Spaltenauswahl für Kreditausfallrisiko

Kreditrisikomodellierung in Python

Michael Crabtree

Data Scientist, Ford Motor Company

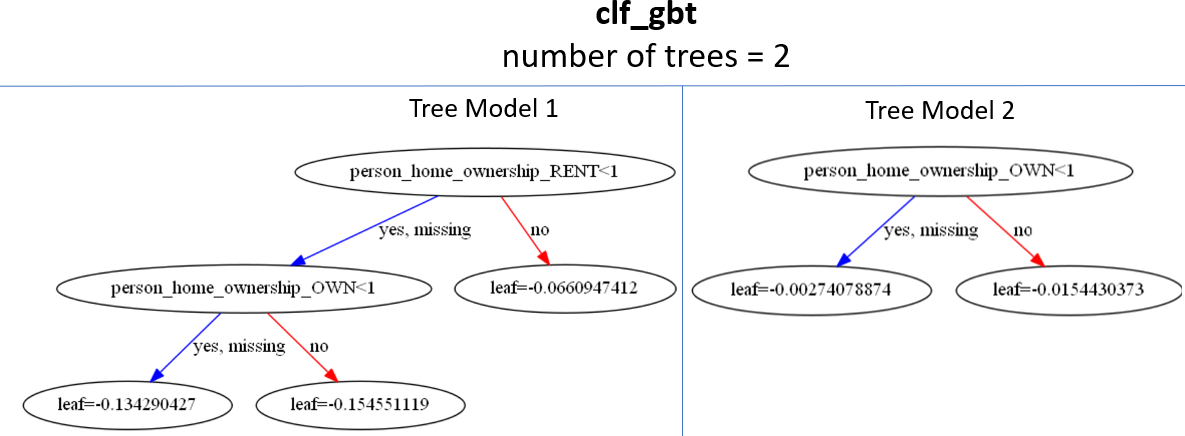

Interpretation der Spaltenwichtigkeit

# Spaltenwichtigkeiten mit importance_type = 'weight'

{'person_home_ownership_RENT': 1, 'person_home_ownership_OWN': 2}

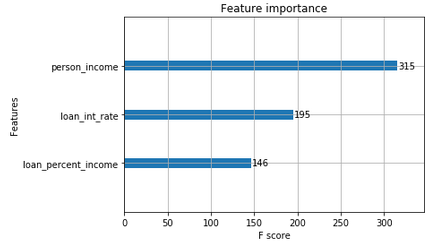

Spaltenwichtigkeiten plotten

- Nutze die Funktion

plot_importance()

xgb.plot_importance(clf_gbt, importance_type = 'weight')

{'person_income': 315, 'loan_int_rate': 195, 'loan_percent_income': 146}

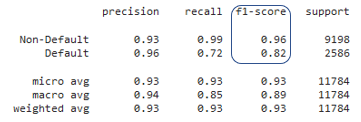

F1-Score für Modelle

- Genauigkeit und Recall für verschiedene Spaltengruppen zu prüfen kostet Zeit

- Der F1-Score fasst Genauigkeit und Recall in einer Kennzahl zusammen

- Erscheint im

classification_report()