Kredi modelleri için çapraz doğrulama

Python ile Kredi Riski Modellemesi

Michael Crabtree

Data Scientist, Ford Motor Company

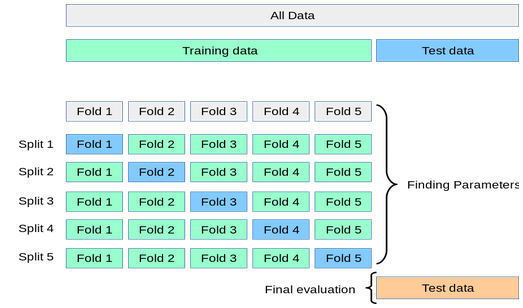

Çapraz doğrulama nasıl çalışır

- Eğitim verisinin parçalarını (fold) işler ve kalan kısımda test eder

- Son test, gerçek test kümesine karşı yapılır

1 https://scikit-learn.org/stable/modules/cross_validation.html

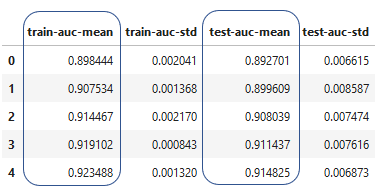

Çapraz doğrulama sonuçları

- Çapraz doğrulamadan gelen değerlerle bir veri çerçevesi oluşturur