Risk factors and the financial crisis

Quantitative Risk Management in Python

Jamsheed Shorish

Computational Economist

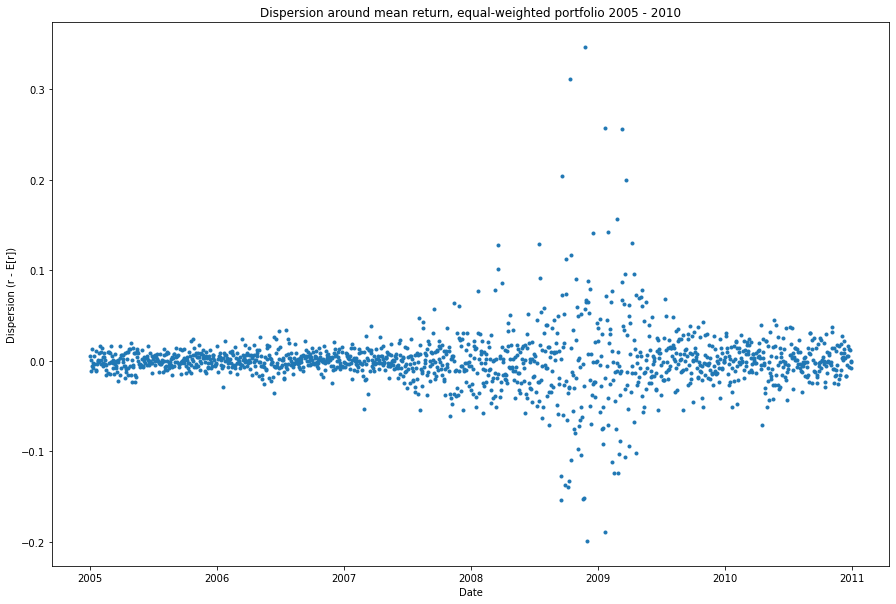

Risk factors

Systematic risk

Idiosyncratic risk

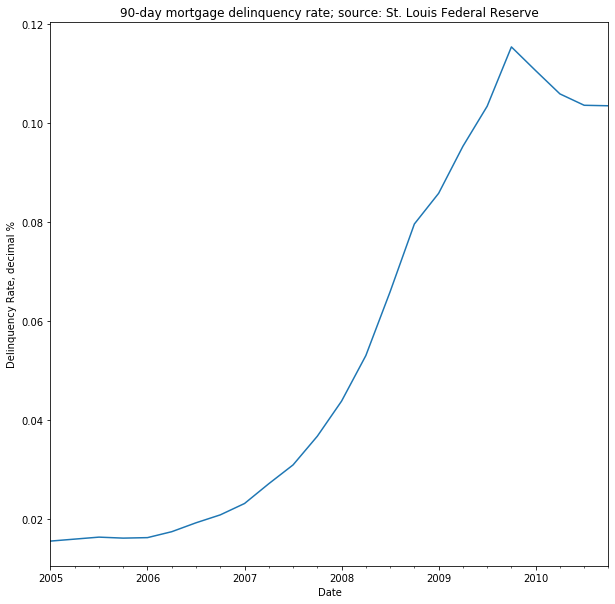

Crisis risk factor: mortgage-backed securities

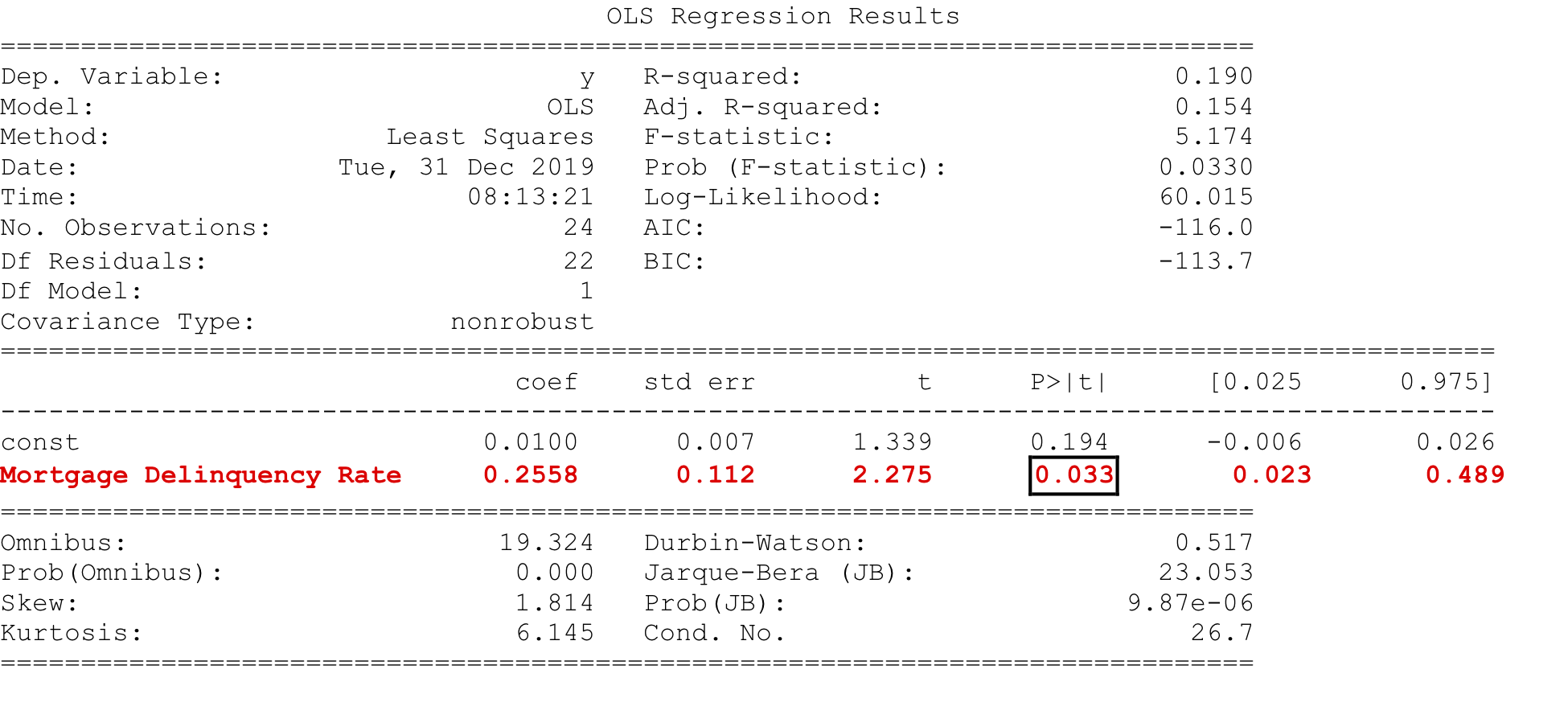

Regression .summary() results

Quantitative Risk Management in Python

Jamsheed Shorish

Computational Economist