Árvores impulsionadas (Gradient Boosting) com XGBoost

Modelagem de Risco de Crédito em Python

Michael Crabtree

Data Scientist, Ford Motor Company

Árvores de decisão

- Gera previsões parecidas com regressão logística

- Não é estruturada como uma regressão

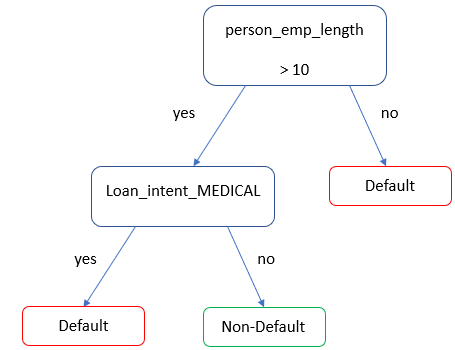

Árvores para status do empréstimo

- Árvore simples para prever probabilidade de default em

loan_status

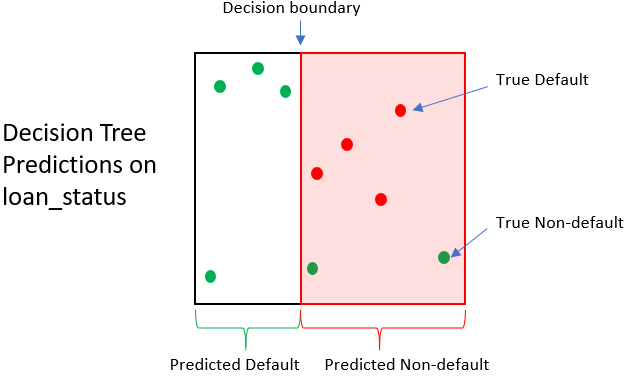

Impacto da árvore de decisão

| Empréstimo | Status real | Status previsto | Valor de quitação | Valor de venda | Ganho/Perda |

|---|---|---|---|---|---|

| 1 | 0 | 1 | $1.500 | $250 | -$1.250 |

| 2 | 0 | 1 | $1.200 | $250 | -$950 |

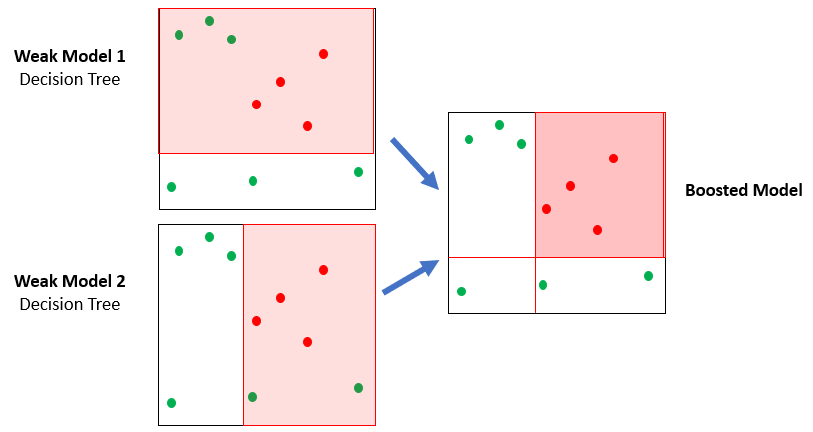

Uma floresta de árvores

- XGBoost usa muitas árvores simples (ensemble)

- Cada árvore é só um pouco melhor que cara ou coroa