Value-at-risk and expected shortfall

Quantitative Risk Management in R

Alexander McNeil

Professor, University of York

Value-at-risk (VaR)

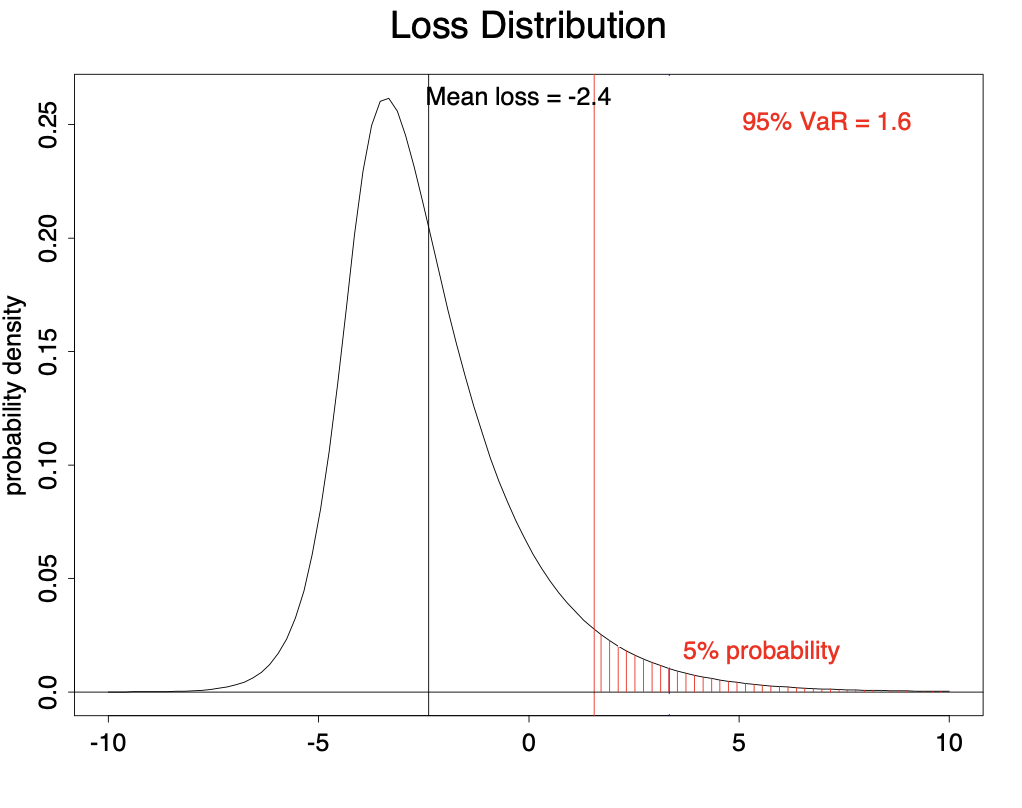

Consider the distribution of losses over a fixed time period (day, week, etc.)

$\alpha$-VaR is the $\alpha$-

quantile

of the loss distribution

$\alpha$ known as

confidence level

(e.g. 95%, 99%)

Should lose no more than $\alpha$-VaR with probability $\alpha$

95% VaR illustrated

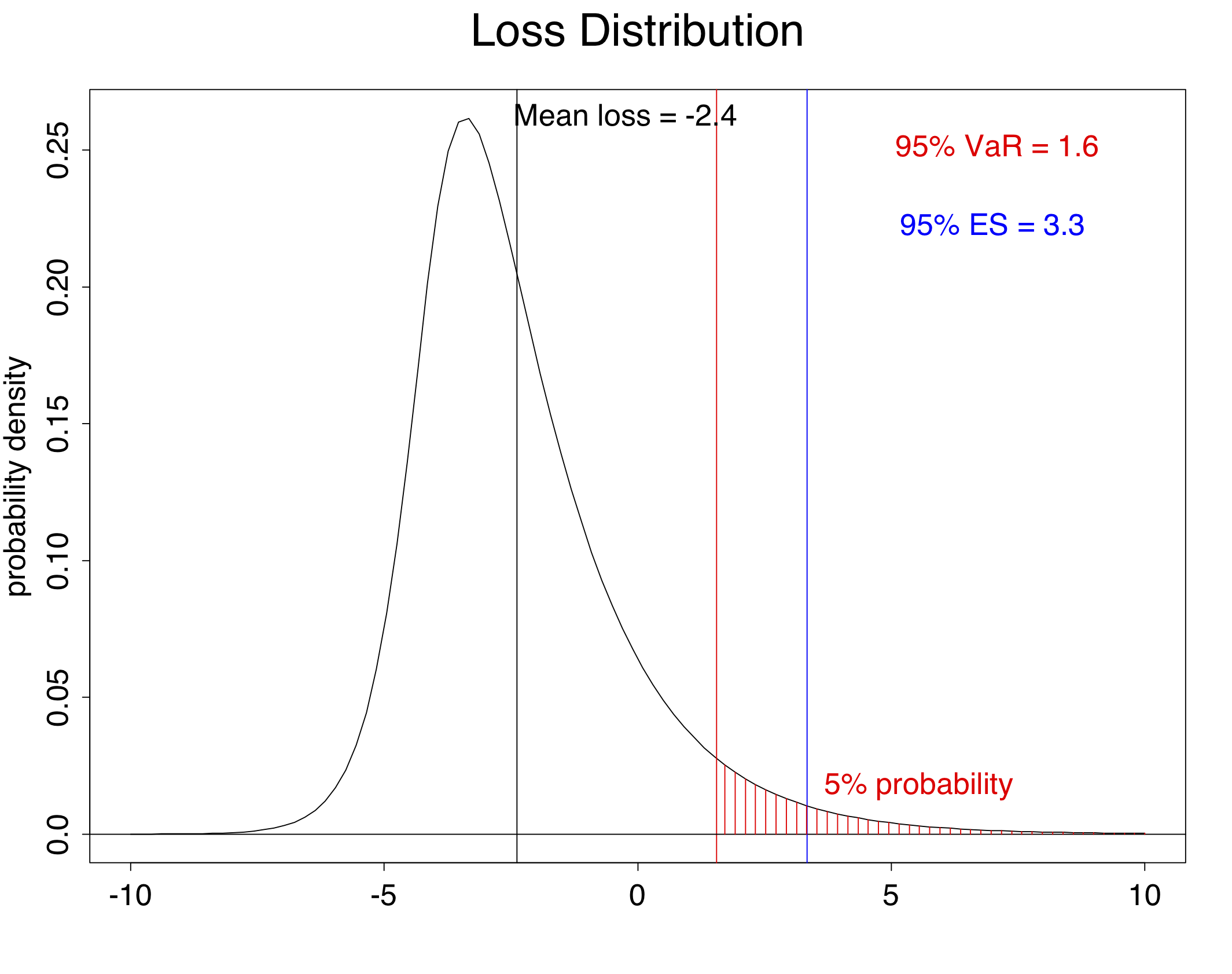

Expected shortfall (ES)

Increasingly important in banking regulation

Tail VaR (TVaR), conditional VaR (CVaR) or

expected shortfall

(ES)

$\alpha$-ES is expected loss given that loss exceeds $\alpha$-VaR

Expectation of tail of distribution

95% of ES illustrated

Let's practice!

Quantitative Risk Management in R

Preparing Video For Download...