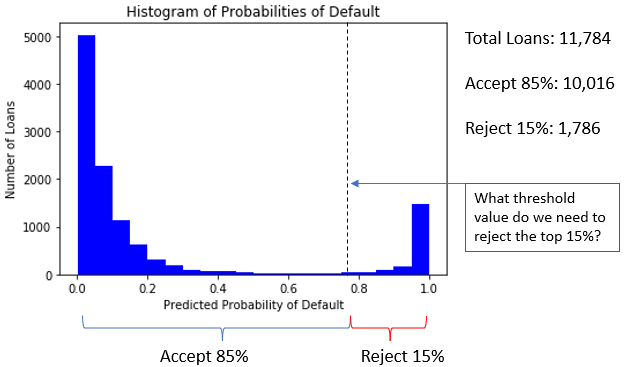

Kredi kabul oranları

Python ile Kredi Riski Modellemesi

Michael Crabtree

Data Scientist, Ford Motor Company

Kabul oranını anlama

- Örnek: En düşük

prob_defaultdeğerine sahip kredilerin %85'ini kabul et

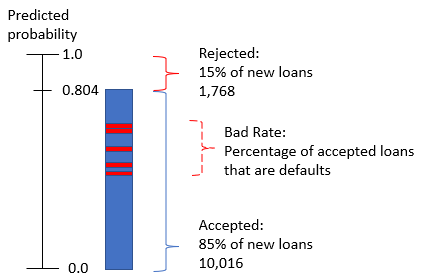

Kötü Oran

- Hesaplanan eşik olsa da, kabul edilen bazı krediler temerrüde düşer

- Bunlar, modelimizin iyi kalibre edilmediği

prob_defaulteşiğine yakın kredilerdir

Kötü oran hesabı

#Calculate the bad rate

np.sum(accepted_loans['true_loan_status']) / accepted_loans['true_loan_status'].count()

- Temerrüt değil

0, temerrüt1ise,sum()temerrüt sayısıdır - Tek bir sütunun

.count()değeri, veri çerçevesinin satır sayısıyla aynıdır