Validação cruzada para modelos de crédito

Modelagem de Risco de Crédito em Python

Michael Crabtree

Data Scientist, Ford Motor Company

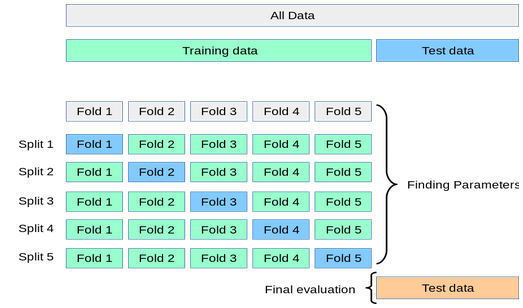

Como funciona a validação cruzada

- Processa partes do treino (chamadas folds) e testa contra a parte não usada

- Teste final no conjunto de teste real

1 https://scikit-learn.org/stable/modules/cross_validation.html

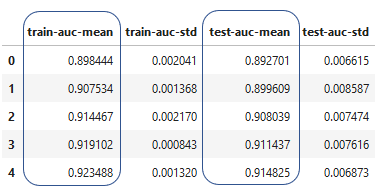

Resultados da validação cruzada

- Cria um data frame com os valores da validação cruzada