Quantitative Risk Management in R

Alexander McNeil

Instructor

K <- 50 T <- 2 t <- 0 S <- 40 r <- 0.005 sigma <- 0.25 Black_Scholes(t, S, r, sigma, K, T, "call")

K <- 50

T <- 2

t <- 0

S <- 40

r <- 0.005

sigma <- 0.25

Black_Scholes(t, S, r, sigma, K, T, "call")

2.619183

Black_Scholes(t, S, r, sigma*1.2, K, T, "call")

3.677901

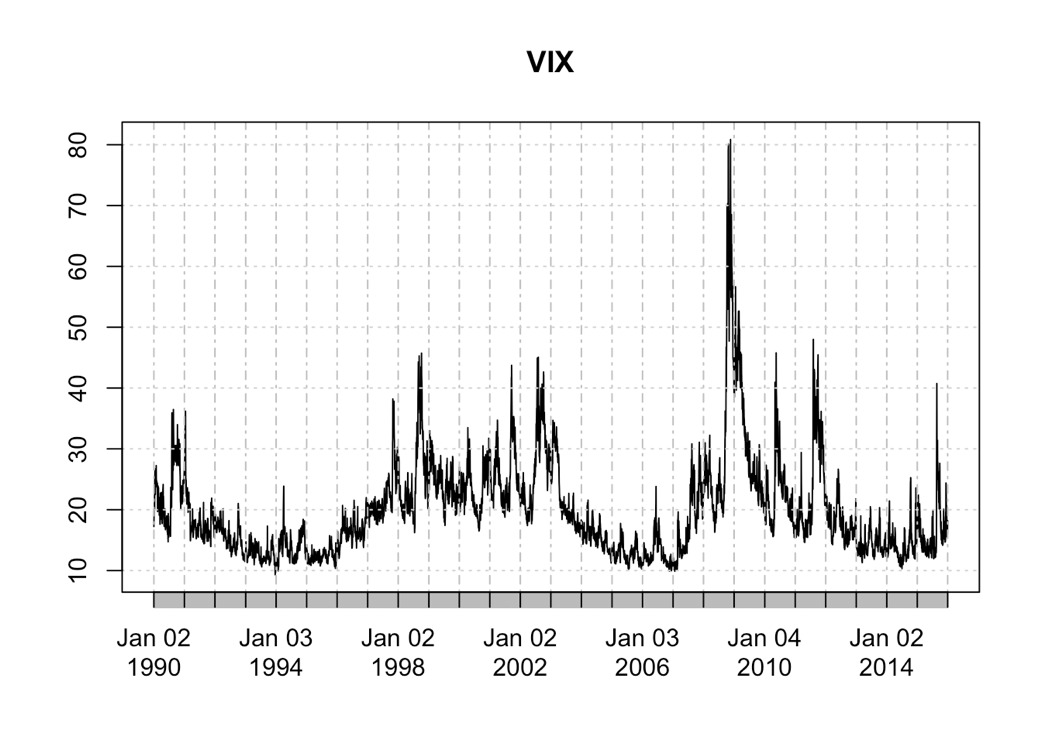

plot(VIX)