Estimating and Forecasting an AR Model

Time Series Analysis in Python

Rob Reider

Adjunct Professor, NYU-Courant Consultant, Quantopian

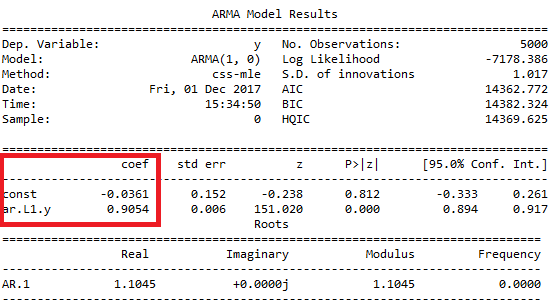

Estimating an AR Model

- Full output (true $\large \mu=0$ and $\large \phi=0.9$)

print(result.summary())

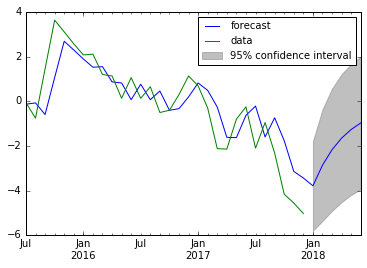

Forecasting With an AR Model

from statsmodels.graphics.tsaplots import plot_predict

fig, ax = plt.subplots()

data.plot(ax=ax)

plot_predict(result, start='2012-09-27', end='2012-10-06', alpha=0.05, ax=ax)

plt.show()

- Arguments of function

plot_predict()- First argument is fitted model

- Set

alpha=Nonefor no confidence interval - Set

ax=axto plot the data and prediction on same axes