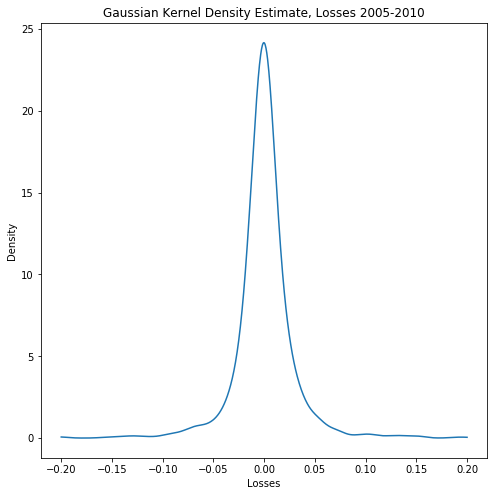

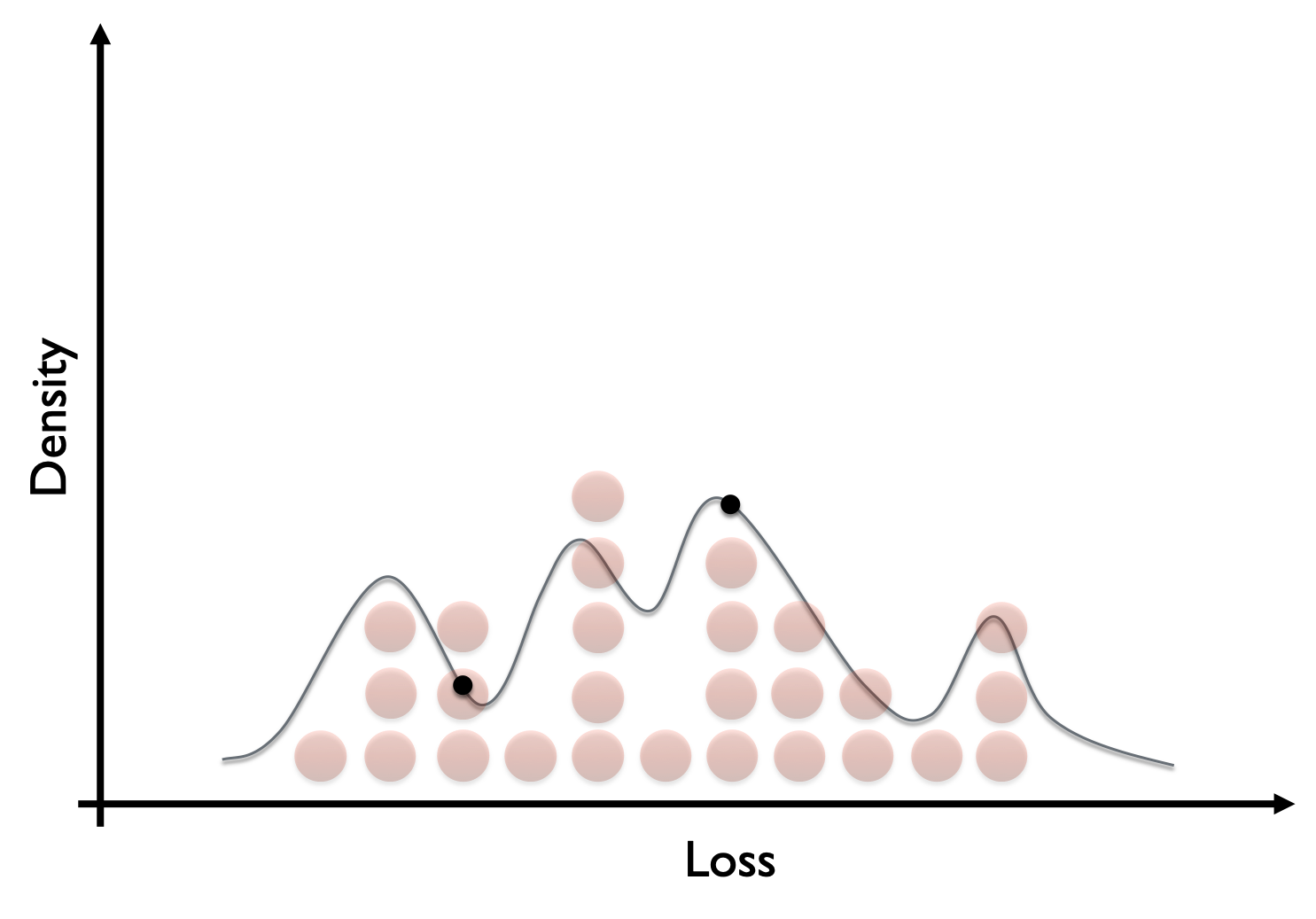

Kernel density estimation

Quantitative Risk Management in Python

Jamsheed Shorish

Computational Economist

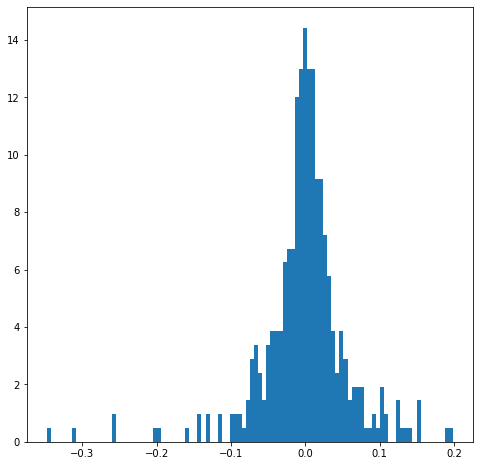

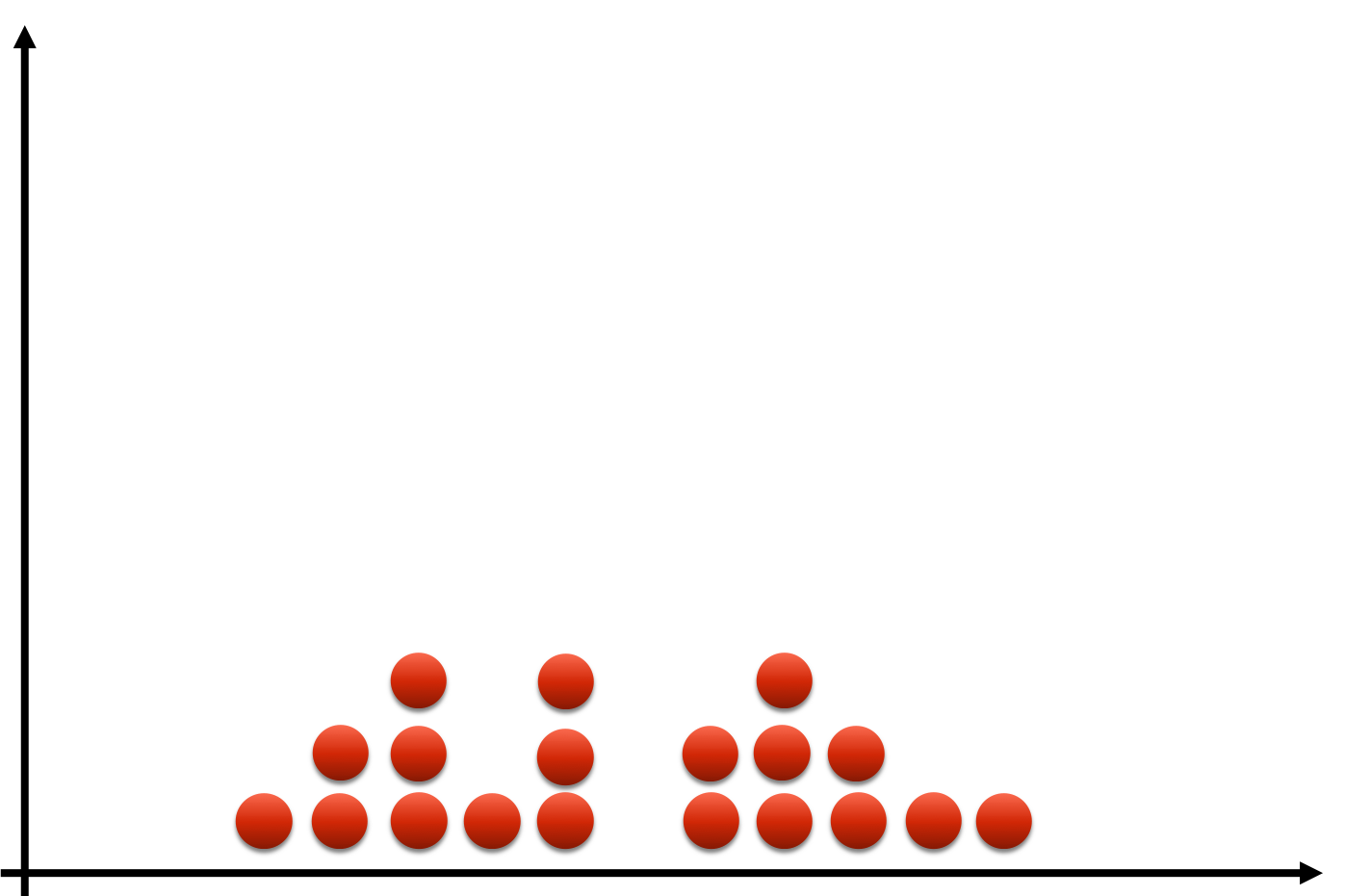

The histogram revisited

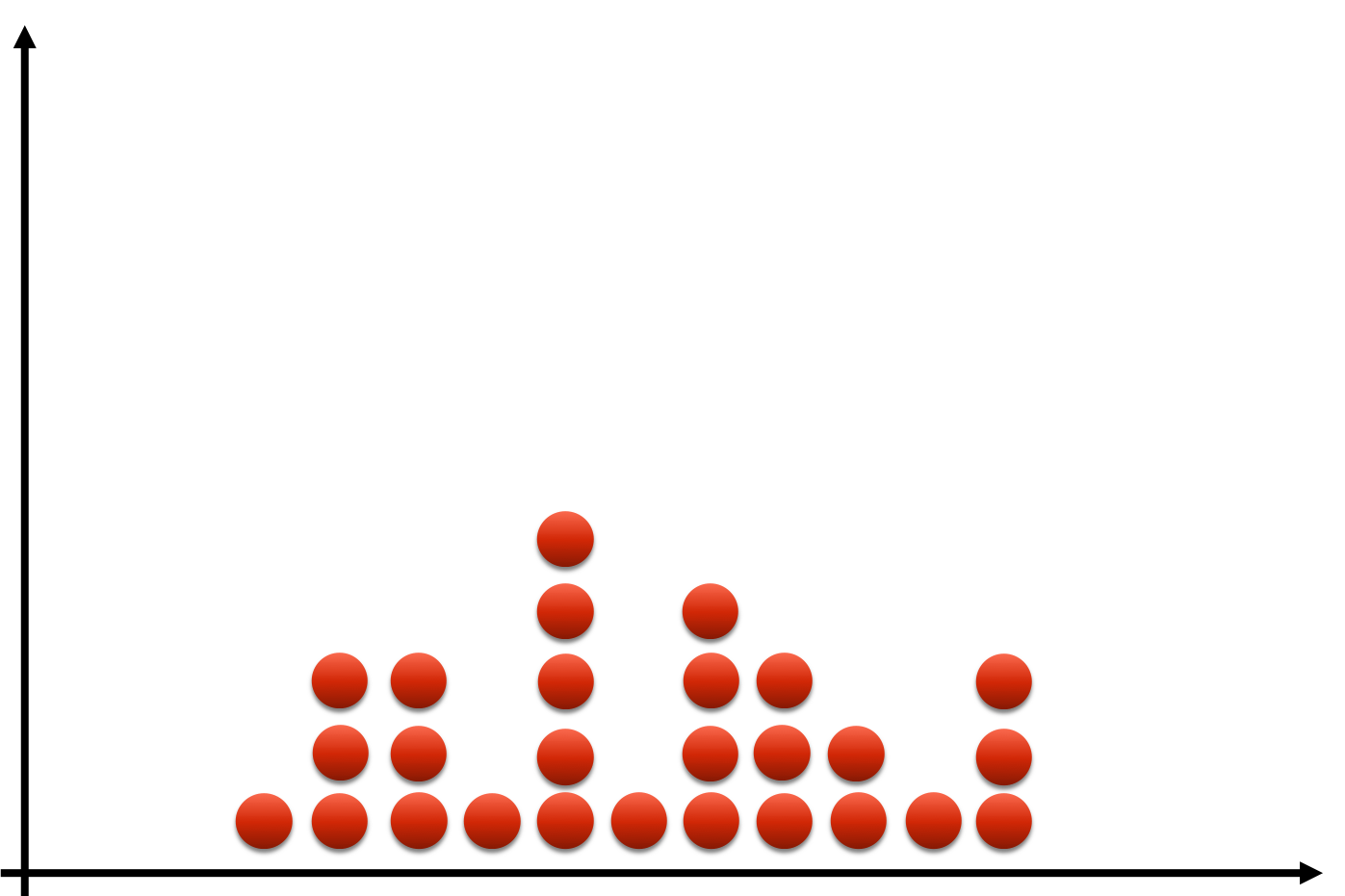

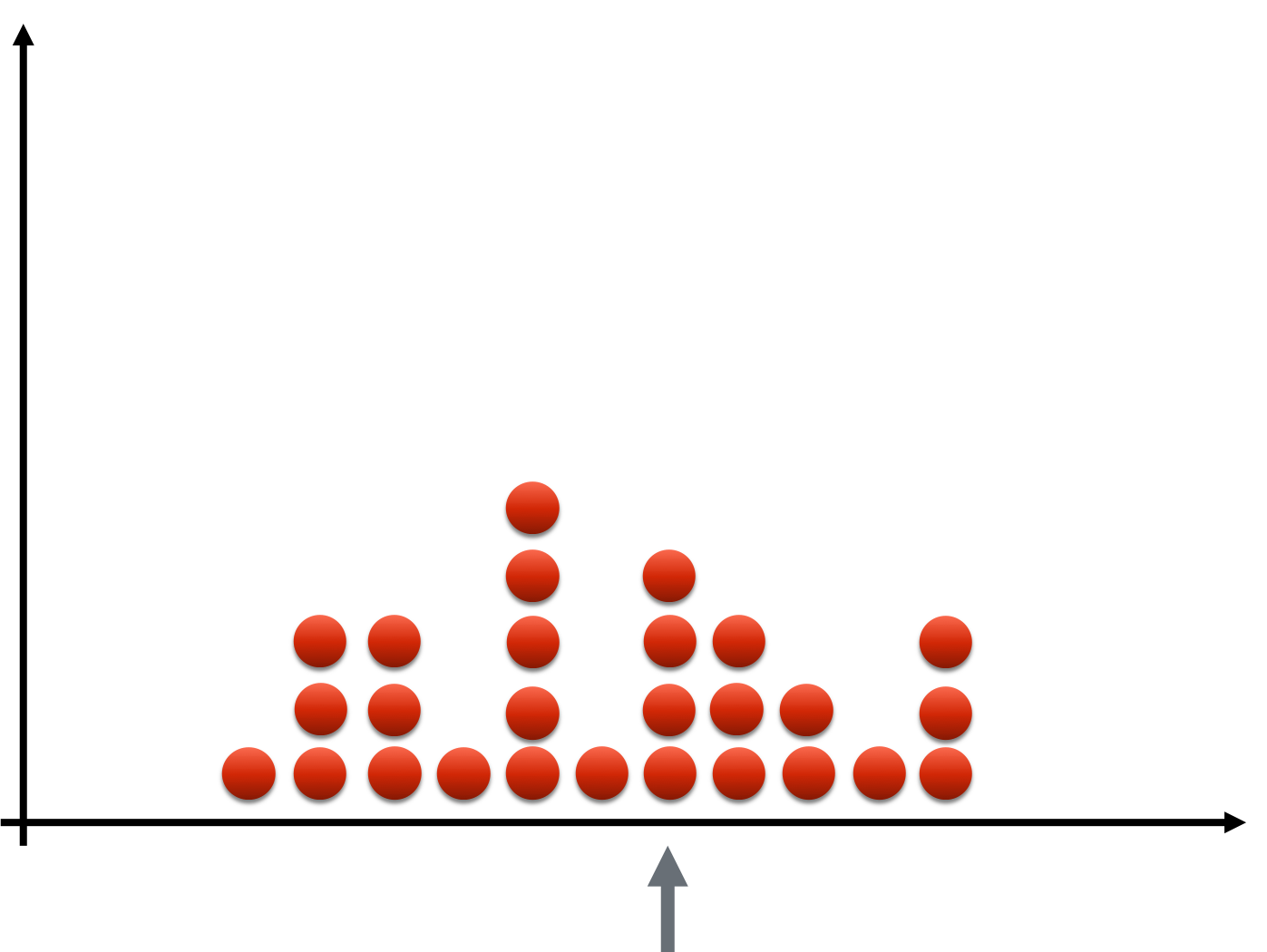

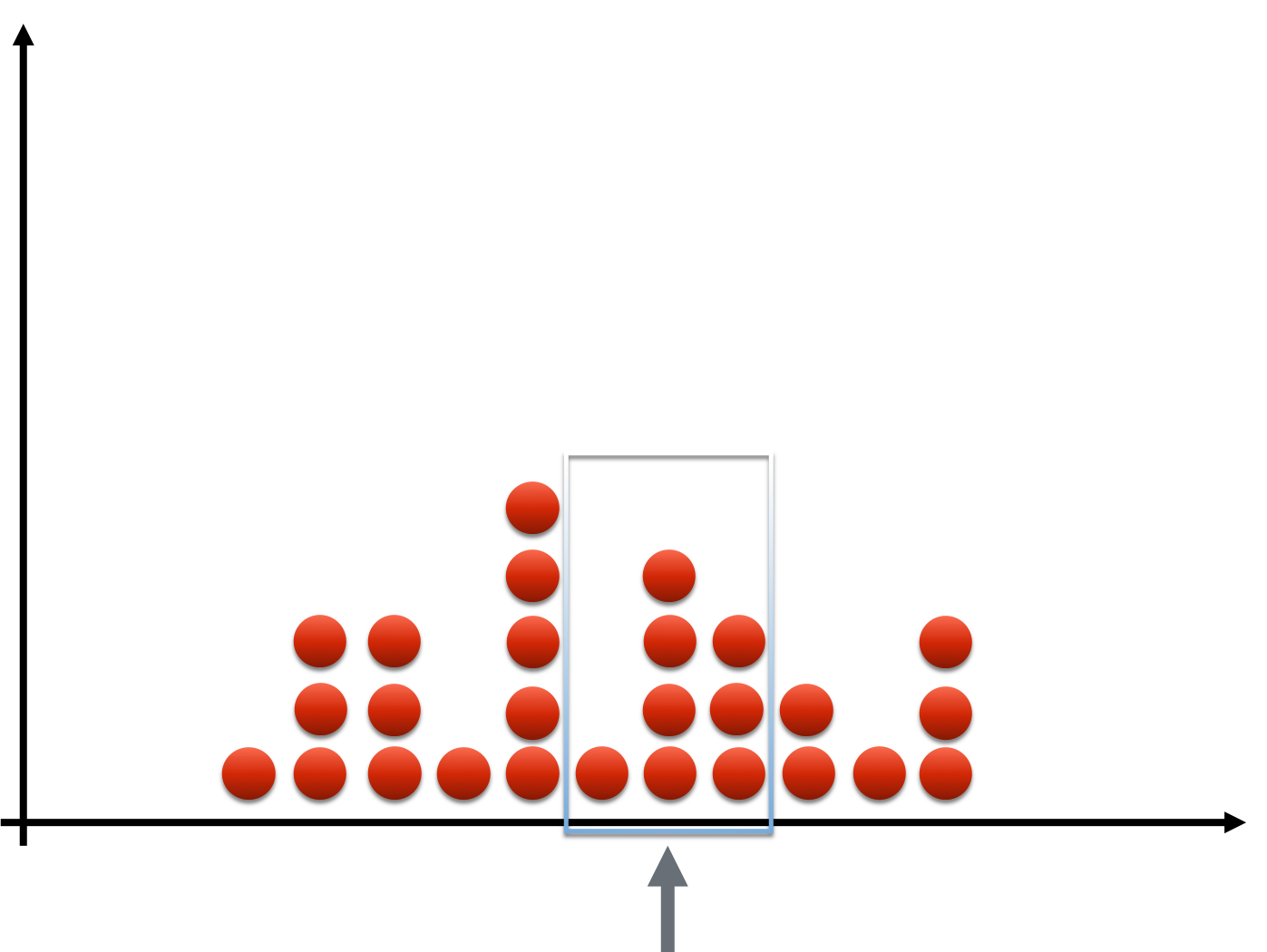

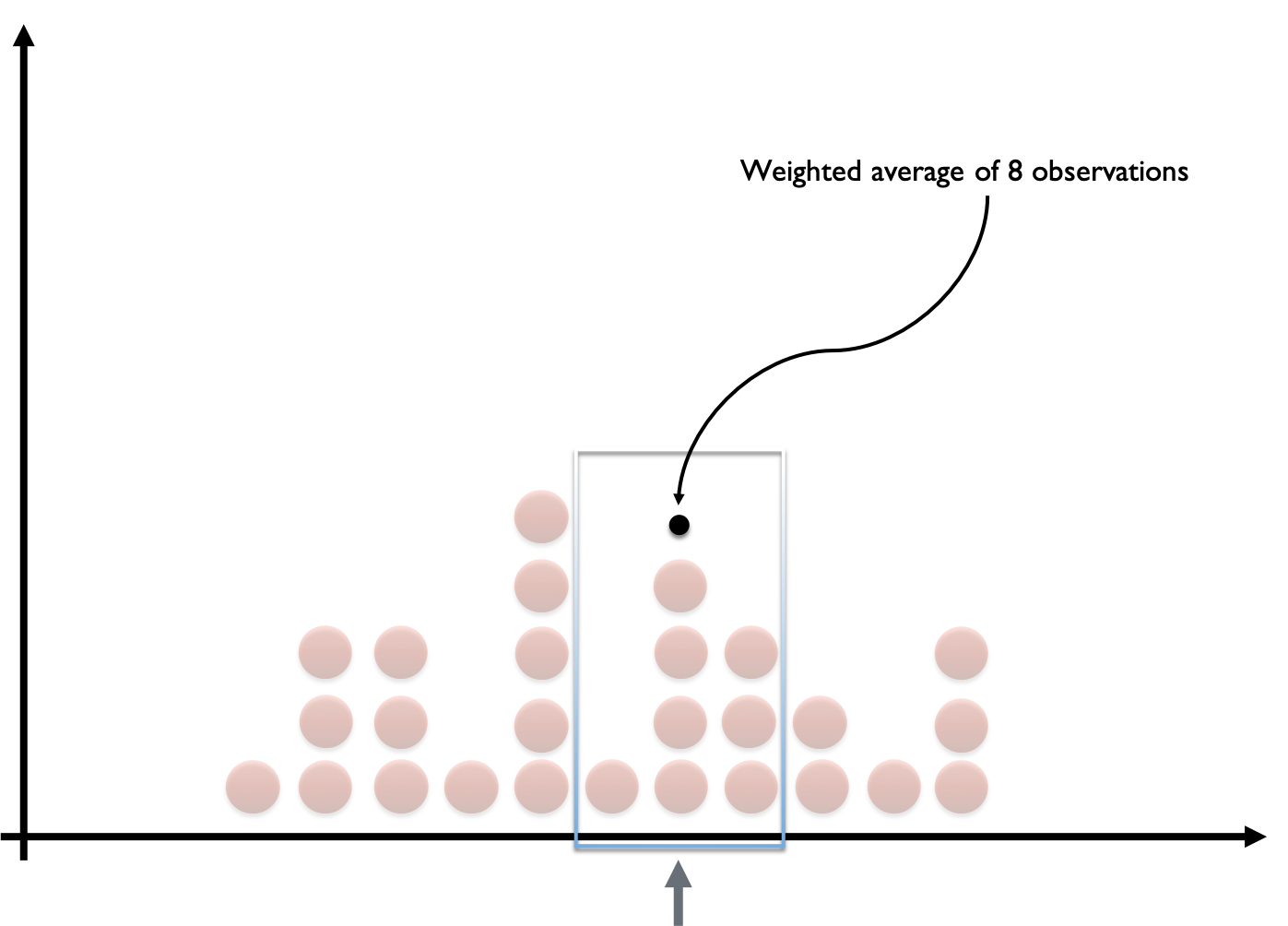

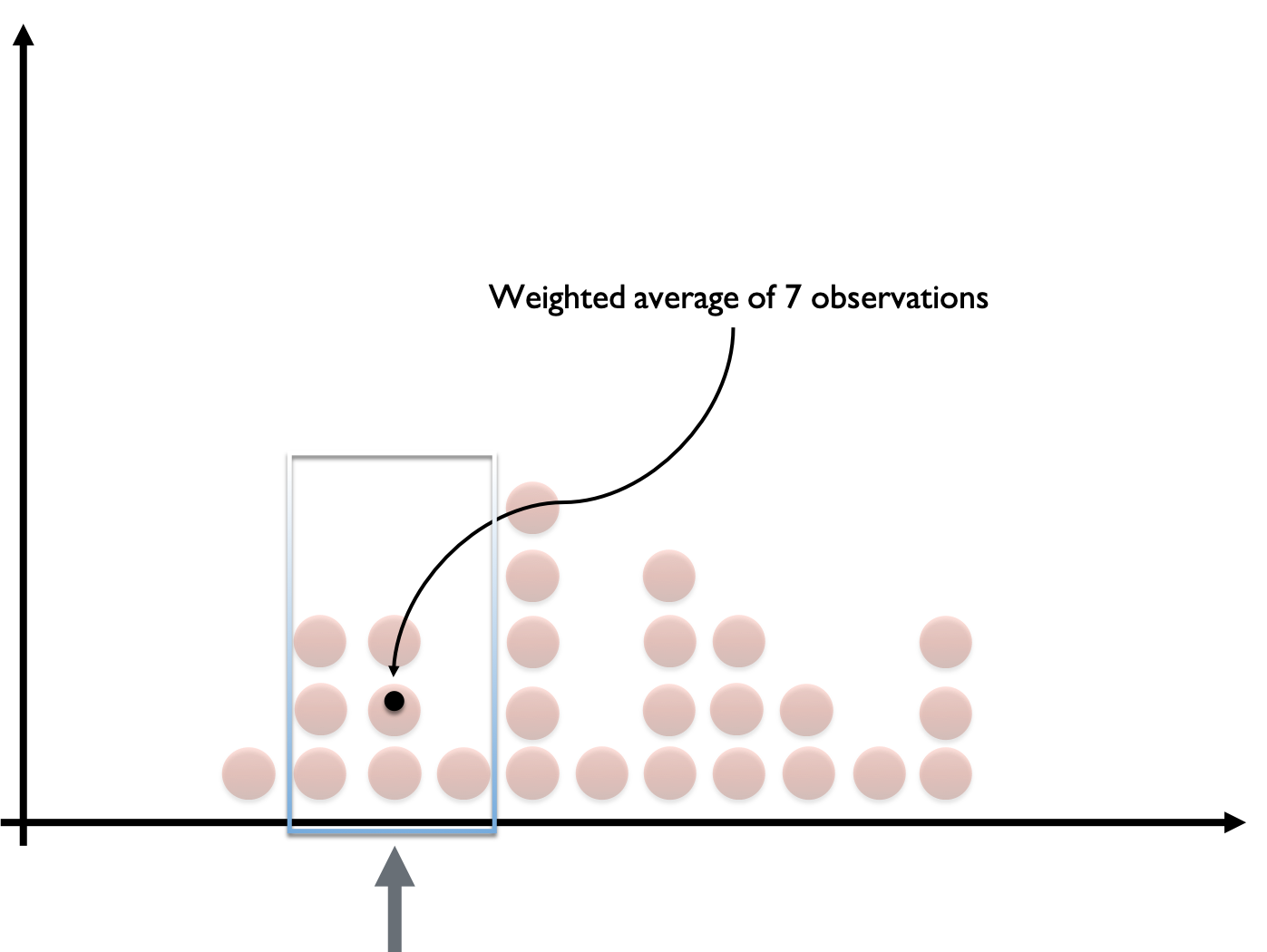

Data smoothing

Data smoothing

Data smoothing

Data smoothing

Data smoothing

Data smoothing

Data smoothing

Data smoothing

Data smoothing

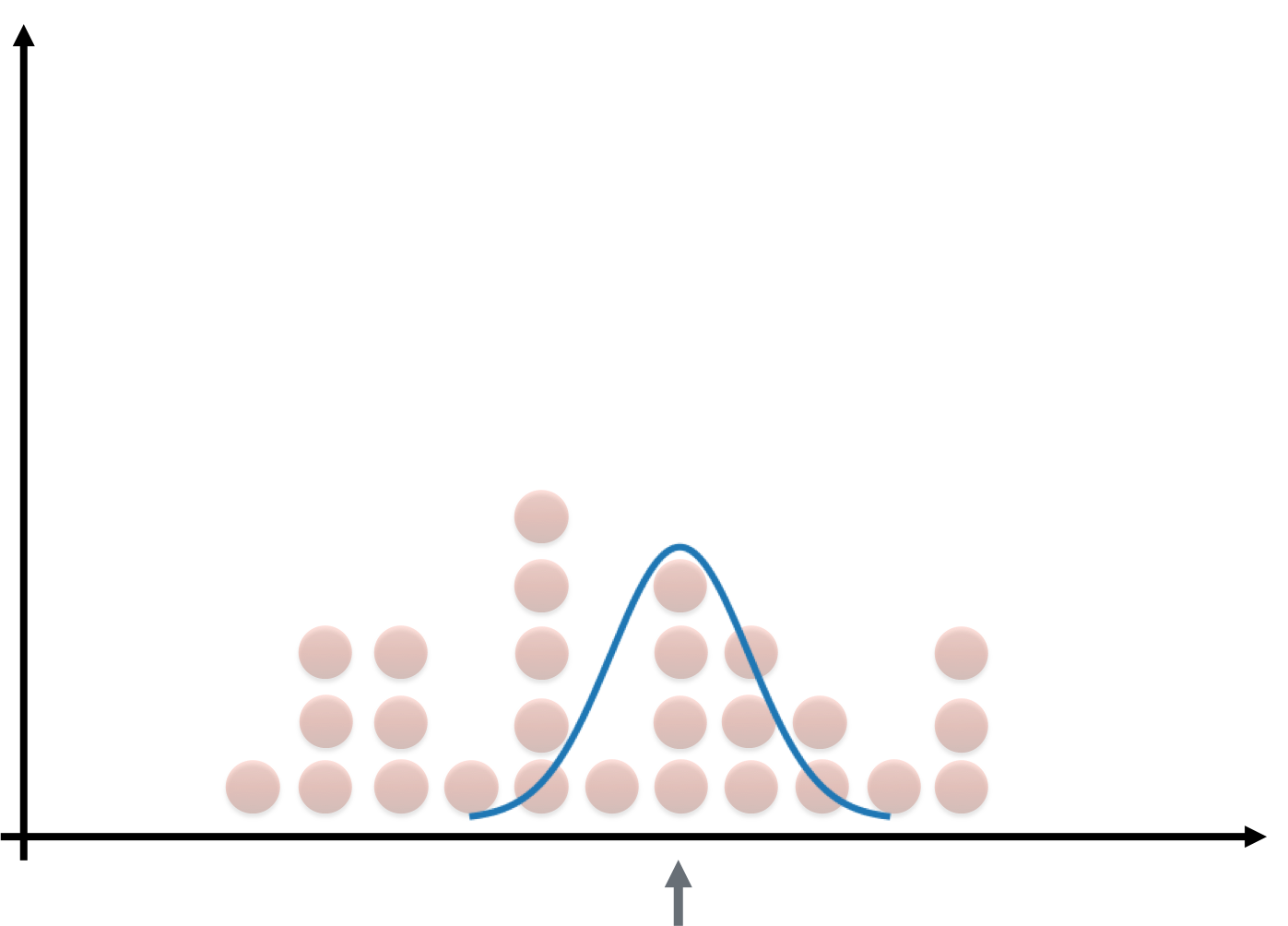

The Gaussian kernel

KDE in Python