Evaluación e implementación del modelo

Modelado del riesgo crediticio en Python

Michael Crabtree

Data Scientist, Ford Motor Company

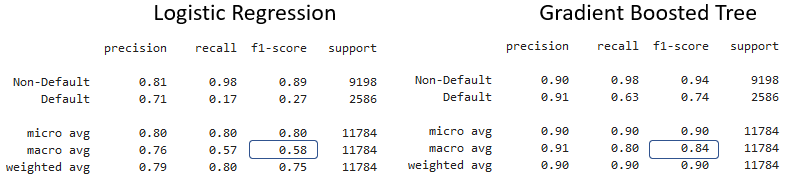

Comparar informes de clasificación

- Crea los informes con

classification_report()y compáralos

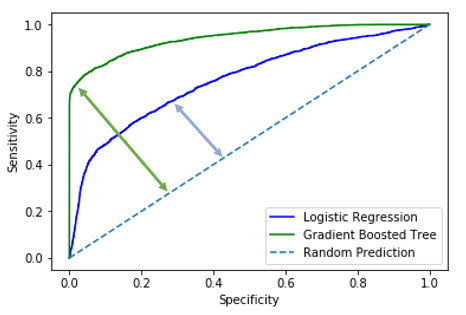

Análisis ROC y AUC

- Los modelos con mejor desempeño tienen más lift

- Más lift implica mayor AUC

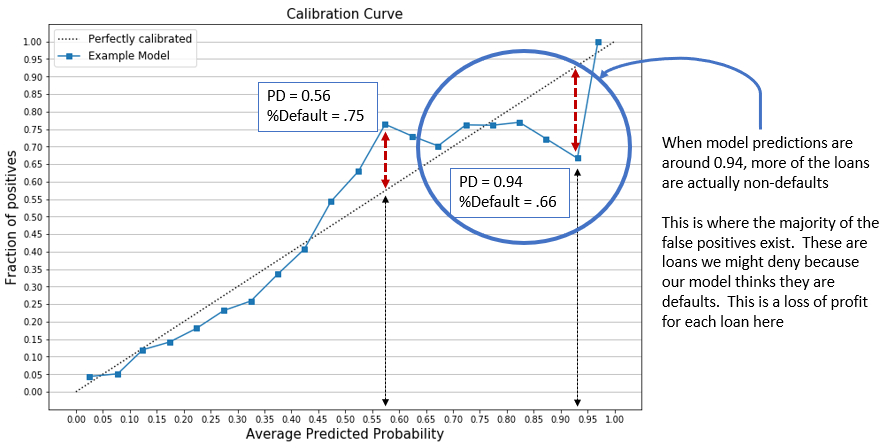

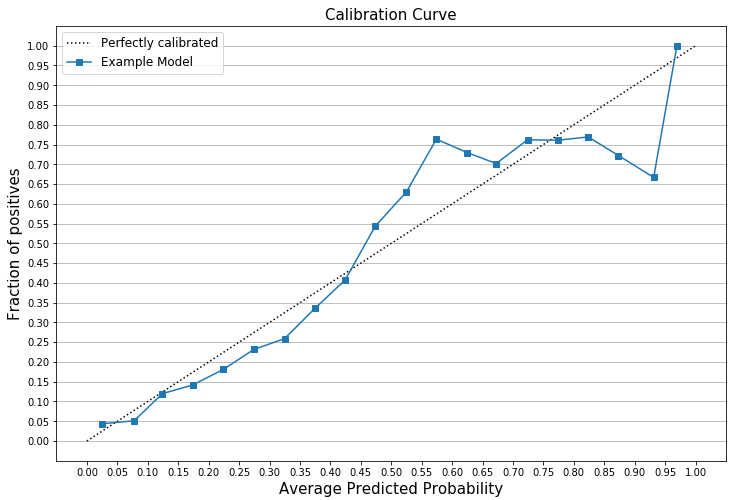

Trazar curvas de calibración

plt.plot(mean_predicted_value, fraction_of_positives, label="%s" % "Example Model")

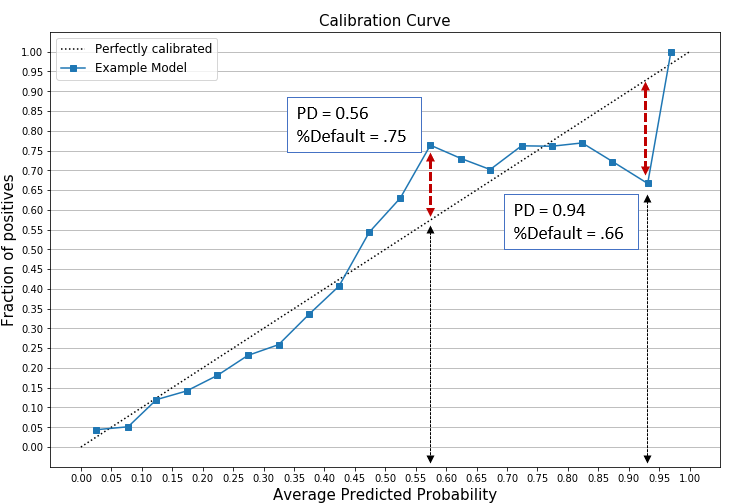

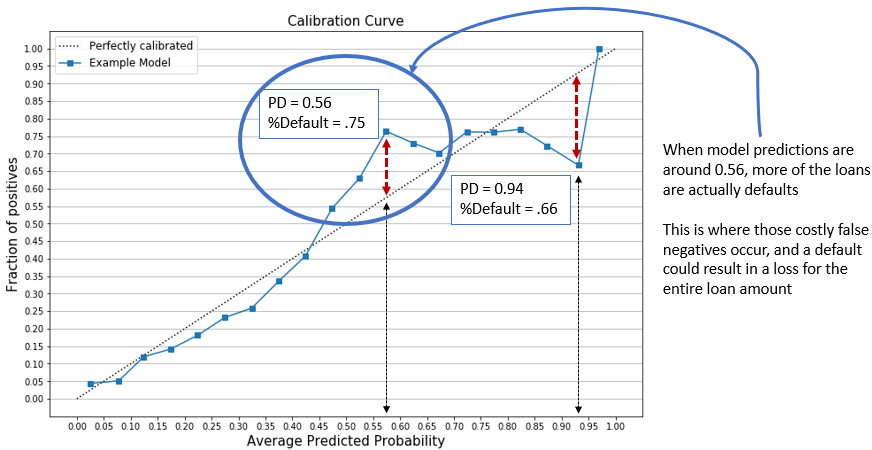

Revisar curvas de calibración

- Como ejemplo, dos eventos seleccionados (encima y debajo de la línea perfecta)

Interpretación de la curva de calibración

Interpretación de la curva de calibración