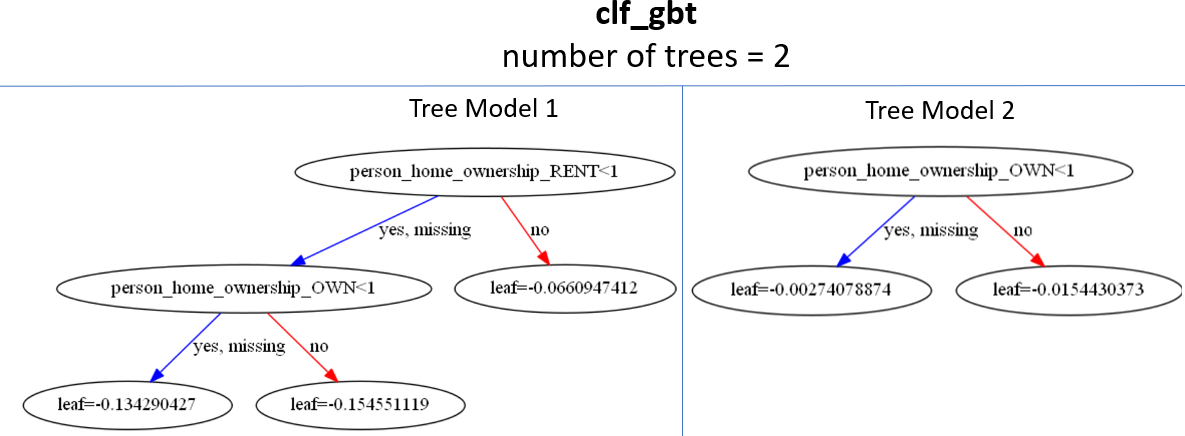

Selezione colonne per il rischio di credito

Credit Risk Modeling in Python

Michael Crabtree

Data Scientist, Ford Motor Company

Interpretare l'importanza delle colonne

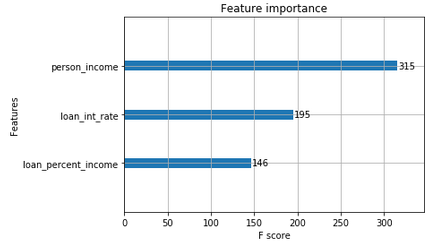

# Importanza colonne da importance_type = 'weight'

{'person_home_ownership_RENT': 1, 'person_home_ownership_OWN': 2}

Grafico dell'importanza delle colonne

- Usa la funzione

plot_importance()

xgb.plot_importance(clf_gbt, importance_type = 'weight')

{'person_income': 315, 'loan_int_rate': 195, 'loan_percent_income': 146}

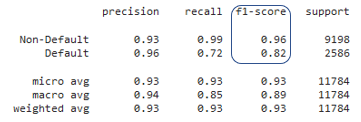

F1 score per i modelli

- Valutare accuracy e recall per gruppi di colonne richiede tempo

- L'F1 è un'unica metrica che combina accuracy e recall

- È mostrato nel

classification_report()