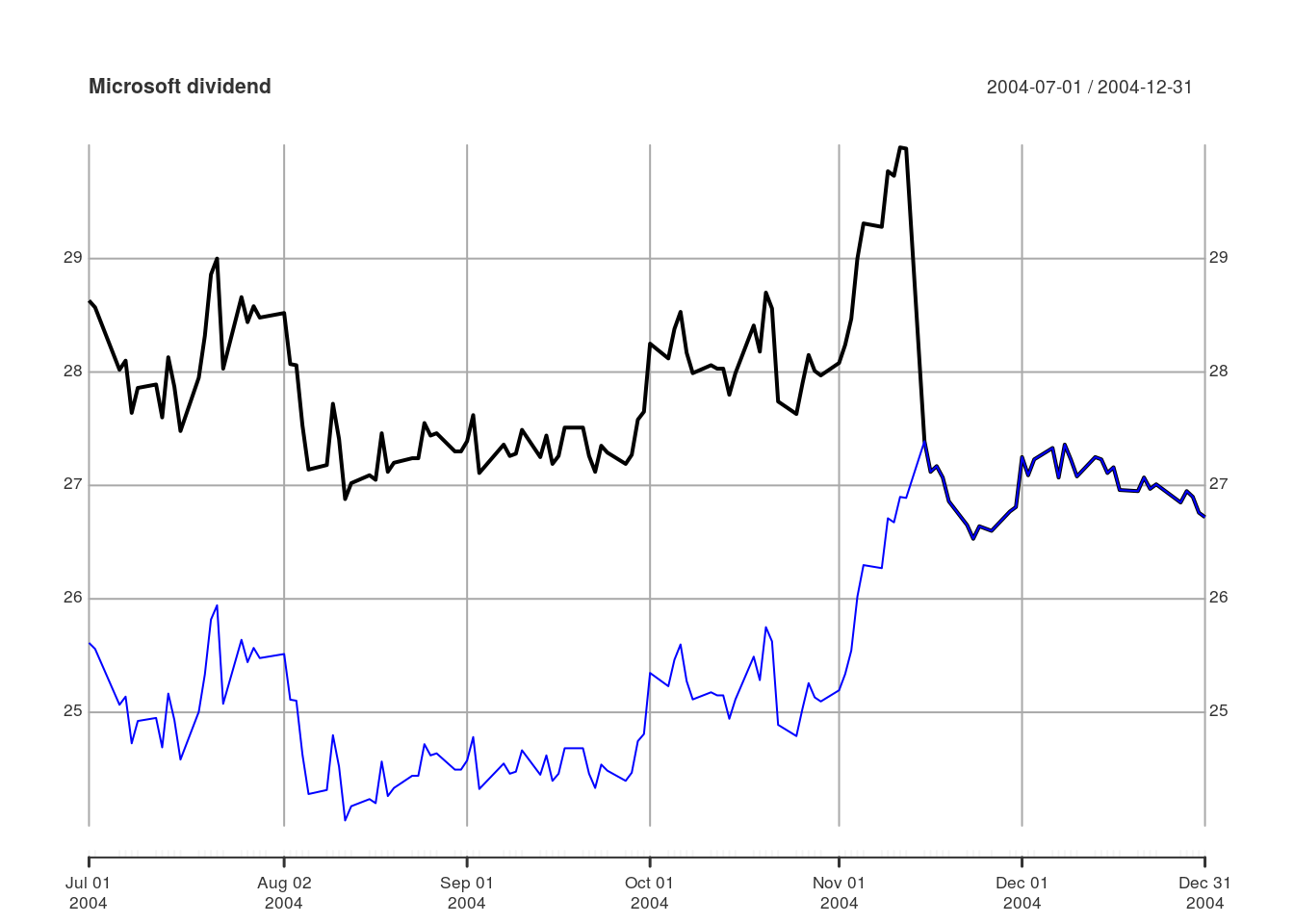

Şirket işlemlerine göre ayarlama

R ile Finansal Verileri İçe Aktarma ve Yönetme

Joshua Ulrich

Quantitative Analyst & quantmod Co-Author and Maintainer

Hisse bölünmeleri ve temettüler için ayarlama (2)

R ile Finansal Verileri İçe Aktarma ve Yönetme

Joshua Ulrich

Quantitative Analyst & quantmod Co-Author and Maintainer