Index-Korrelation & Export nach Excel

Zeitreihen in Python bearbeiten

Stefan Jansen

Founder & Lead Data Scientist at Applied Artificial Intelligence

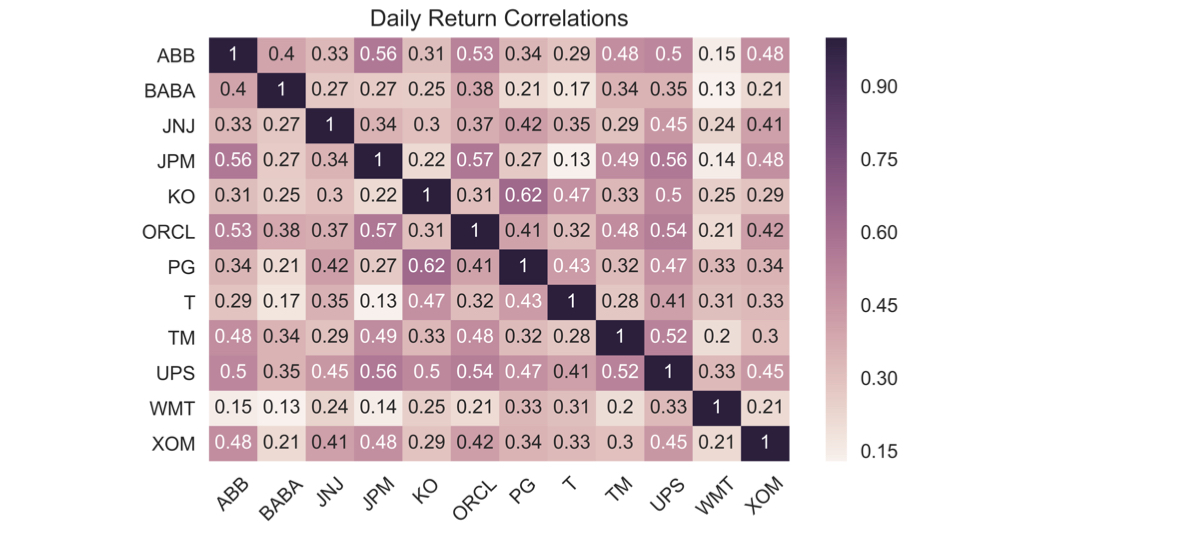

Indexkomponenten: Renditekorrelationen

sns.heatmap(correlations, annot=True)

plt.xticks(rotation=45)

plt.title('Daily Return Correlations')

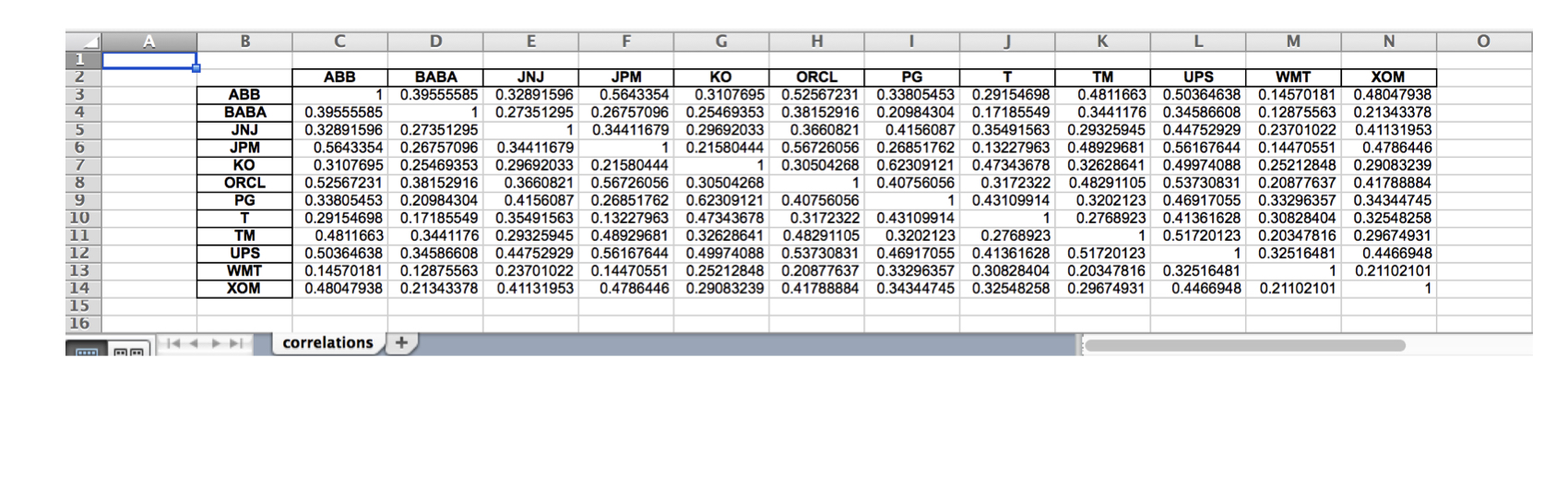

In ein einzelnes Excel-Tabellenblatt speichern

correlations.to_excel(excel_writer= 'correlations.xls',

sheet_name='correlations',

startrow=1,

startcol=1)

In mehrere Excel-Tabellenblätter speichern

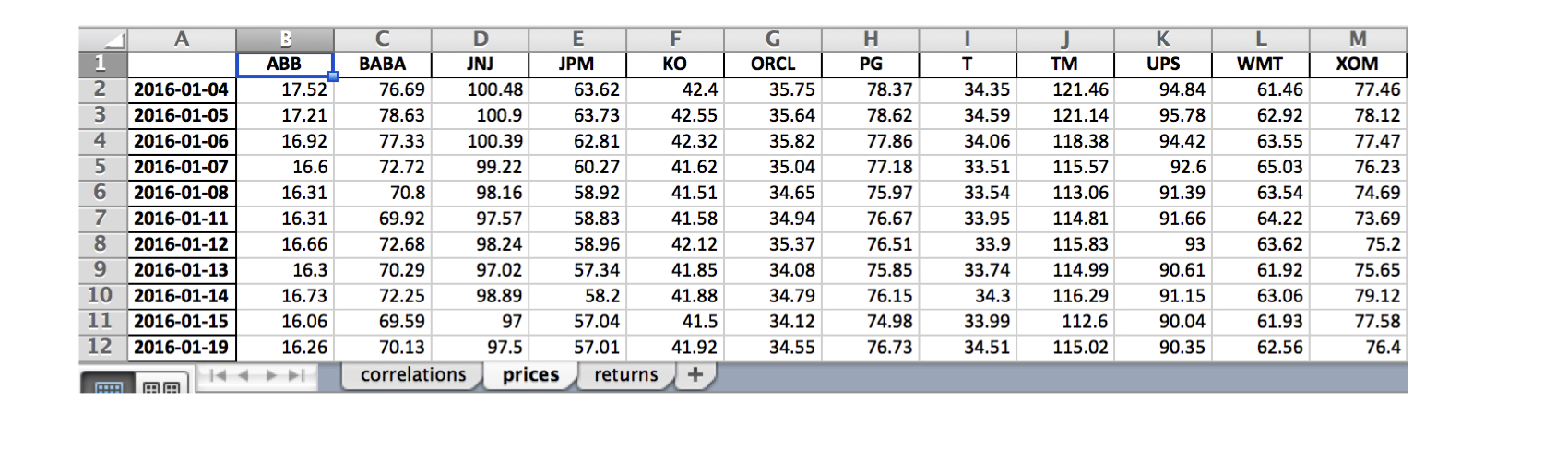

data.index = data.index.date # Keep only date componentwith pd.ExcelWriter('stock_data.xlsx') as writer:corr.to_excel(excel_writer=writer, sheet_name='correlations')data.to_excel(excel_writer=writer, sheet_name='prices')data.pct_change().to_excel(writer, sheet_name='returns')