Estimating serial correlations

Quantitative Risk Management in R

Alexander McNeil

Professor, University of York

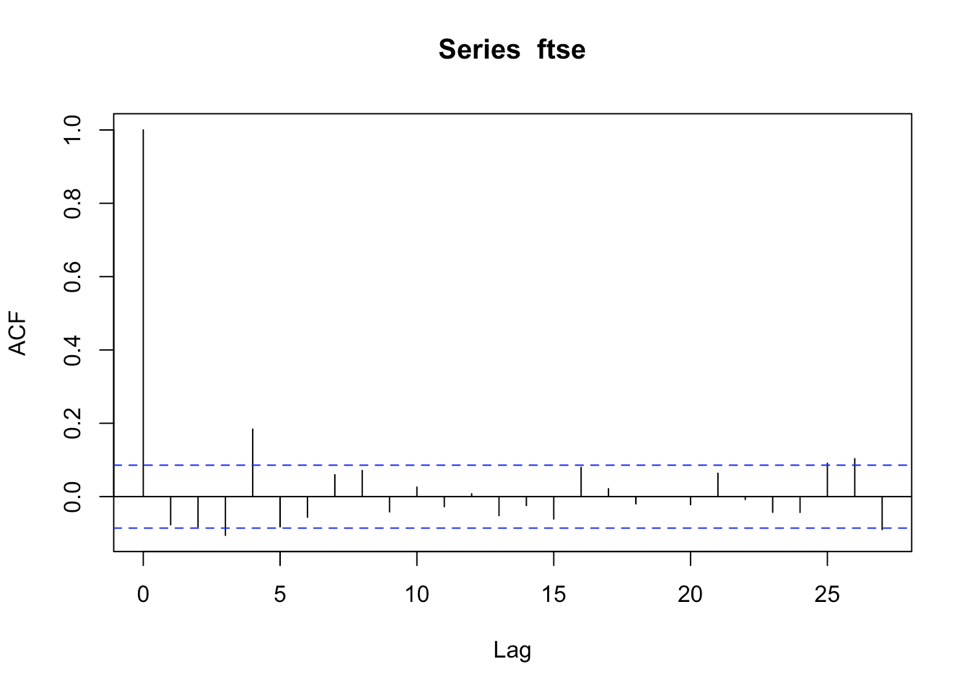

The sample acf plot or correlogram

acf(ftse)

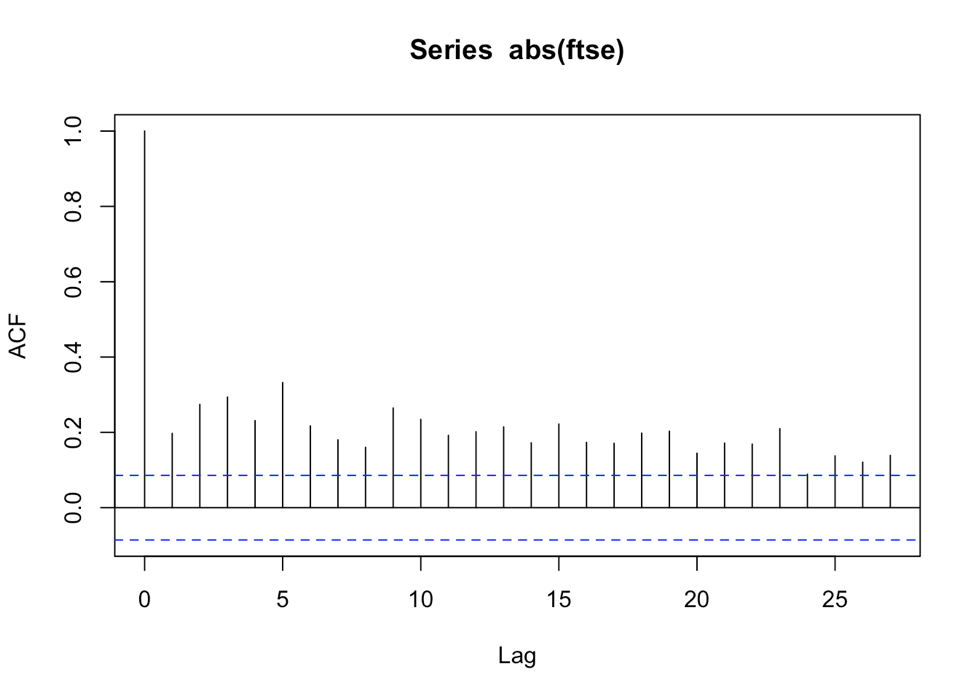

The sample acf plot or correlogram

acf(abs(ftse))

Quantitative Risk Management in R

Alexander McNeil

Professor, University of York

acf(ftse)

acf(abs(ftse))