Cointegration Models

Tijdreeksanalyse in Python

Rob Reider

Adjunct Professor, NYU-Courant Consultant, Quantopian

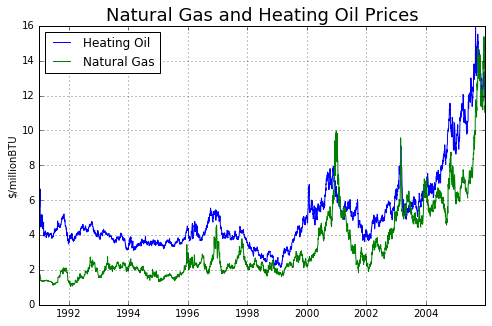

Example: Heating Oil and Natural Gas

- Heating Oil and Natural Gas both look like random walks...

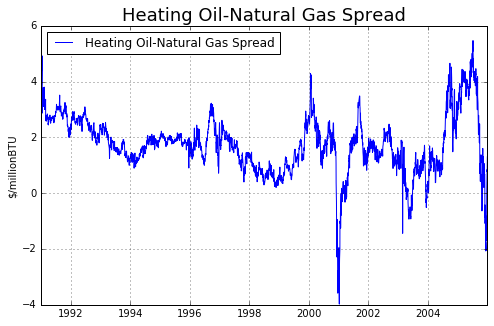

Example: Heating Oil and Natural Gas

- But the spread (difference) is mean reverting