Kreditannahmeraten

Kreditrisikomodellierung in Python

Michael Crabtree

Data Scientist, Ford Motor Company

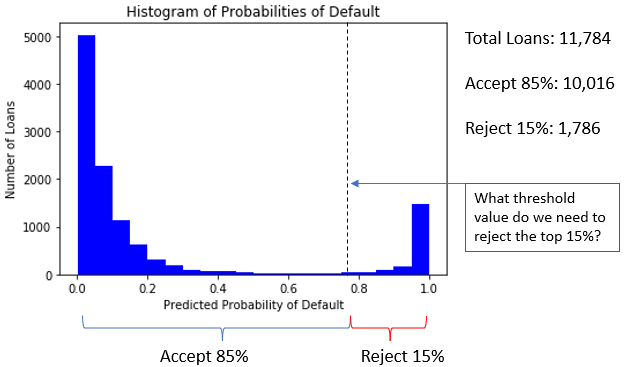

Annahmerate verstehen

- Beispiel: 85% der Kredite mit der niedrigsten

prob_defaultannehmen

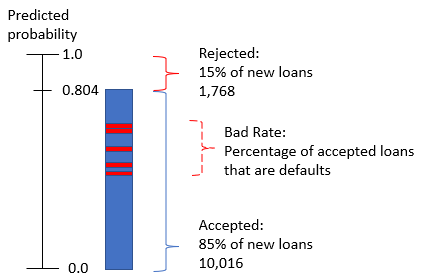

Bad Rate

- Auch mit berechnetem Schwellenwert werden einige angenommene Kredite ausfallen

- Das sind Kredite mit

prob_defaultnahe Bereichen, in denen das Modell schlecht kalibriert ist

Berechnung der Bad Rate

#Calculate the bad rate

np.sum(accepted_loans['true_loan_status']) / accepted_loans['true_loan_status'].count()

- Wenn Nichtausfall

0und Ausfall1ist, dann istsum()die Anzahl der Ausfälle .count()einer einzelnen Spalte entspricht der Zeilenanzahl des DataFrames