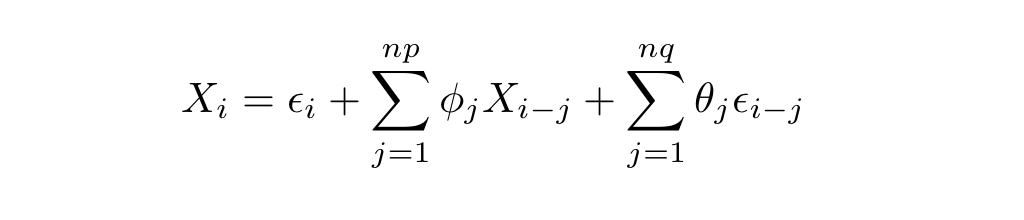

Auto regressive model

Optimizing R Code with Rcpp

Romain François

Consulting Datactive, ThinkR

Auto regressive model, AR

ar <- function(n, phi, sd){

x <- epsilon <- rnorm(n, sd = sd)

np <- length(phi)

for( i in seq(np+1, n)){

x[i] <- sum(x[seq(i-1, i-np)] * phi) + epsilon[i]

}

x

}

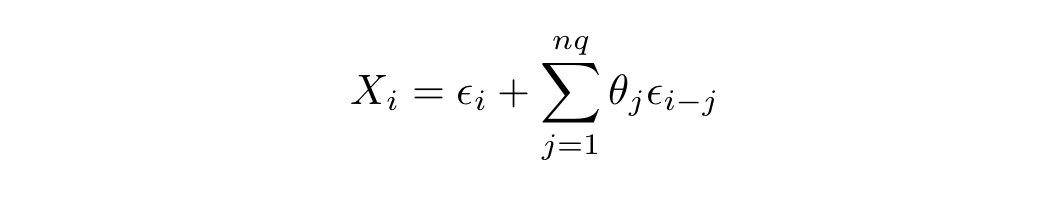

Moving average simulation

ma <- function(n, theta, sd){

epsilon <- rnorm(n, sd = sd)

x <- numeric(n)

nq <- length(theta)

for( i in seq(nq+1, n)){

x[i] <- sum(epsilon[seq(i-1, i-nq)] * theta) + epsilon[i]

}

x

}

ARMA(p,q) = AR(p) + MA(q)