Training and test sets

Forecasting in R

Rob J. Hyndman

Professor of Statistics at Monash University

Training and test sets

Training and test sets

Training and test sets

- The test set must not be used for any aspect of calculating forecasts

- Build forecasts using training set

- A model which fits the training data well will not necessarily forecast well

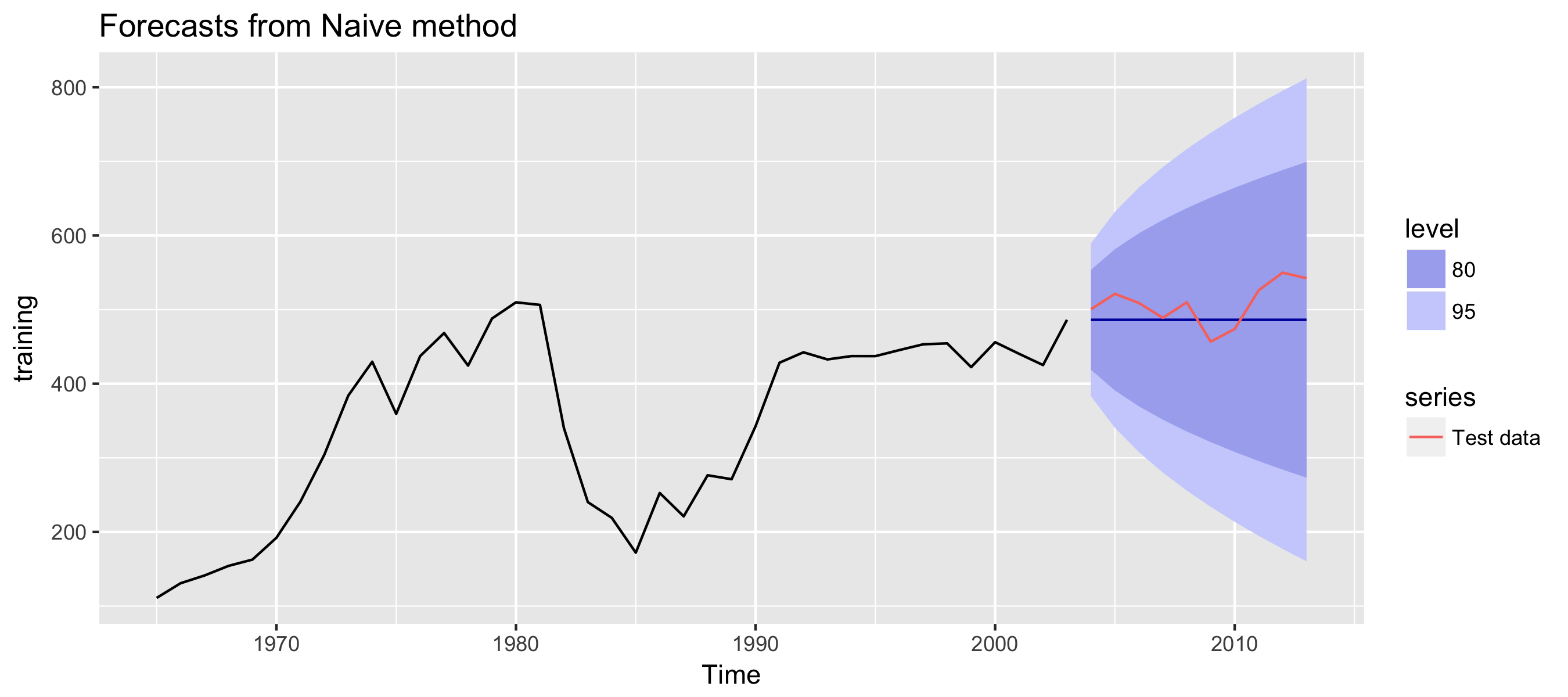

Example: Saudi Arabian oil production

training <- window(oil, end = 2003)

test <- window(oil, start = 2004)

fc <- naive(training, h = 10)

autoplot(fc) + autolayer(test, series = "Test data")