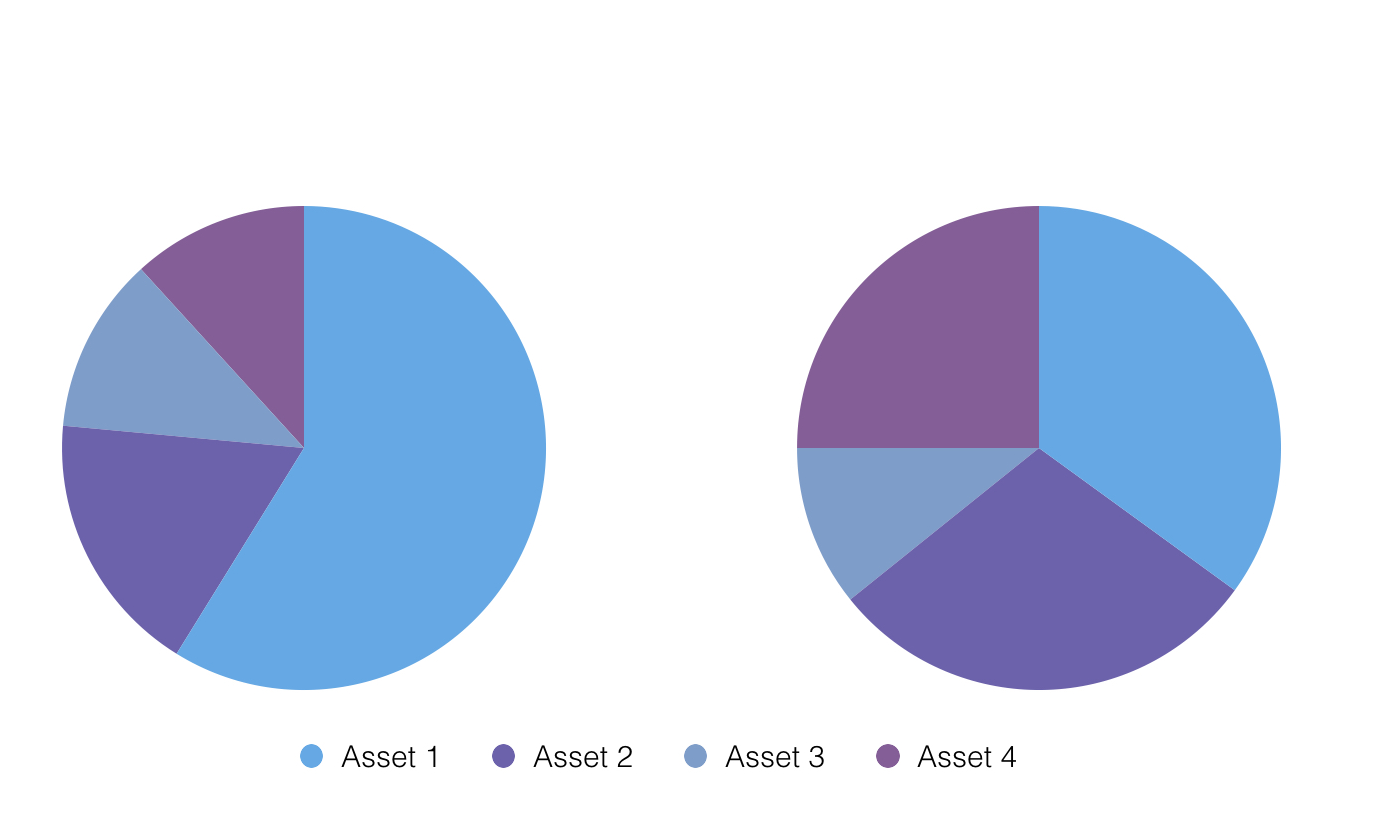

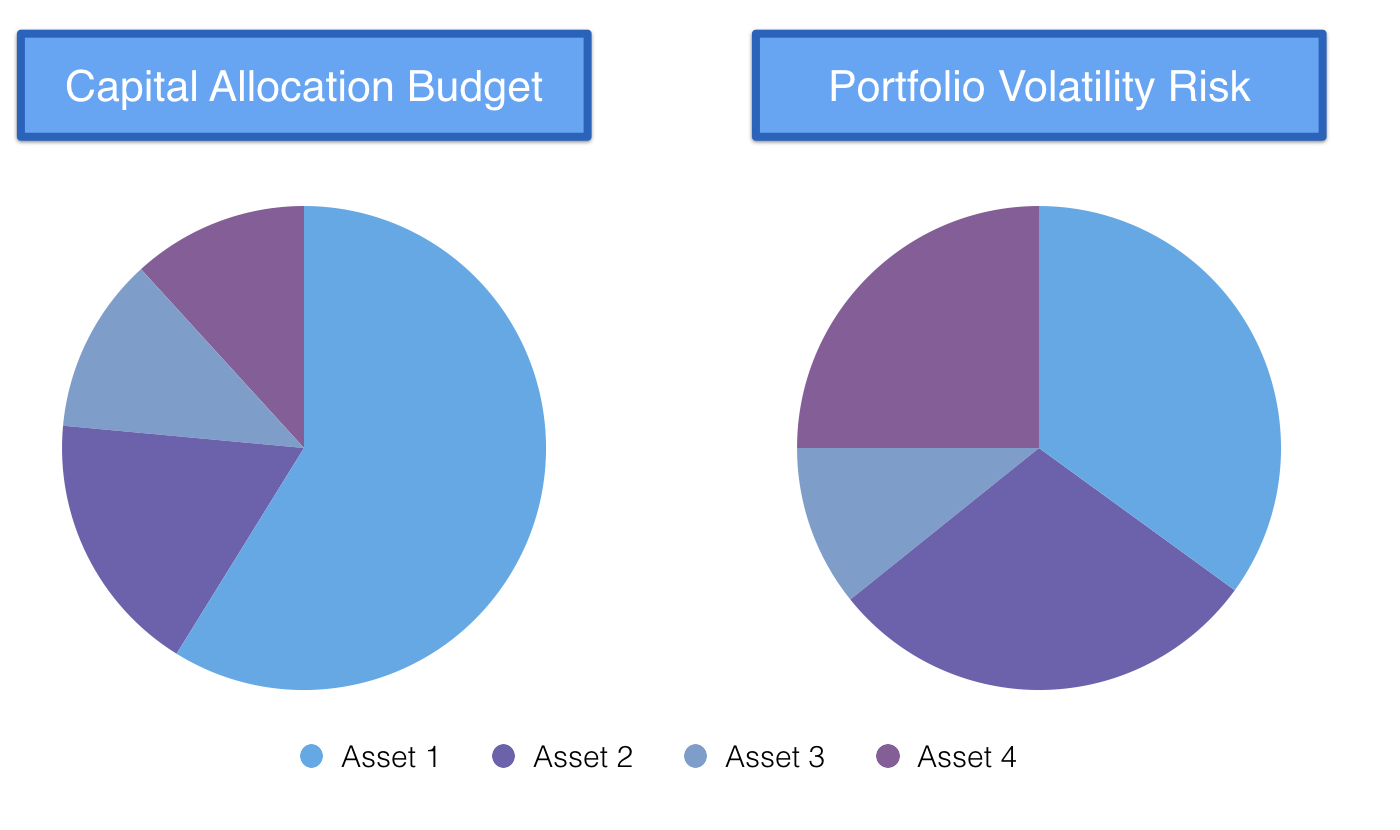

Risicobudget van de portefeuille

Introductie tot portefeuilleanalyse in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

Wie deed het?

Wie deed het?

Introductie tot portefeuilleanalyse in R

Kris Boudt

Professor, Free University Brussels & Amsterdam