Exponentially weighted forecasts

Voorspellen in R

Rob J. Hyndman

Professor of Statistics at Monash University

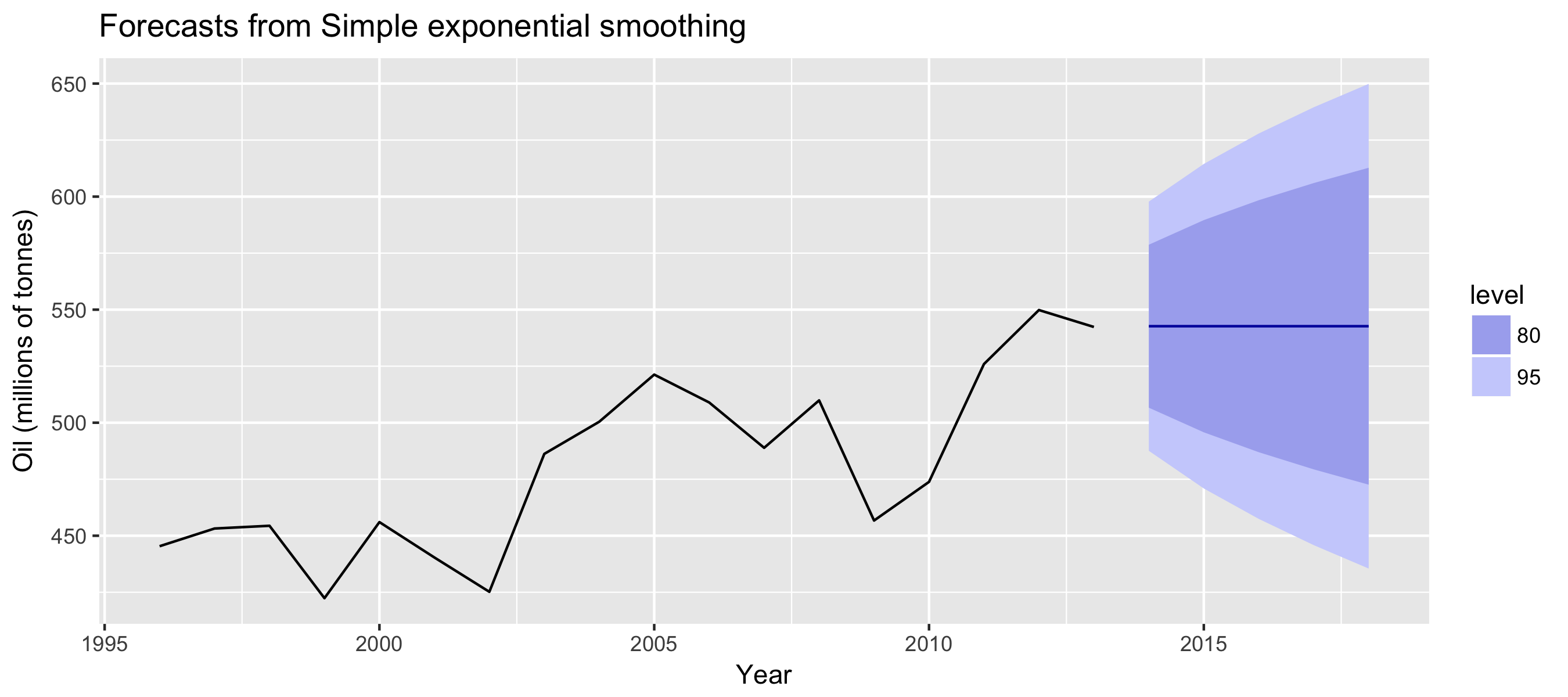

Voorbeeld: olieproductie

autoplot(fc) +

ylab("Olie (miljoen ton)") + xlab("Jaar")

Voorspellen in R

Rob J. Hyndman

Professor of Statistics at Monash University

autoplot(fc) +

ylab("Olie (miljoen ton)") + xlab("Jaar")