Desbalanceamento em dados de empréstimos

Modelagem de Risco de Crédito em Python

Michael Crabtree

Data Scientist, Ford Motor Company

Função de perda do modelo

- Gradient Boosted Trees no

xgboostusam log-loss como função de perda- O objetivo é minimizá-la

| Status real do empréstimo | Prob. prevista | Log-loss |

|---|---|---|

| 1 | 0.1 | 2.3 |

| 0 | 0.9 | 2.3 |

- Um default previsto errado tem impacto financeiro pior

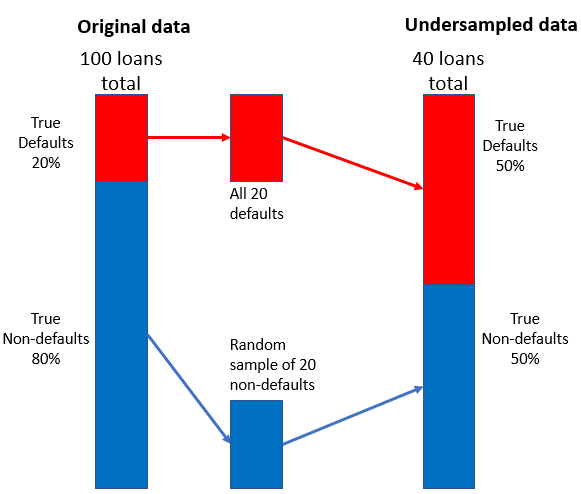

Estratégia de subamostragem

- Combine uma amostra aleatória menor de não inadimplentes com os inadimplentes