditure

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 1),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 1, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

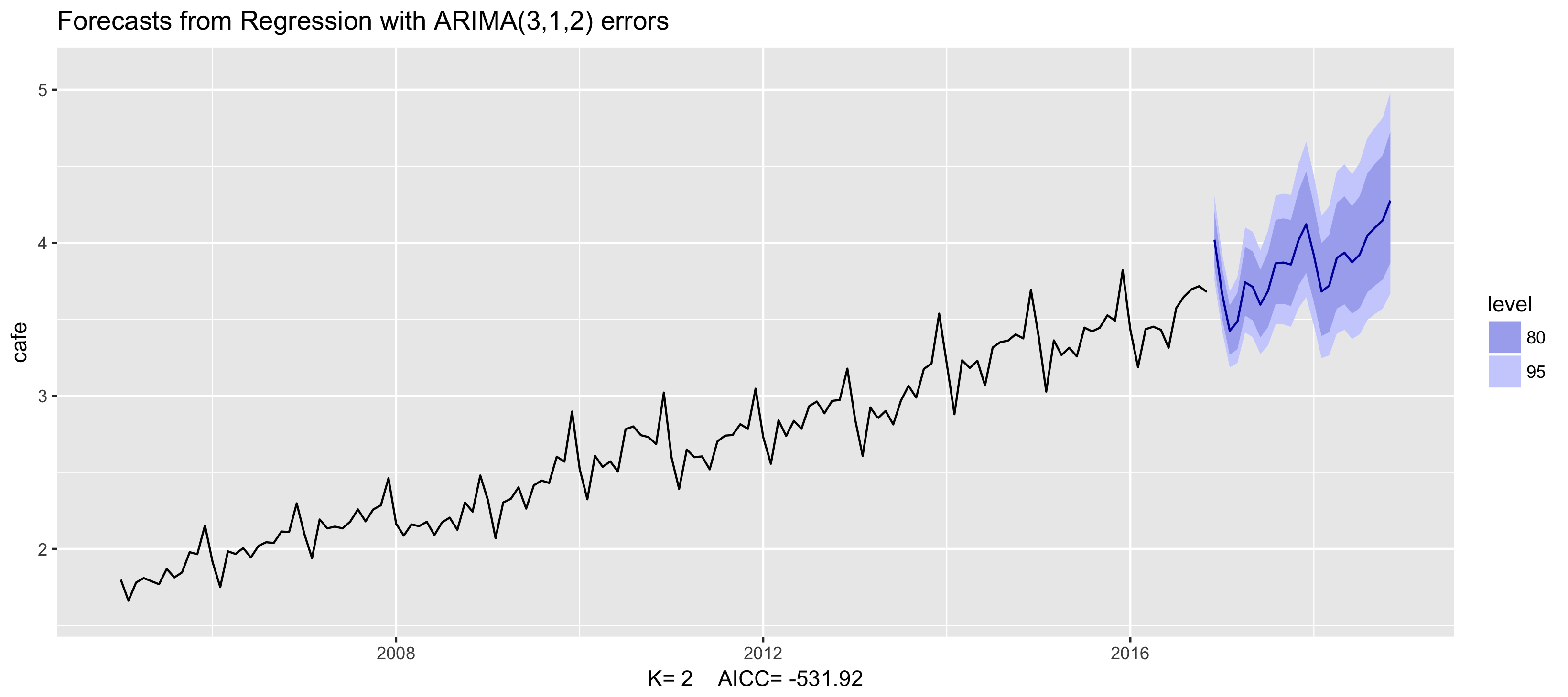

Example: Australian cafe expenditure

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 2),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 2, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

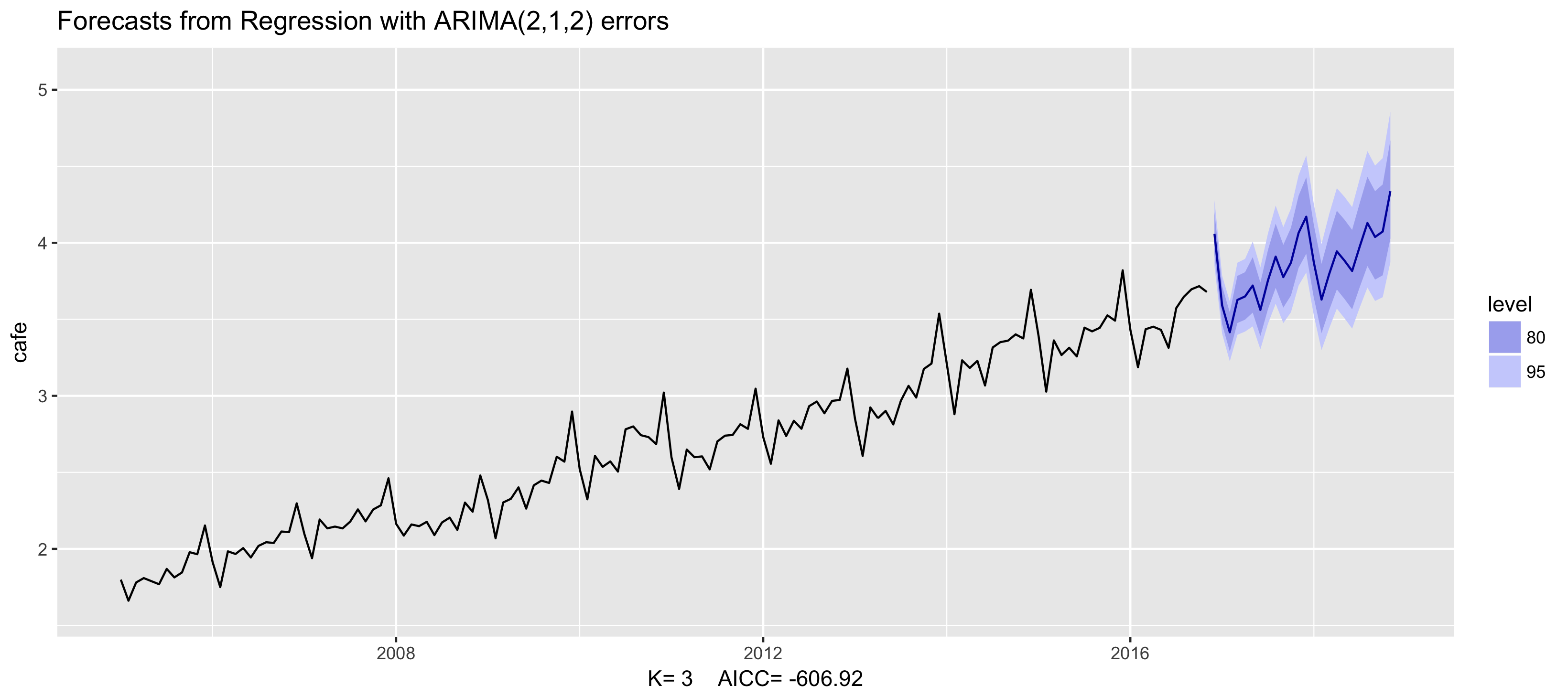

Example: Australian cafe expenditure

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 3),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 3, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

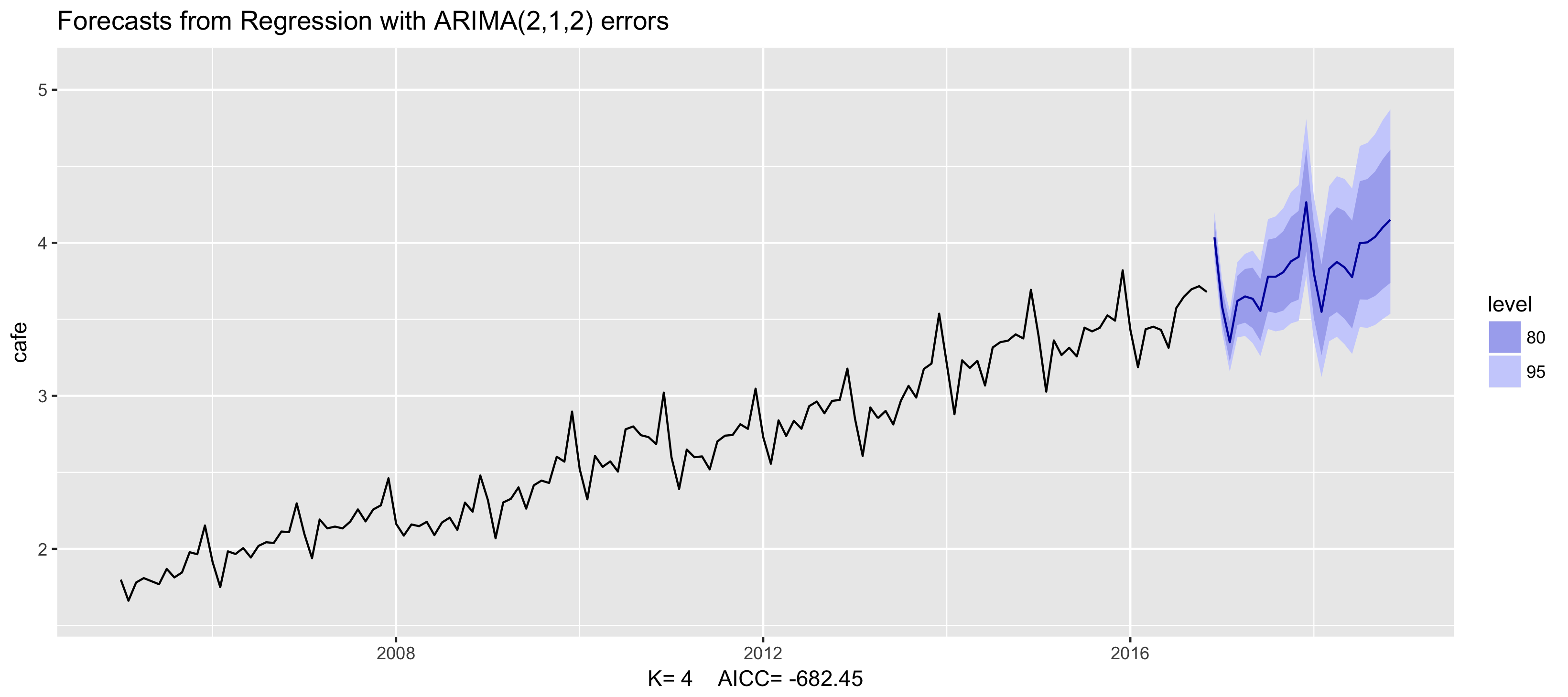

Example: Australian cafe expenditure

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 4),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 4, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

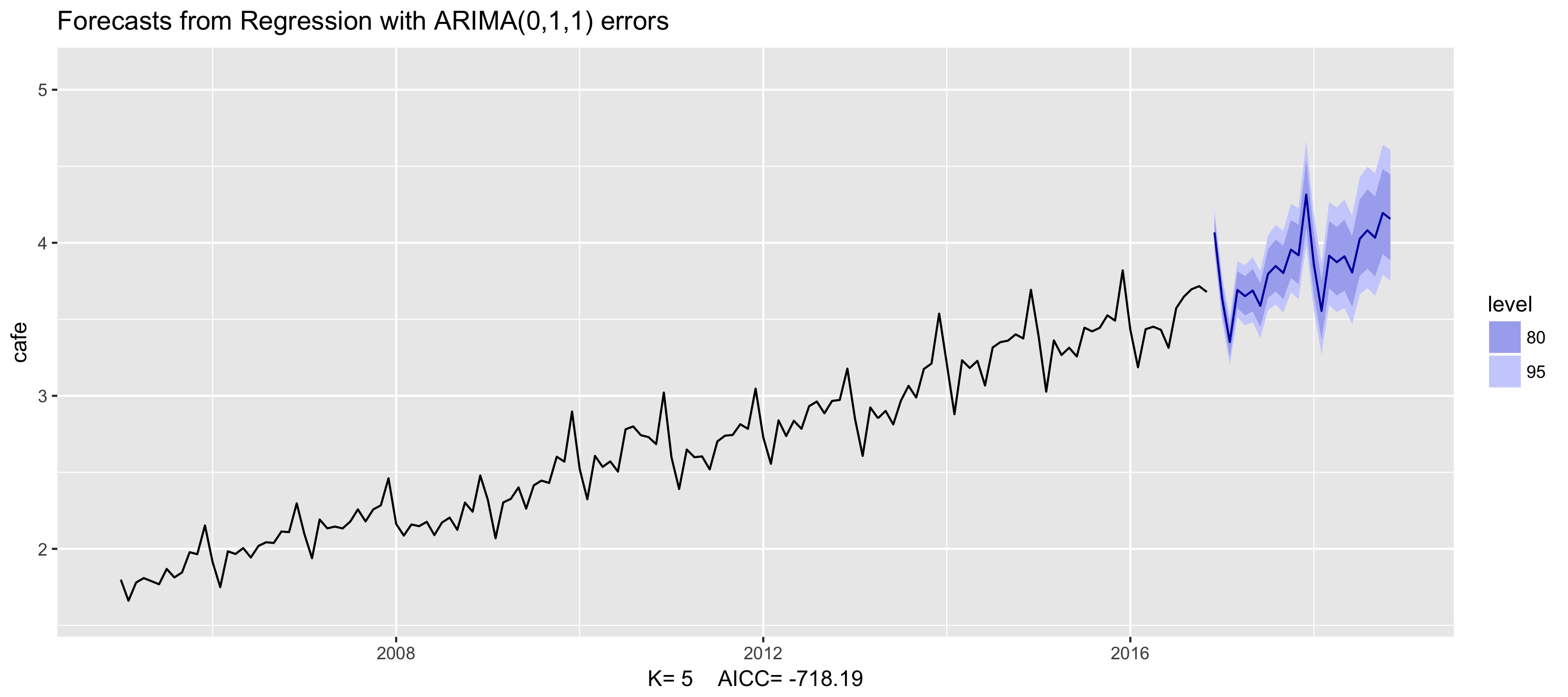

Example: Australian cafe expenditure

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 5),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 5, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

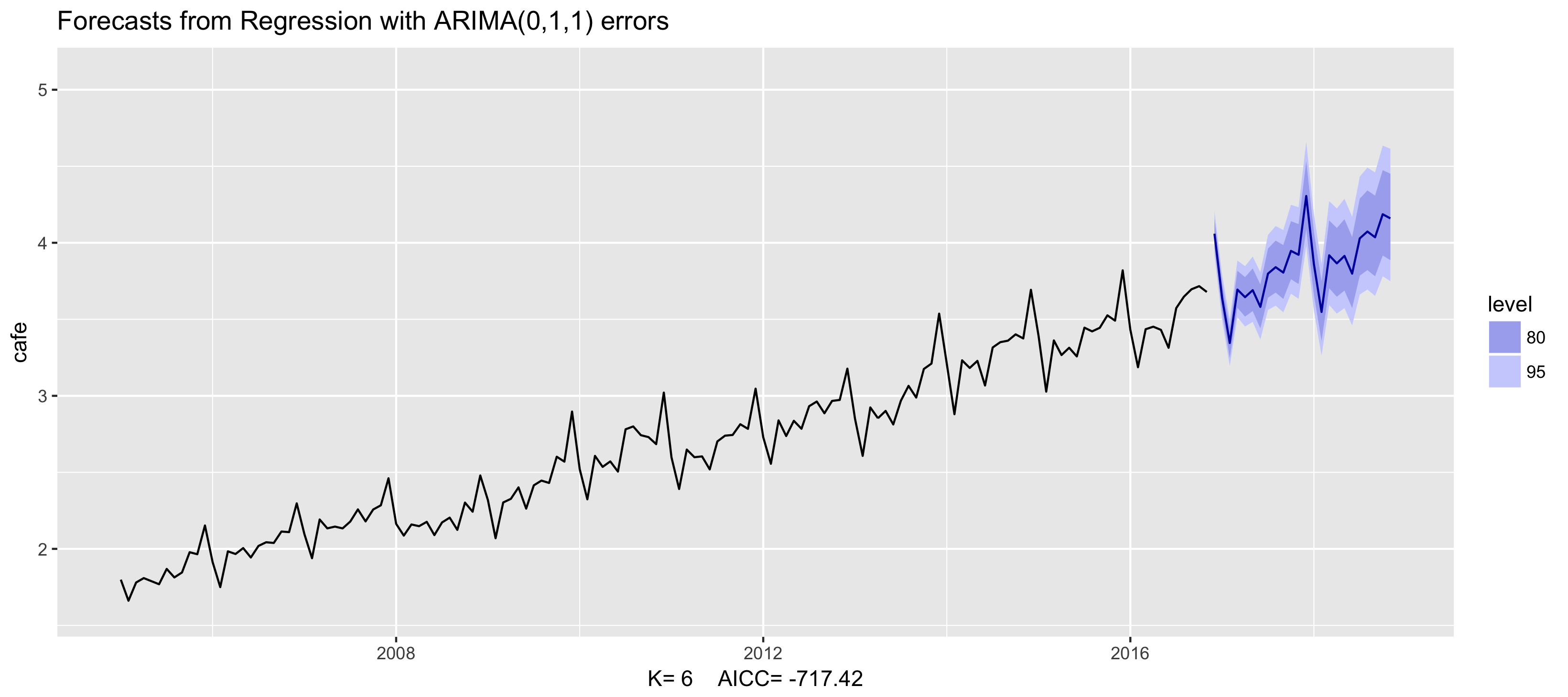

Example: Australian cafe expenditure

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 6),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 6, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

Dynamic harmonic regression

- Other predictor variables can be added as well: $x_{t,1},...,x_{t,r}$

- Choose K to minimize the $AIC_c$

- K can not be more than m/2

- This is particularly useful for weekly data, daily data and sub-daily data.