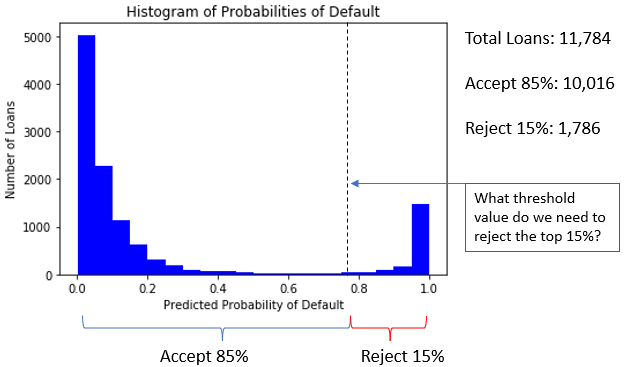

Taxas de aceitação de crédito

Modelagem de Risco de Crédito em Python

Michael Crabtree

Data Scientist, Ford Motor Company

Entendendo a taxa de aceitação

- Exemplo: aceitar 85% dos empréstimos com menor

prob_default

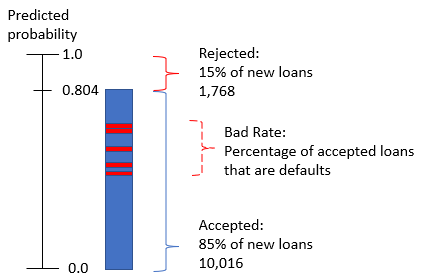

Taxa de inadimplência

- Mesmo com um limiar calculado, alguns empréstimos aceitos vão inadimplir

- São empréstimos com

prob_defaultperto da faixa onde o modelo não está bem calibrado

Cálculo da taxa de inadimplência

#Calculate the bad rate

np.sum(accepted_loans['true_loan_status']) / accepted_loans['true_loan_status'].count()

- Se não inadimplente é

0e inadimplente é1, entãosum()é a contagem de inadimplentes - O

.count()de uma única coluna é igual ao número de linhas do data frame