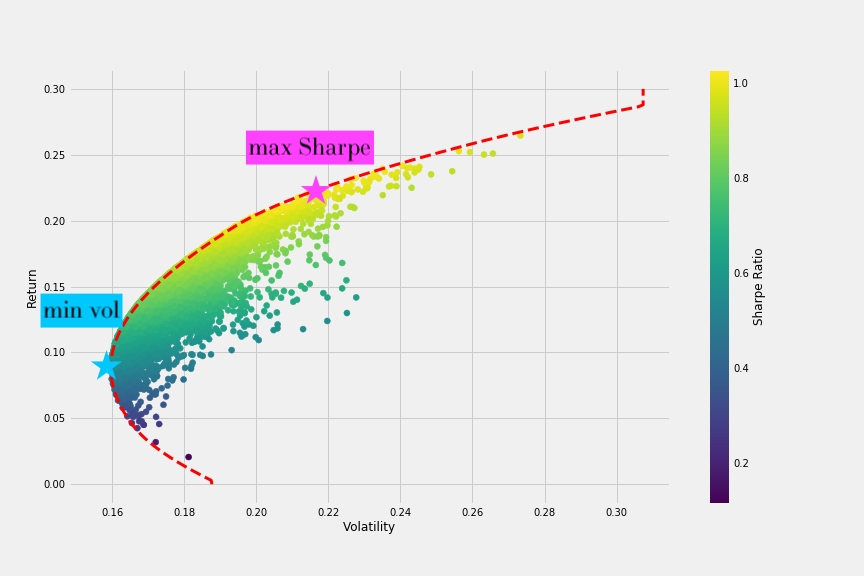

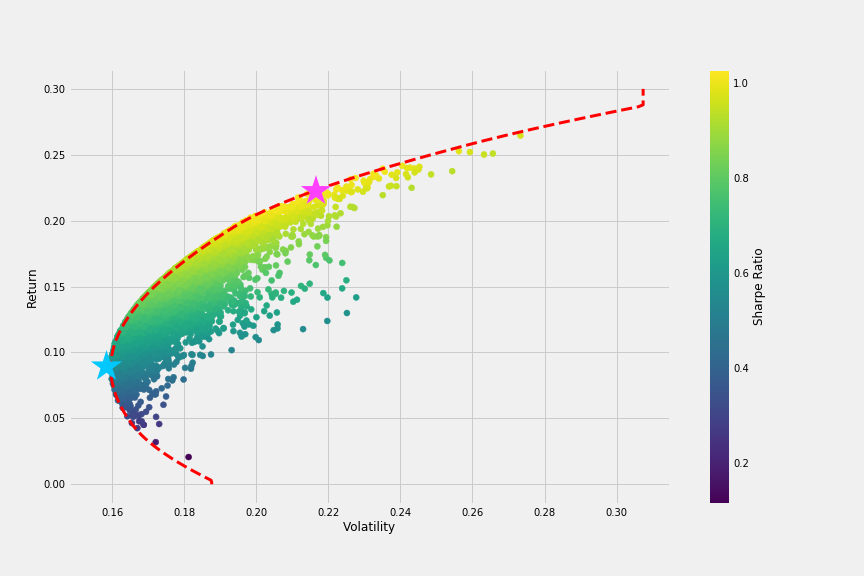

Maximale Sharpe vs. minimale volatiliteit

Introductie tot portefeuille-analyse in Python

Charlotte Werger

Data Scientist

Weet je de efficiënte grens nog?

$$

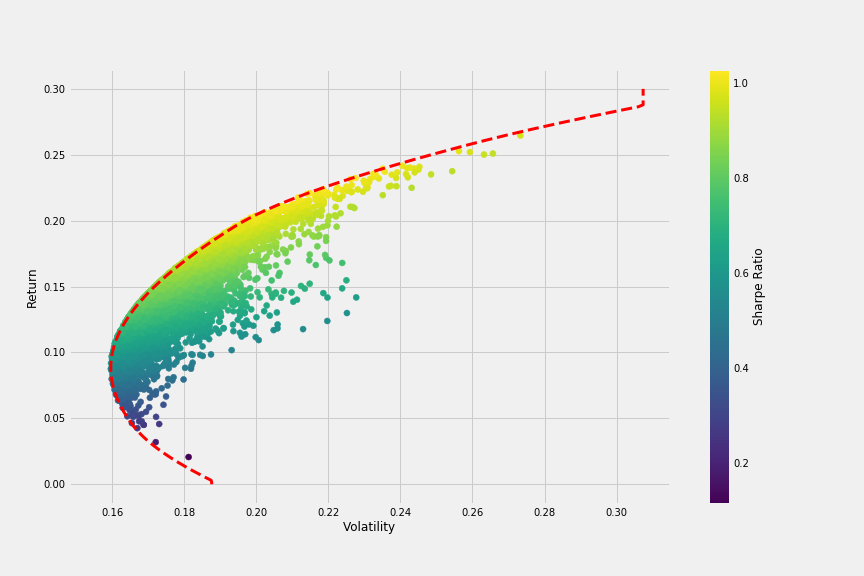

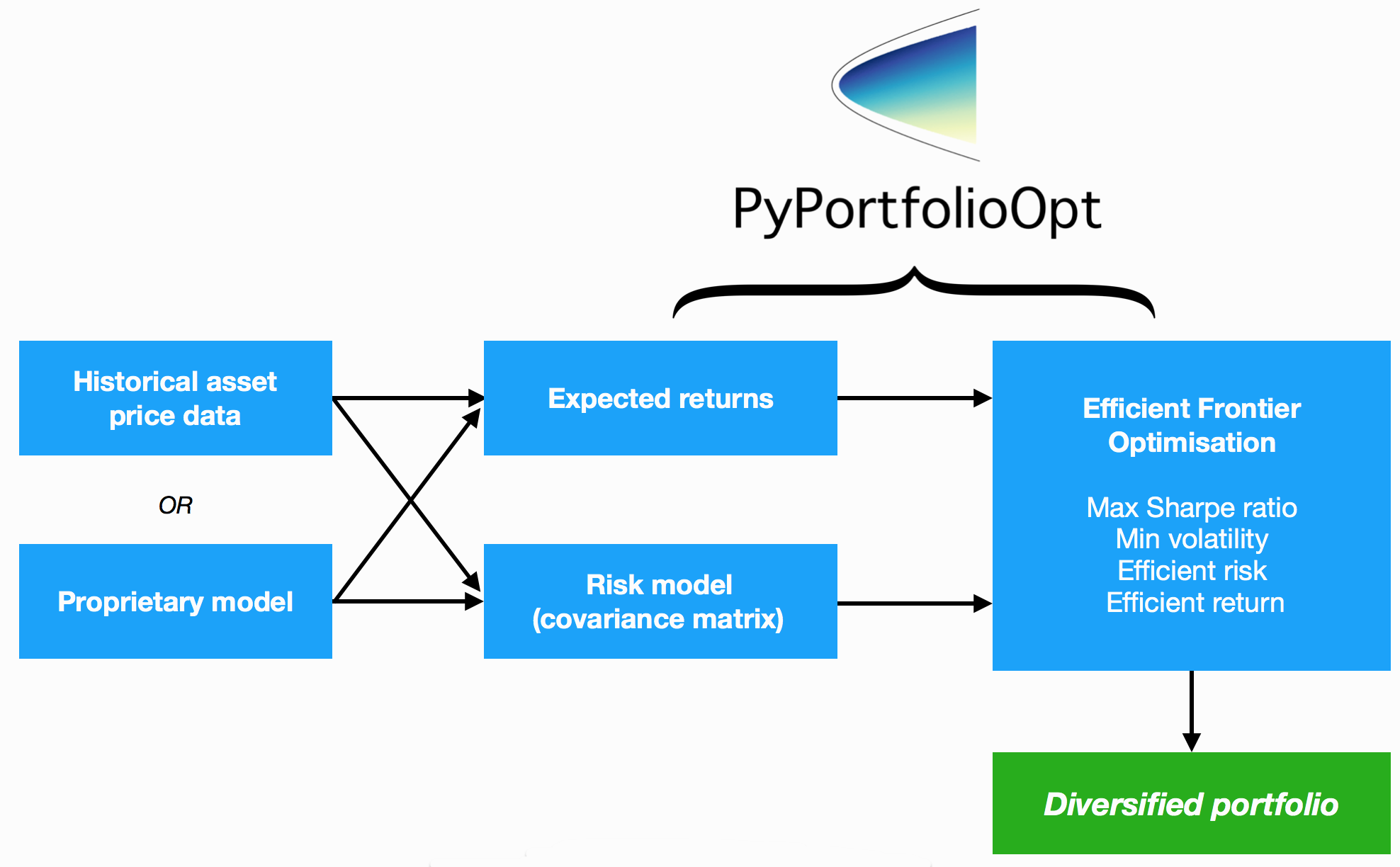

Optimalisatie in PyPortfolioOpt aanpassen

Kijk nog eens naar de efficiënte grens

Maximale Sharpe versus minimale volatiliteit