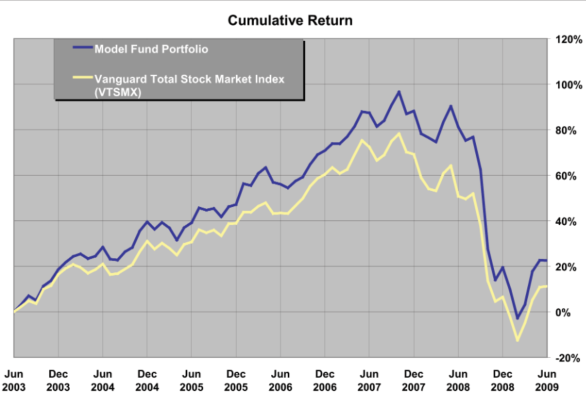

Confronto con un benchmark

Introduzione all'analisi di portafoglio in Python

Charlotte Werger

Data Scientist

Investimento attivo vs benchmark

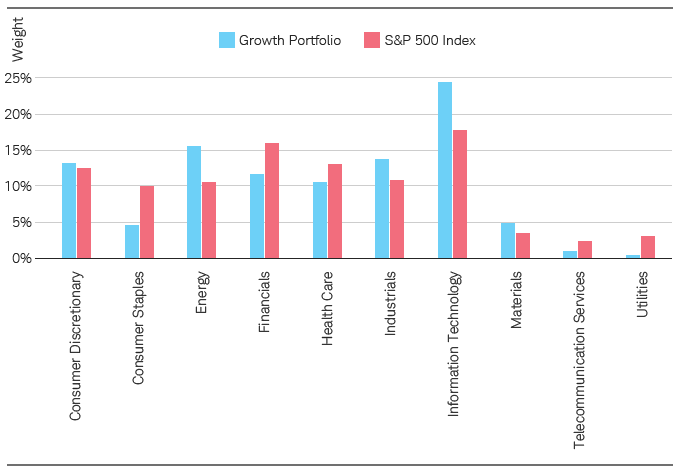

Pesi attivi

1 Fonte: Schwab Center for Financial Research.

Introduzione all'analisi di portafoglio in Python

Charlotte Werger

Data Scientist