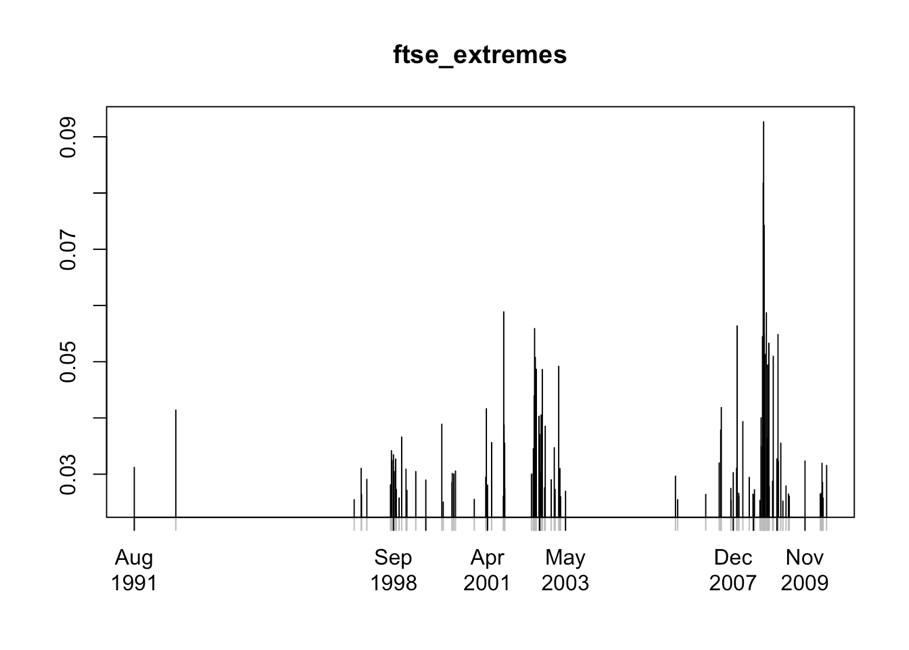

Looking at the extremes in volatile return series

Quantitative Risk Management in R

Alexander McNeil

Professor, University of York

Plotting the extremes values

plot(ftse_extremes, type = "h", auto.grid = FALSE)

Quantitative Risk Management in R

Alexander McNeil

Professor, University of York

plot(ftse_extremes, type = "h", auto.grid = FALSE)