Dynamische harmonische regressie

Voorspellen in R

Rob J. Hyndman

Professor of Statistics at Monash University

Dynamische harmonische regressie

Dynamische harmonische regressie

$m =$ seizoensperiode

Elke periodieke functie is te benaderen met sommen van sin- en cos-termen bij voldoende grote K

Regressiecoëfficiënten: $\alpha_k$ en $\gamma_k$

$e_t$ kan worden gemodelleerd als een niet-seizoensgebonden ARIMA-proces

Veronderstelt een onveranderlijk seizoenspatroon

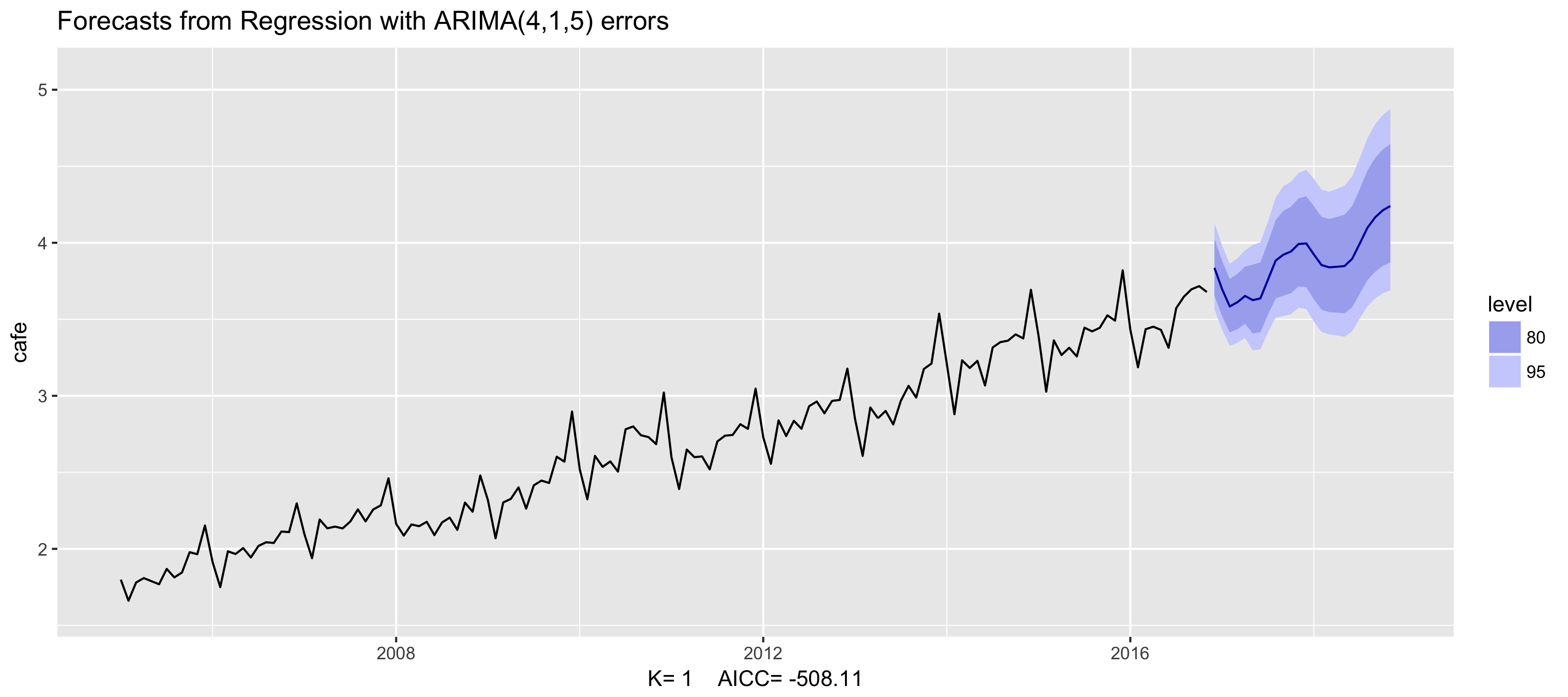

Voorbeeld: Australische cafébestedingen

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 1),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 1, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

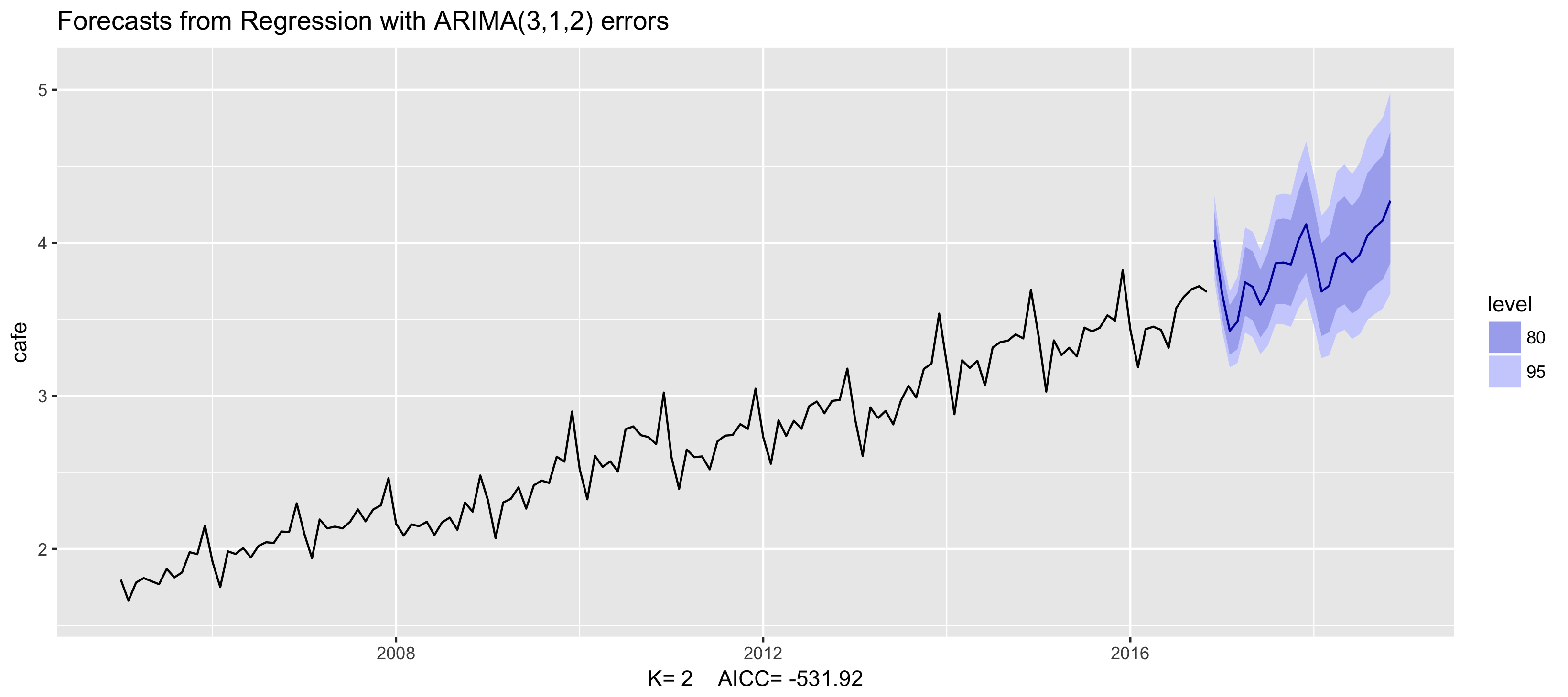

Voorbeeld: Australische cafébestedingen

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 2),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 2, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

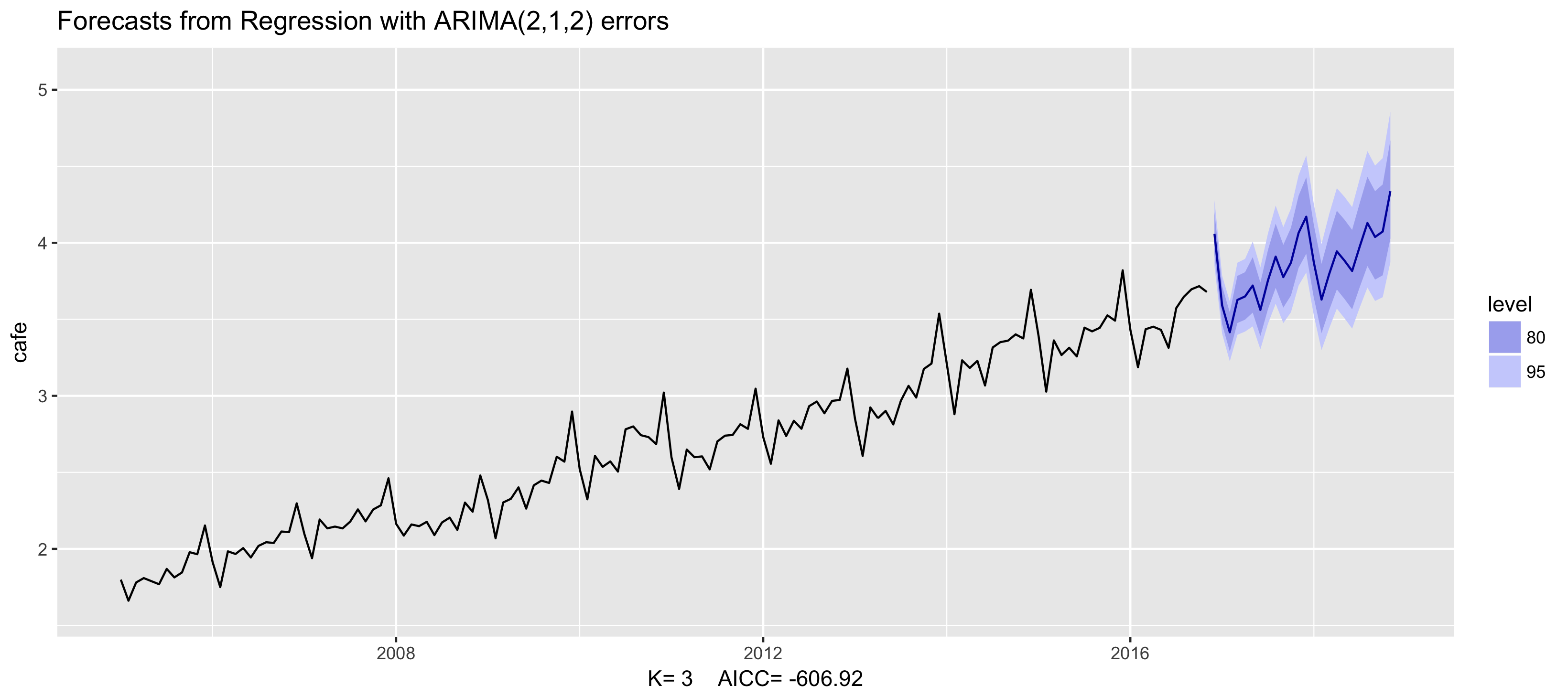

Voorbeeld: Australische cafébestedingen

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 3),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 3, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

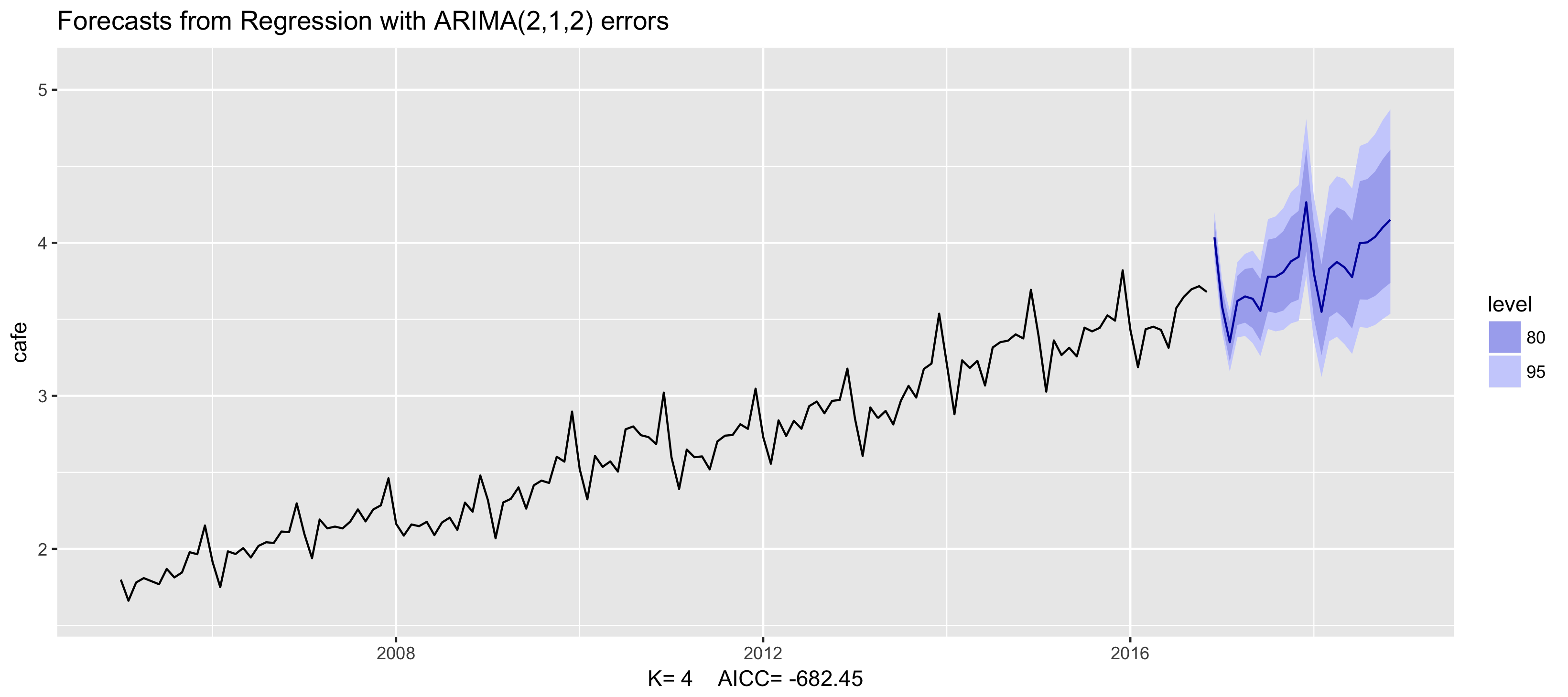

Voorbeeld: Australische cafébestedingen

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 4),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 4, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

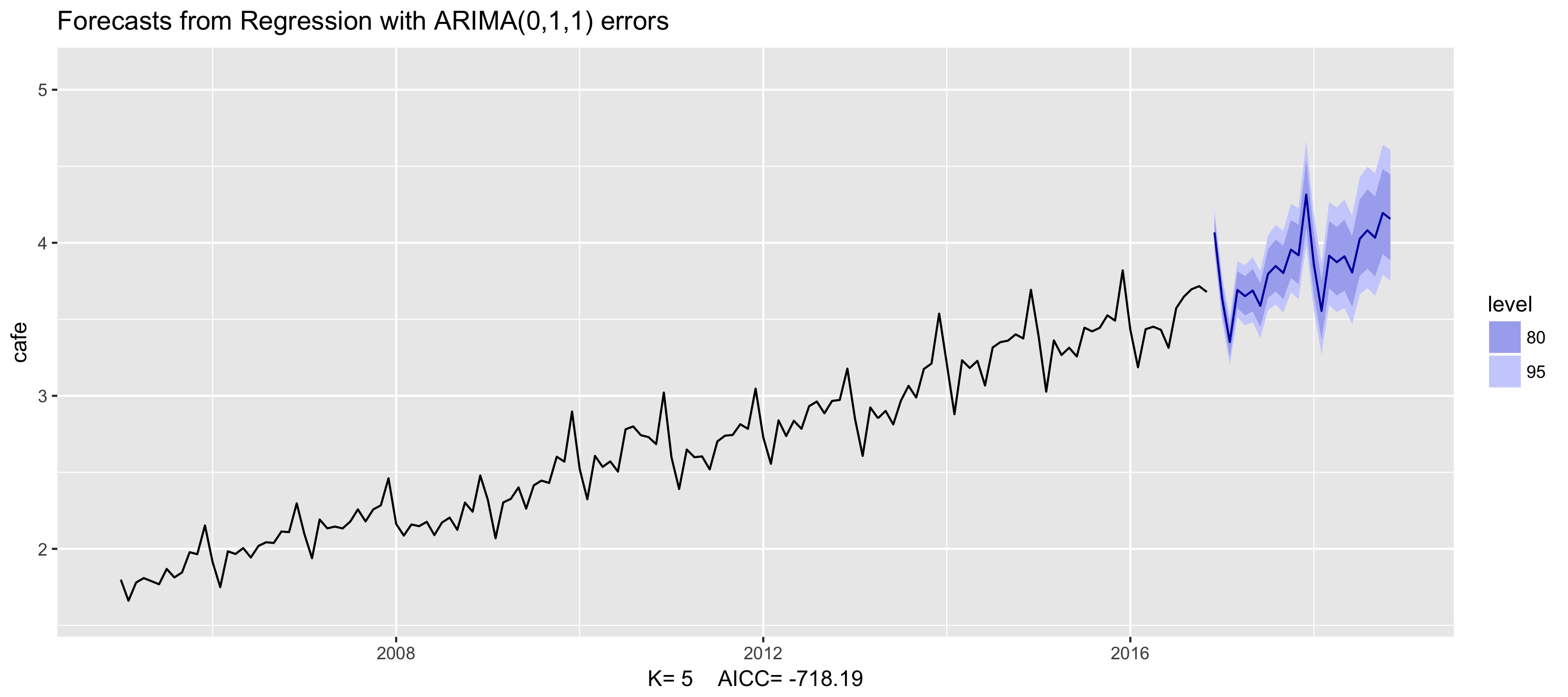

Voorbeeld: Australische cafébestedingen

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 5),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 5, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

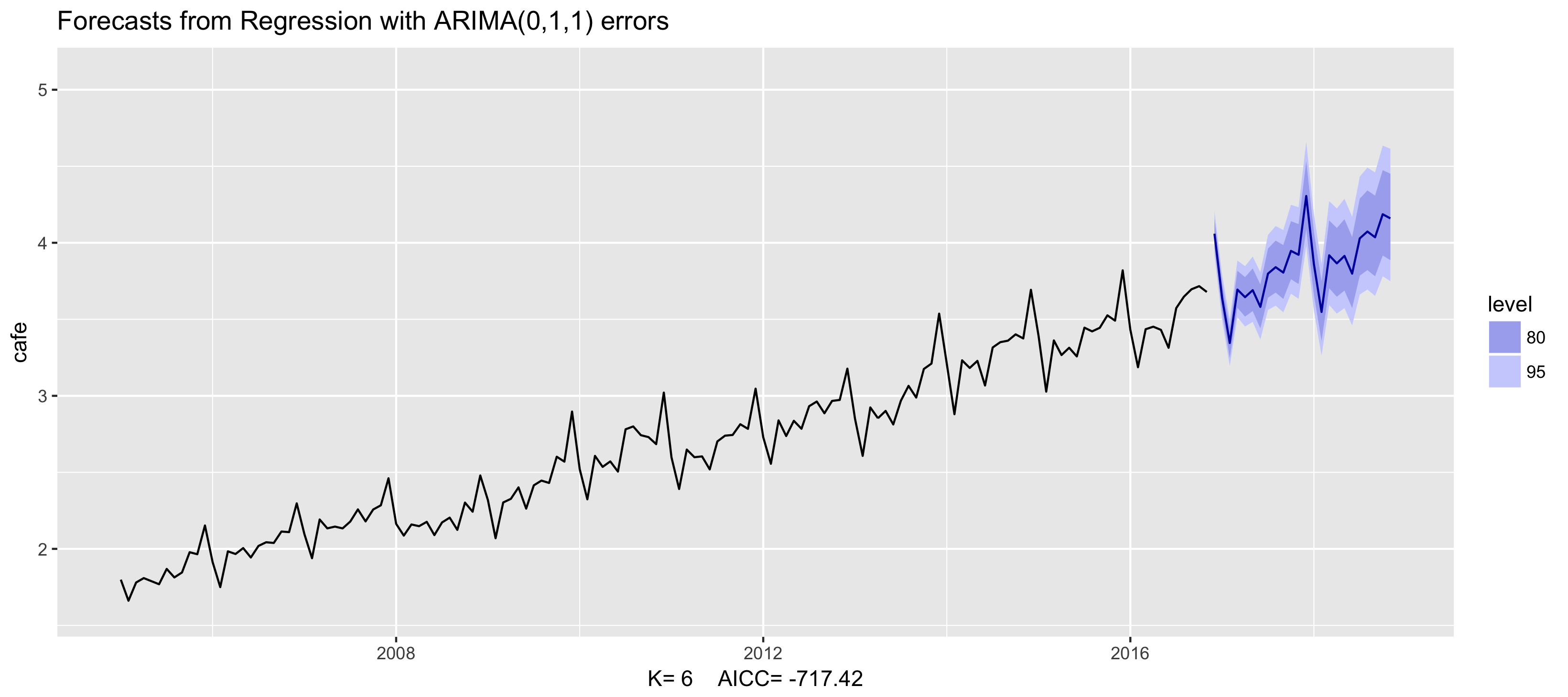

Voorbeeld: Australische cafébestedingen

fit <- auto.arima(cafe, xreg = fourier(cafe, K = 6),

seasonal = FALSE, lambda = 0)

fit %>% forecast(xreg = fourier(cafe, K = 6, h = 24)) %>%

autoplot() + ylim(1.6, 5.1)

Dynamische harmonische regressie

- Andere predictoren kun je ook toevoegen: $x_{t,1},...,x_{t,r}$

- Kies K om de $AIC_c$ te minimaliseren

- K mag niet groter zijn dan m/2

- Vooral nuttig voor wekelijkse, dagelijkse en subdagelijkse data