Simple Linear Regressions

Time Series Analysis in Python

Rob Reider

Adjunct Professor, NYU-Courant Consultant, Quantopian

What is a Regression?

- Ordinary Least Squares (OLS)

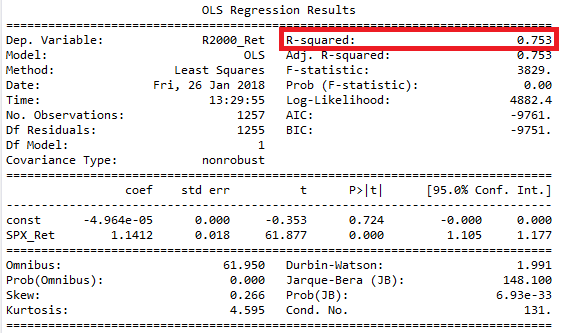

Regression Example (continued)

- Regression output

- Intercept in

results.params[0] - Slope in

results.params[1]

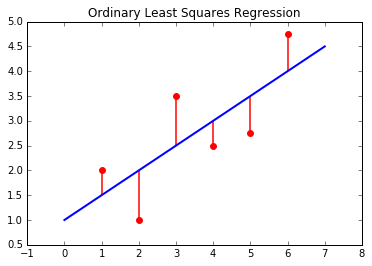

Regression Example (continued)

- Regression output