Groeipercentages van tijdreeksen vergelijken

Tijdreeksgegevens manipuleren in Python

Stefan Jansen

Founder & Lead Data Scientist at Applied Artificial Intelligence

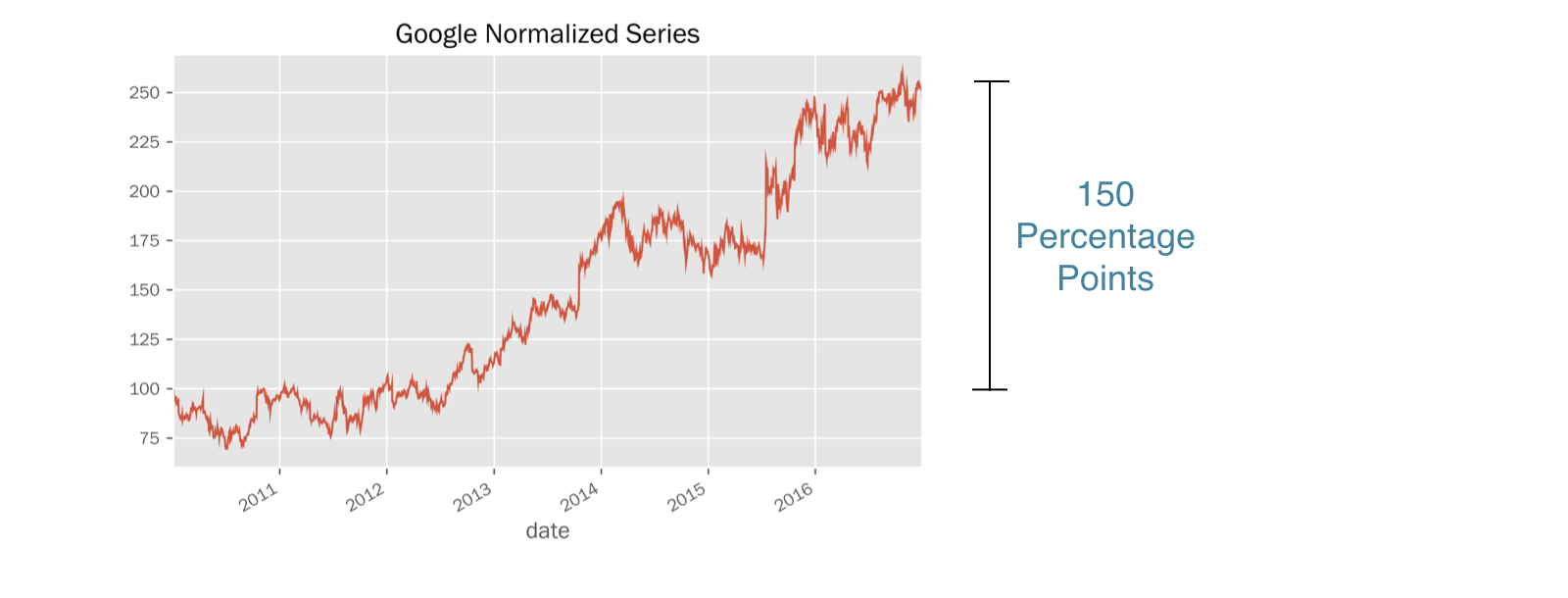

Eén reeks normaliseren (2)

normalized = google.price.div(first_price).mul(100)normalized.plot(title='Google Normalized Series')

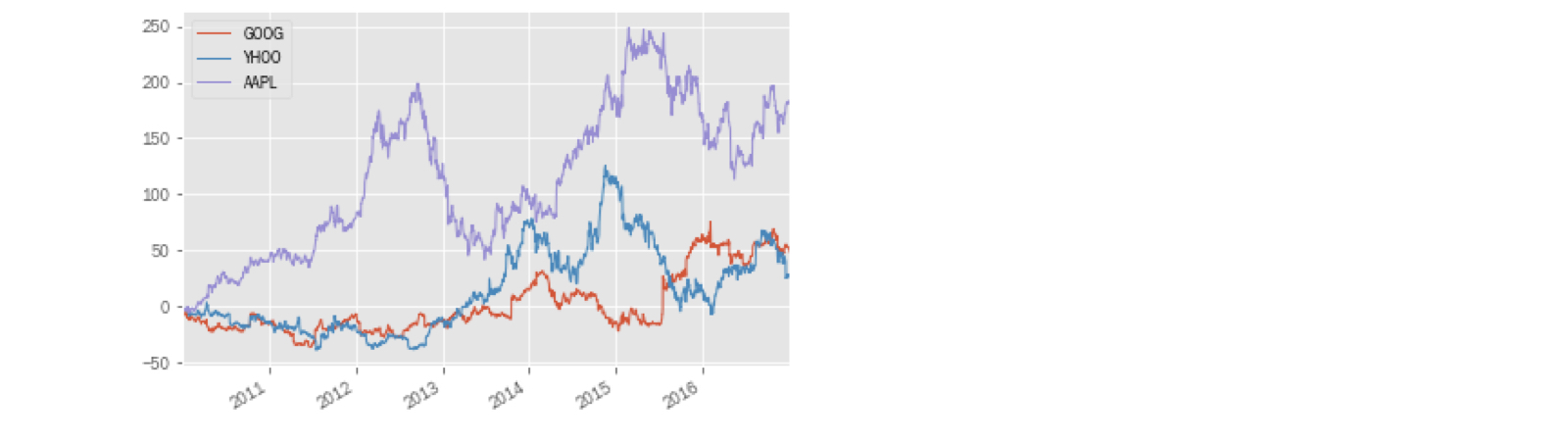

Vergelijken met een benchmark (2)

prices.head(1)

AAPL GOOG YHOO SP500

2010-01-04 30.57 313.06 17.10 1132.99

normalized = prices.div(prices.iloc[0]).mul(100)normalized.plot()

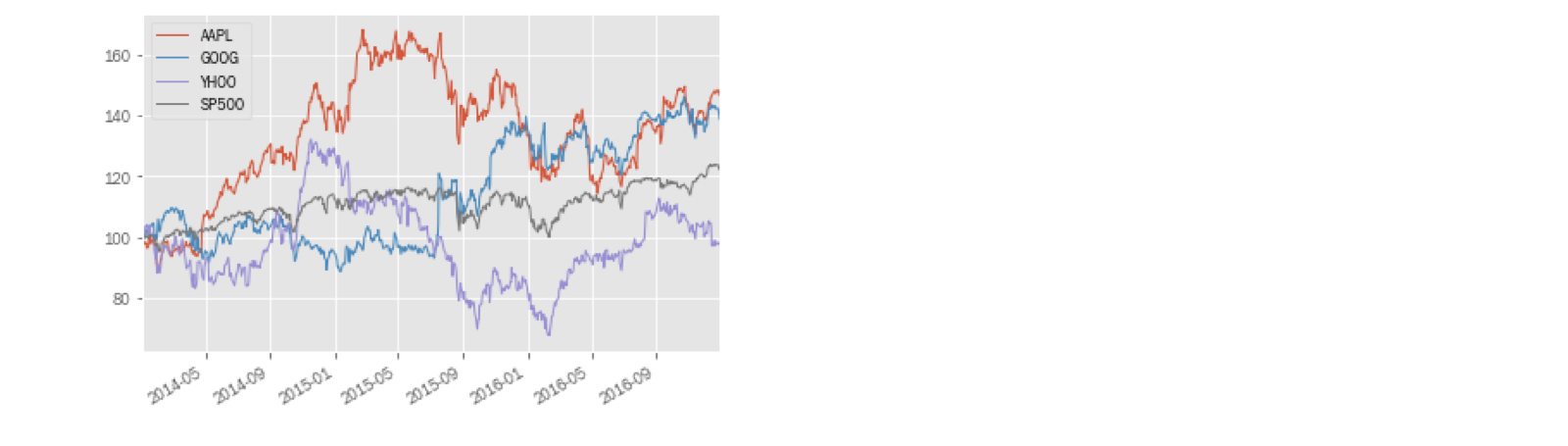

Prestatieverschil plotten

diff.plot()