Seasonal ARIMA models

Forecasting in R

Rob J. Hyndman

Professor of Statistics at Monash University

ARIMA models

- d = Number of lag-1 differences

- p = Number of ordinary AR lags:

- q = Number of ordinary MA lags:

ARIMA models

- d = Number of lag-1 differences

- p = Number of ordinary AR lags:

- q = Number of ordinary MA lags:

ARIMA models

- d = Number of lag-1 differences

- p = Number of ordinary AR lags: $\ y_{t-1}, y_{t-2},...,y_{t-p}$

- q = Number of ordinary MA lags: $\ \epsilon_{t-1}, \epsilon_{t-2},...,\epsilon_{t-q}$

- D = Number of seasonal differences

- P = Number of seasonal AR lags: $\ y_{t-m}, y_{t-2m},...,y_{t-Pm}$

- Q = Number of seasonal MA lags:$\ \epsilon_{t-m}, \epsilon_{t-2m},...,\epsilon_{t-Qm}$

- m = Number of observations per year

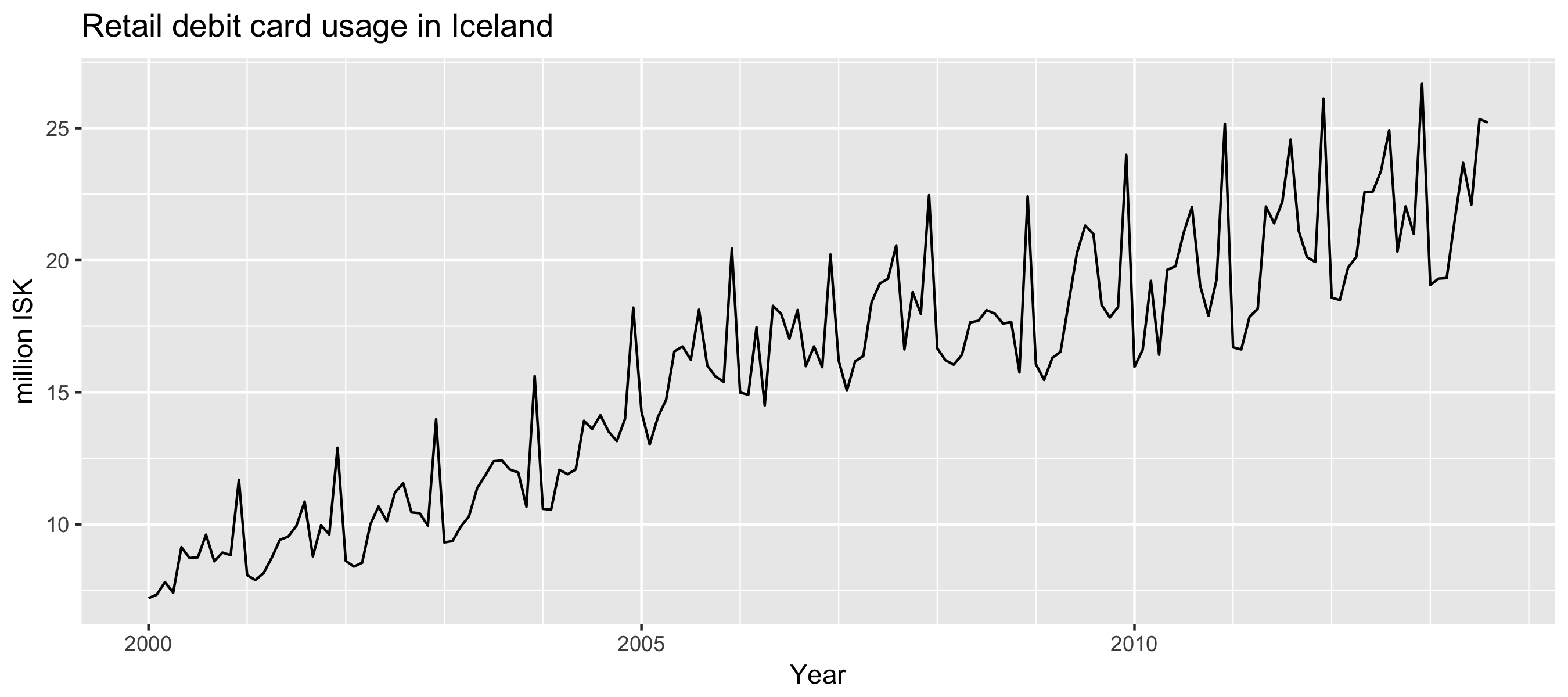

Example: Monthly retail debit card usage in Iceland

autoplot(debitcards) +

xlab("Year") + ylab("million ISK") +

ggtitle("Retail debit card usage in Iceland")

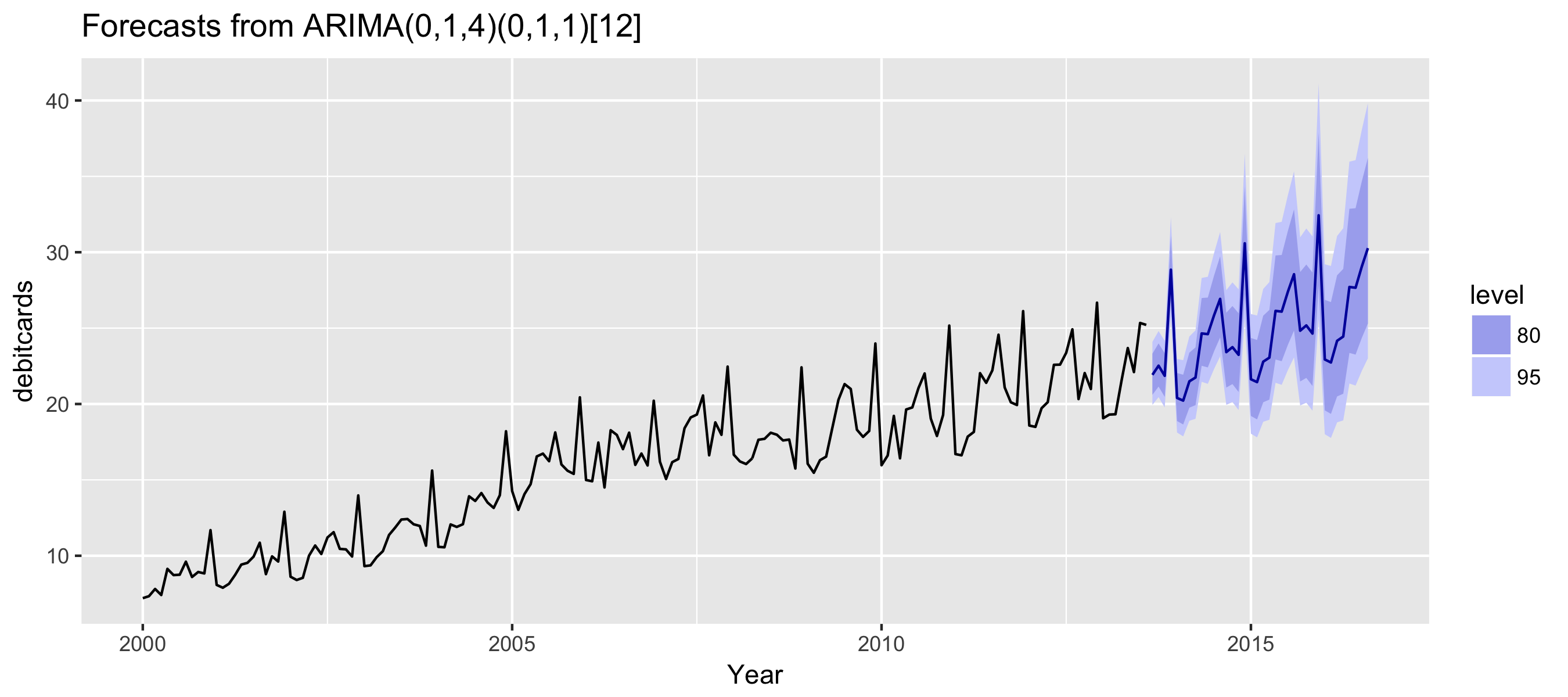

Example: Monthly retail debit card usage in Iceland

fit %>%

forecast(h = 36) %>%

autoplot() + xlab("Year")