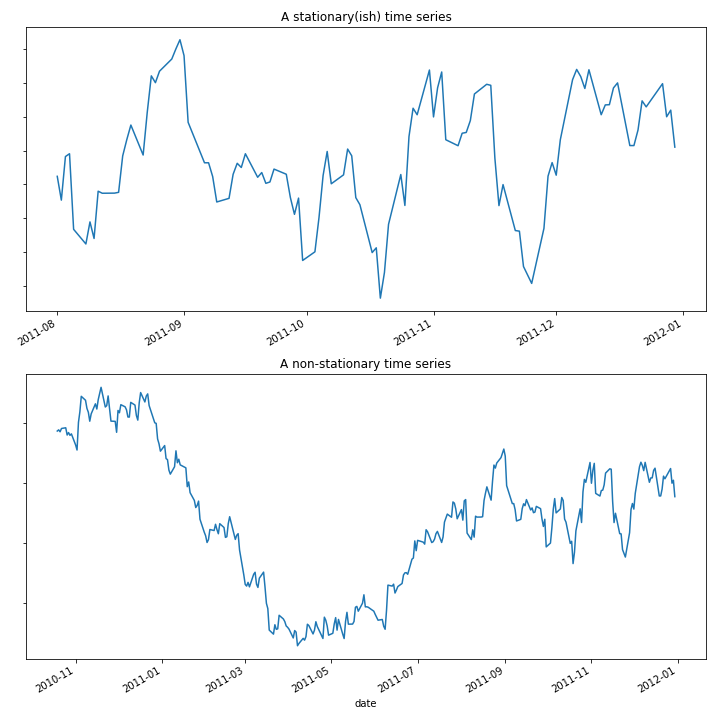

Stationarity and stability

Machine Learning for Time Series Data in Python

Chris Holdgraf

Fellow, Berkeley Institute for Data Science

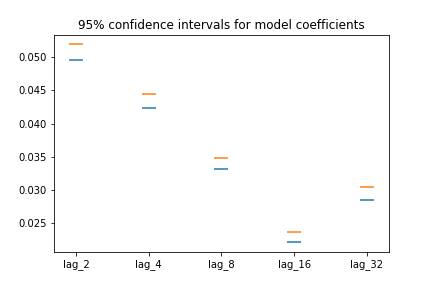

Plotting the bootstrapped coefficients

fig, ax = plt.subplots()

ax.scatter(many_shifts.columns, percentiles[0], marker='_', s=200)

ax.scatter(many_shifts.columns, percentiles[1], marker='_', s=200)

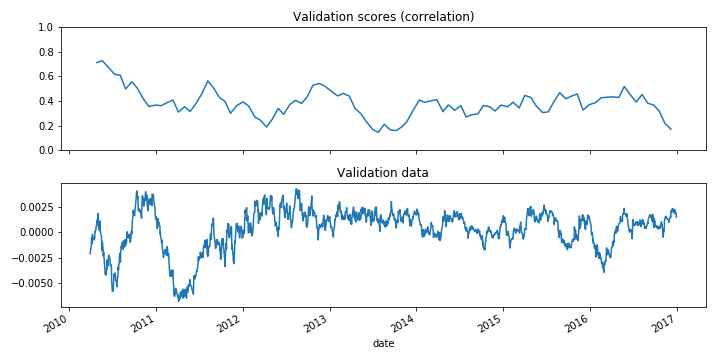

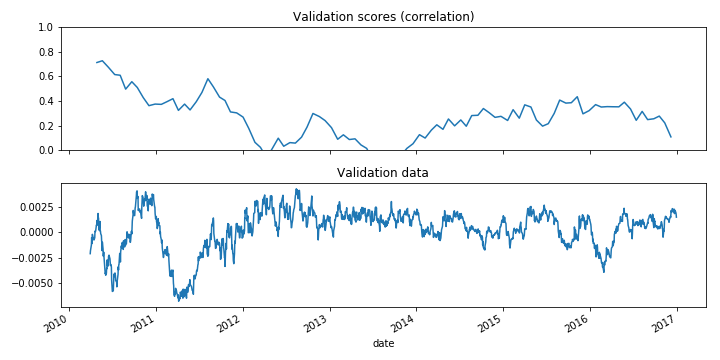

Visualizing model scores

Non-stationary signals