De (geannualiseerde) Sharpe-ratio

Introductie tot portefeuilleanalyse in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

Prestaties benchmarken

Prestaties benchmarken

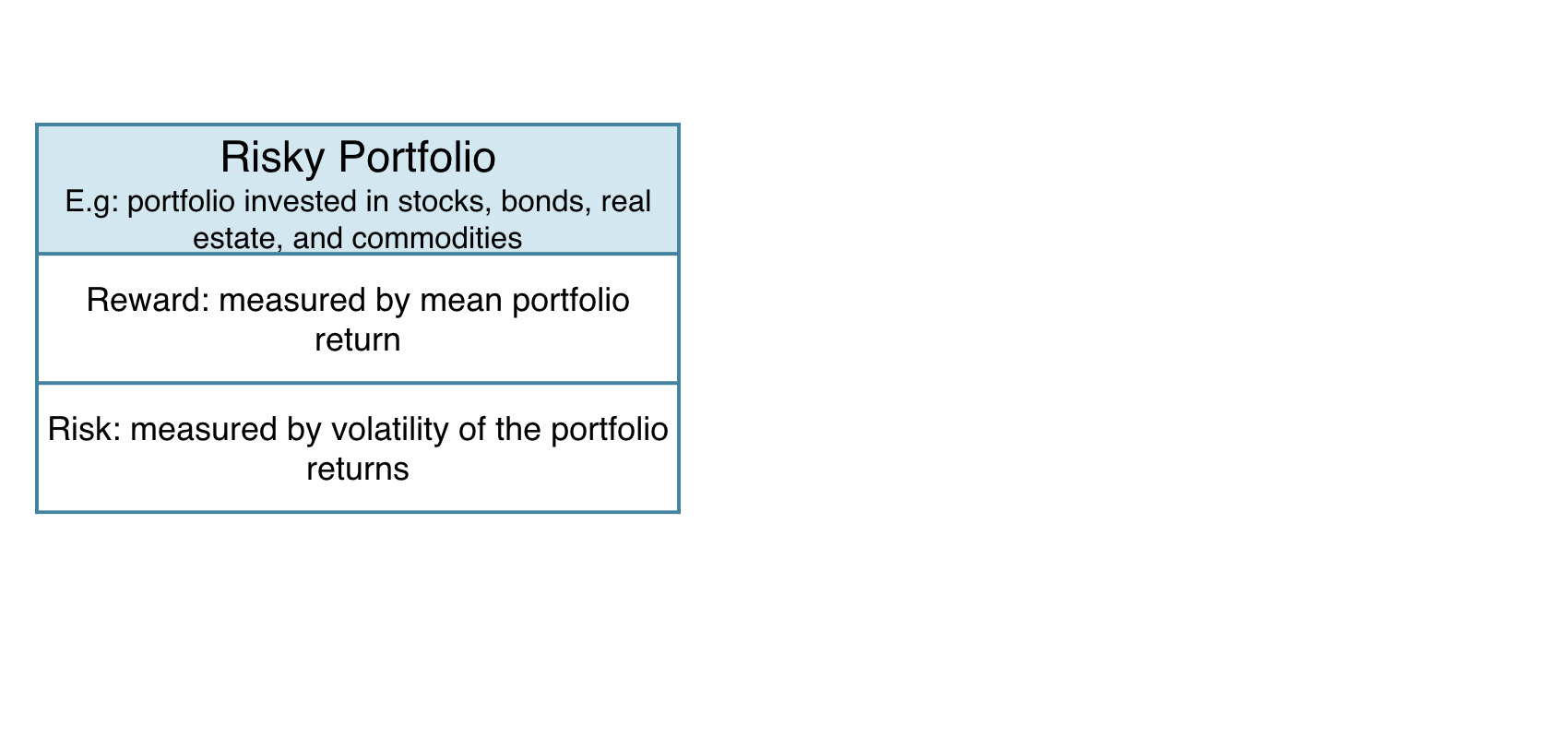

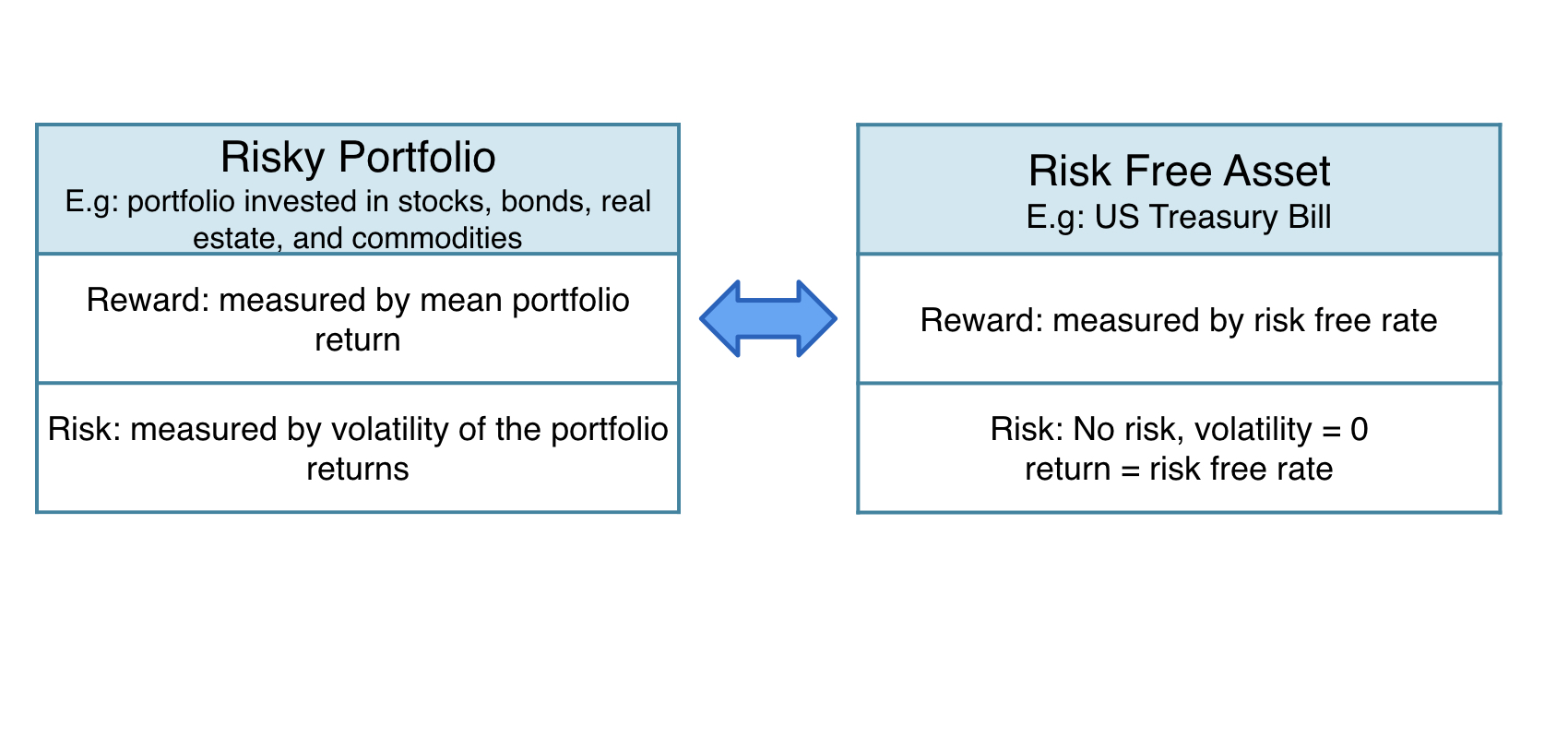

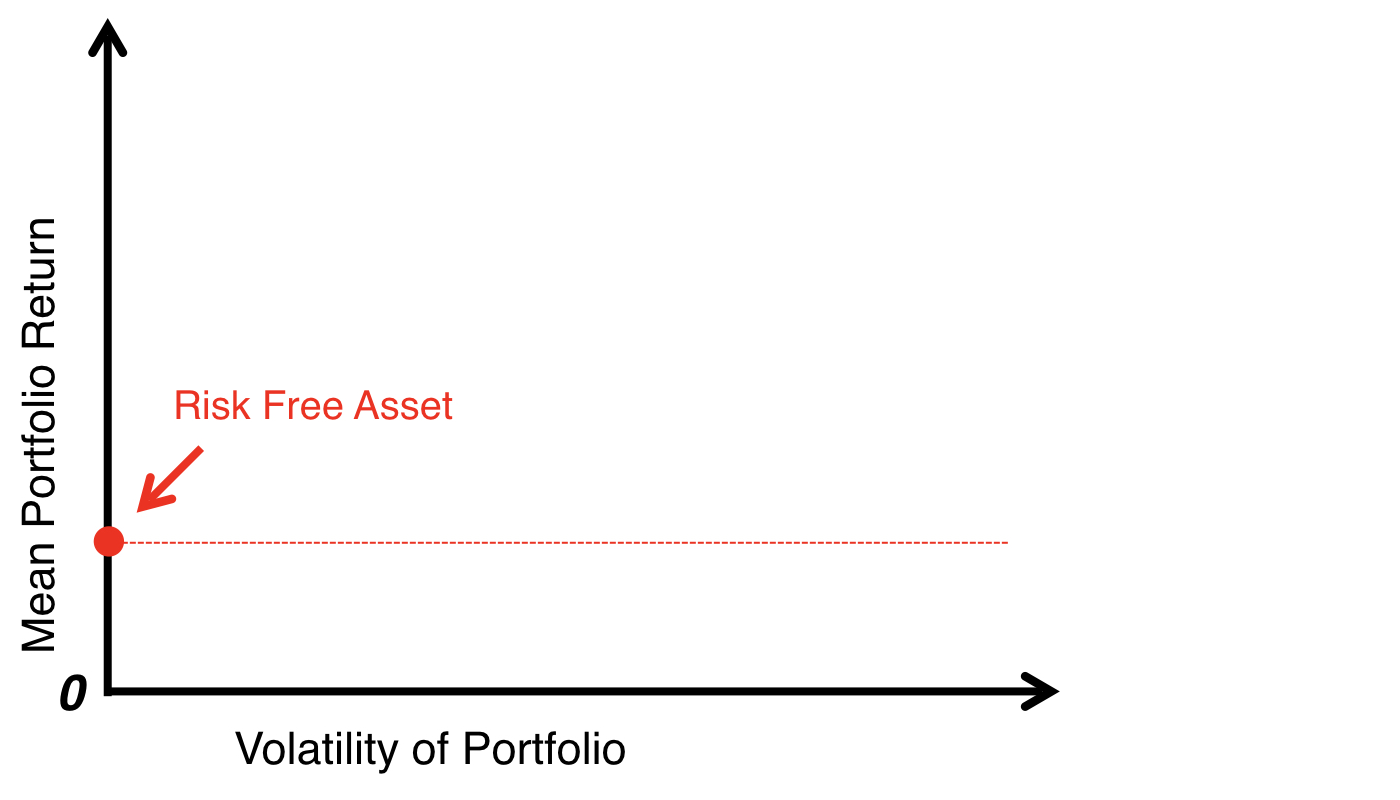

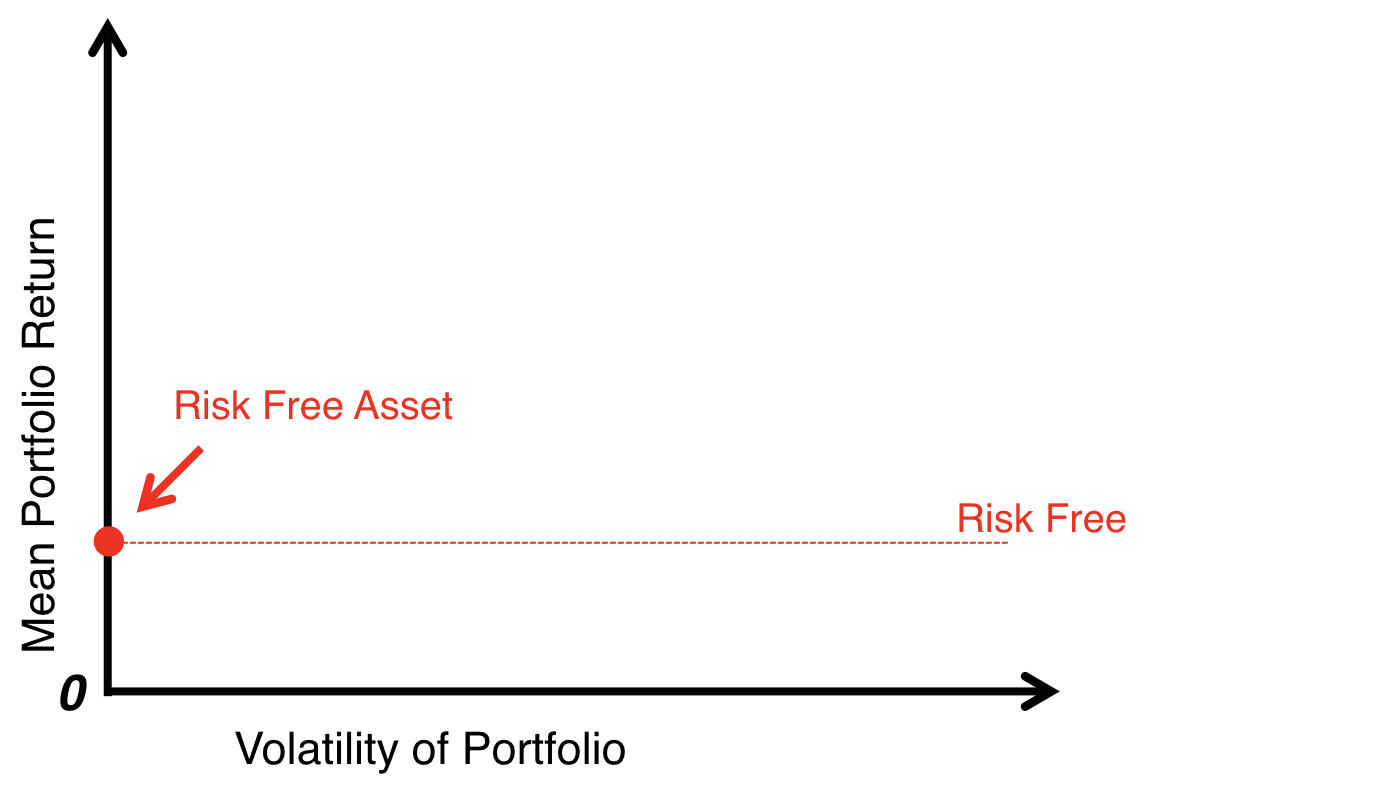

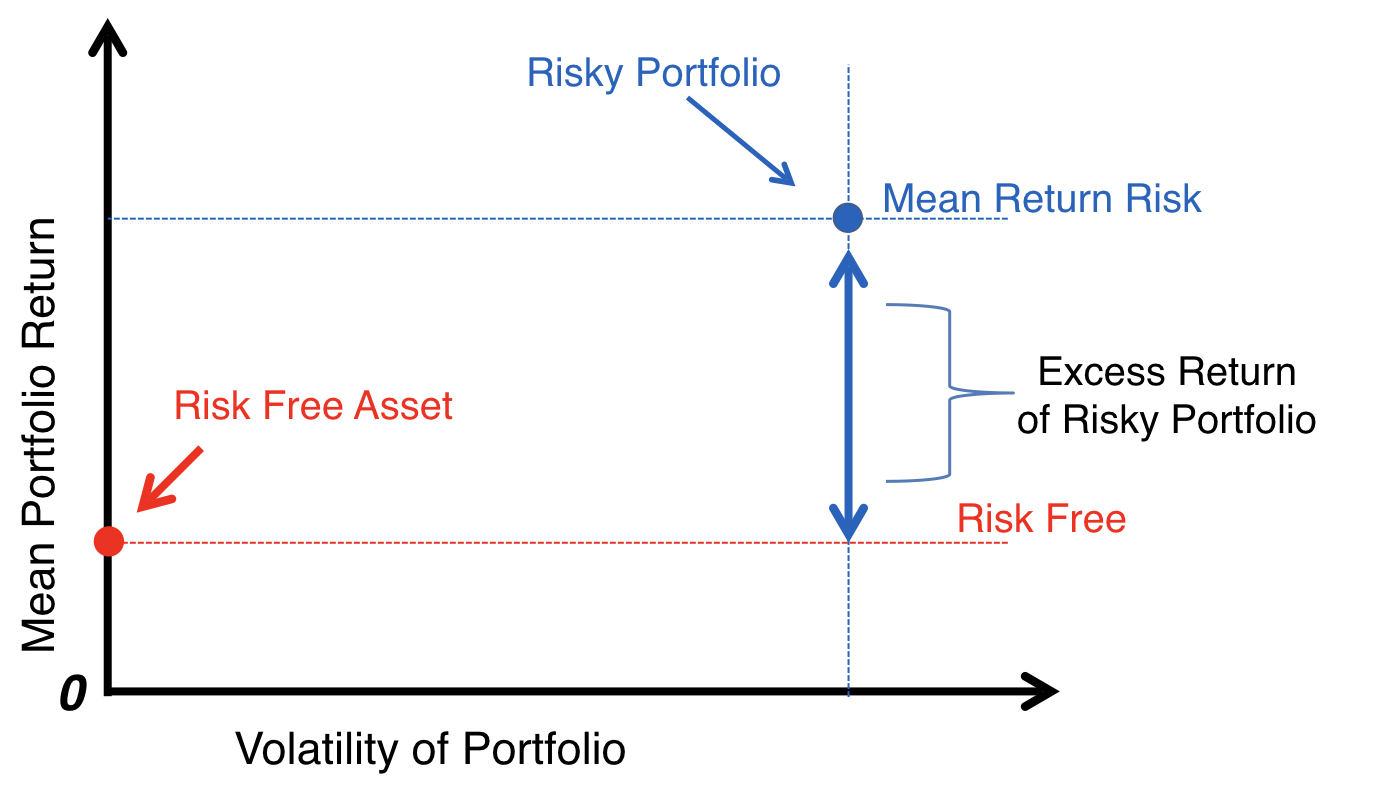

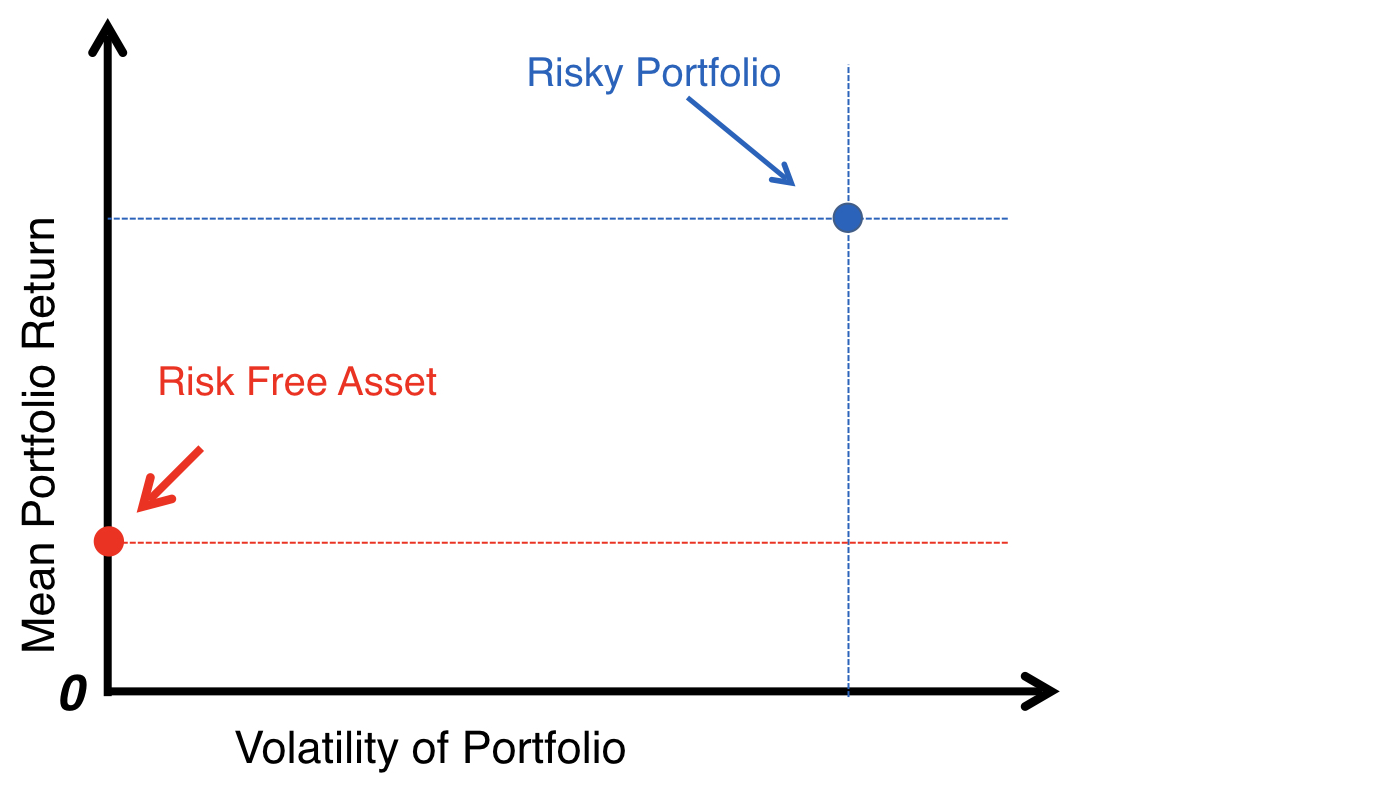

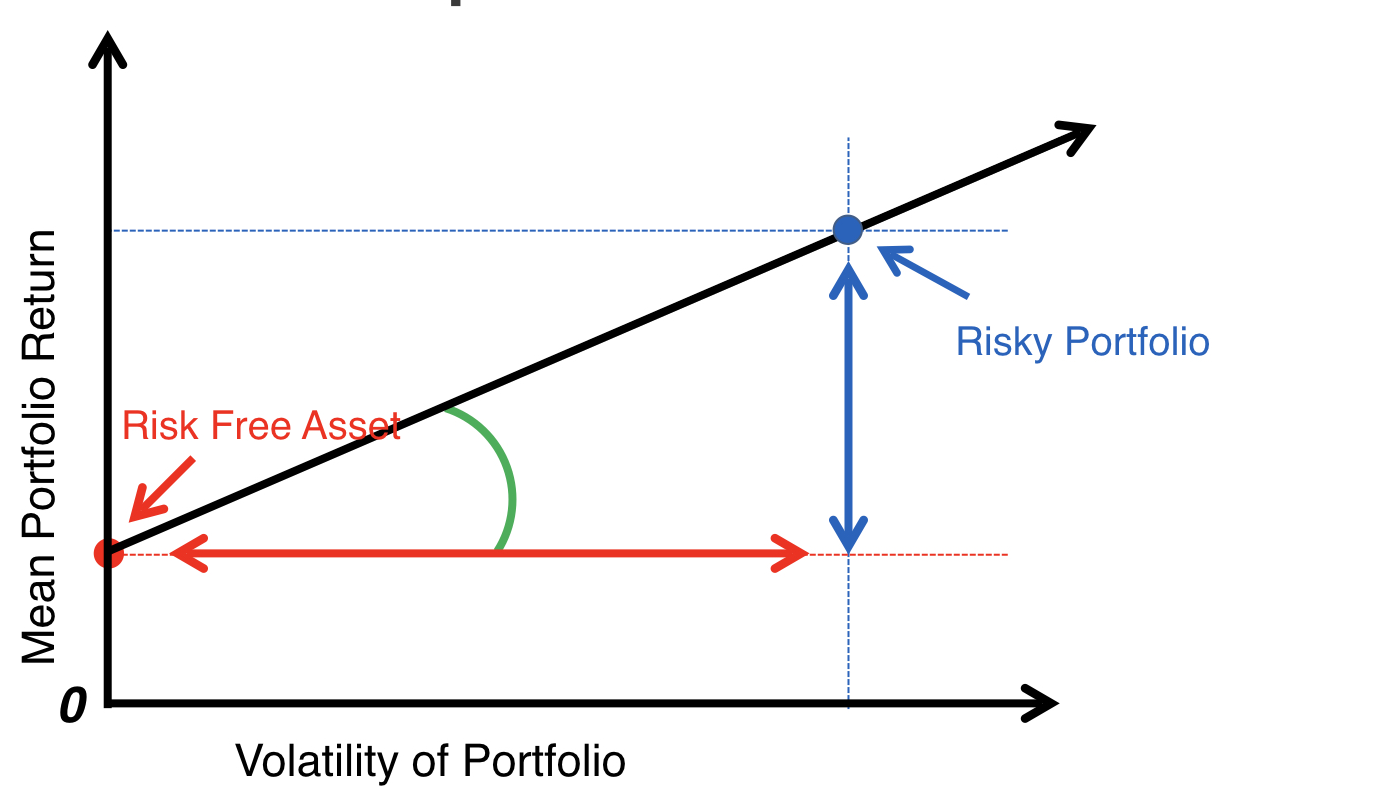

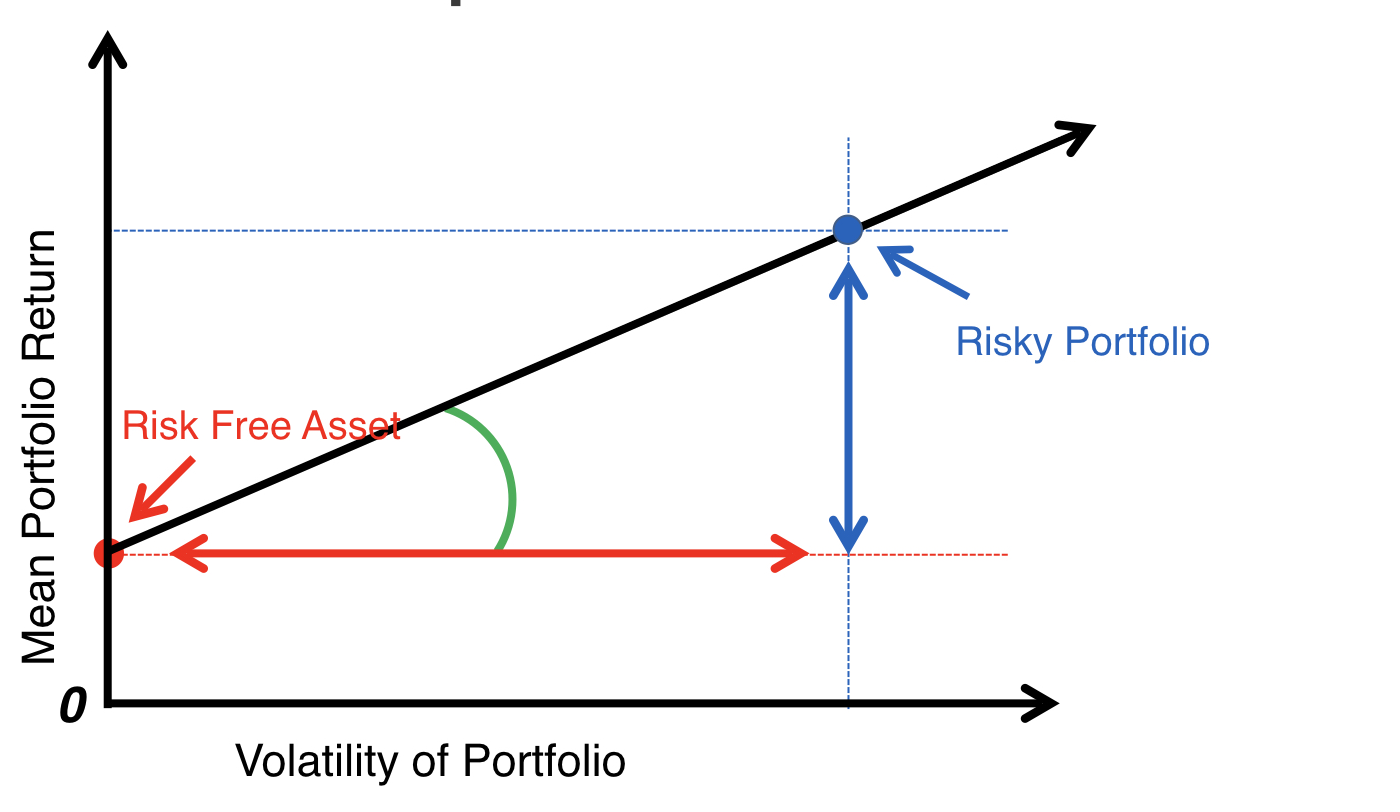

Risico-rendementafweging

Risico-rendementafweging

Risico-rendementafweging

Risico-rendementafweging

Risico-rendementafweging

Risico-rendementafweging

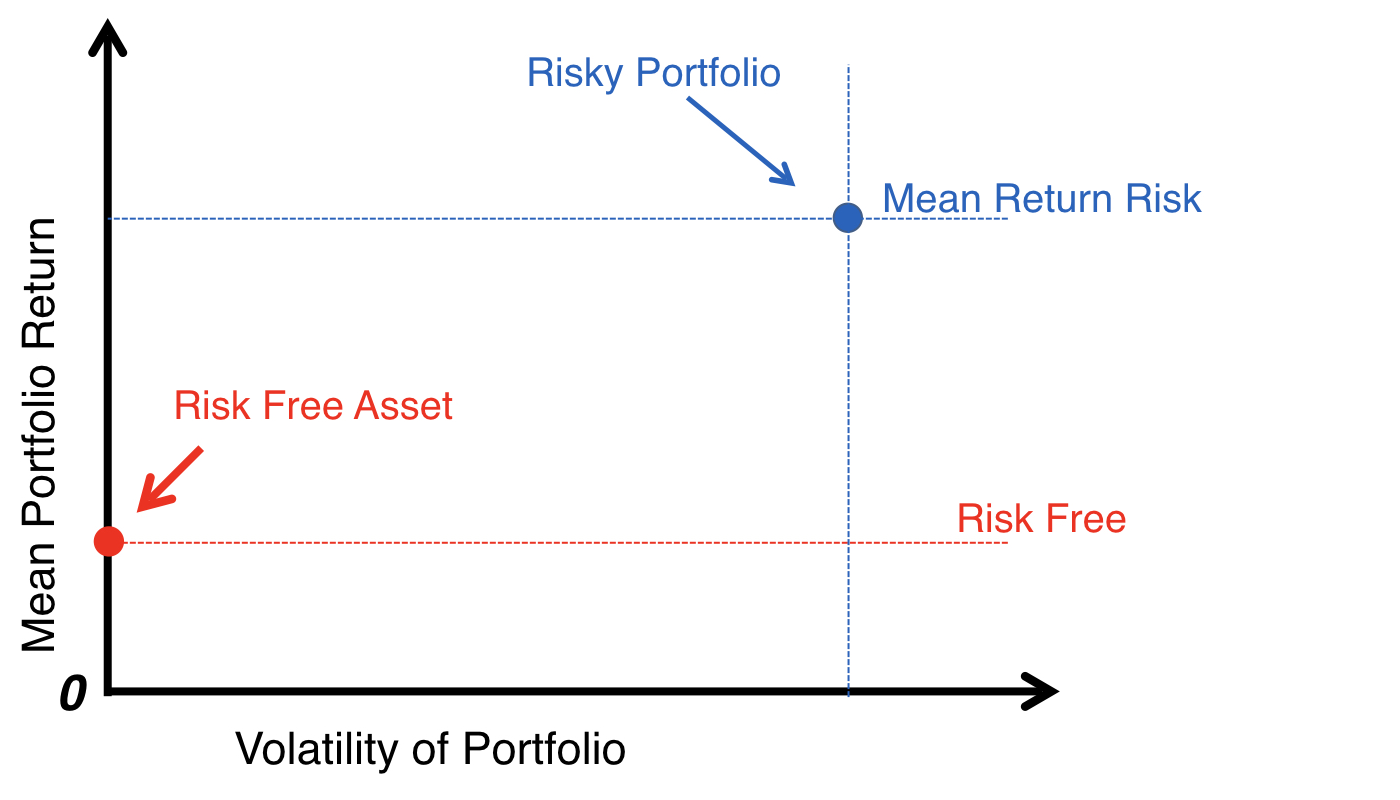

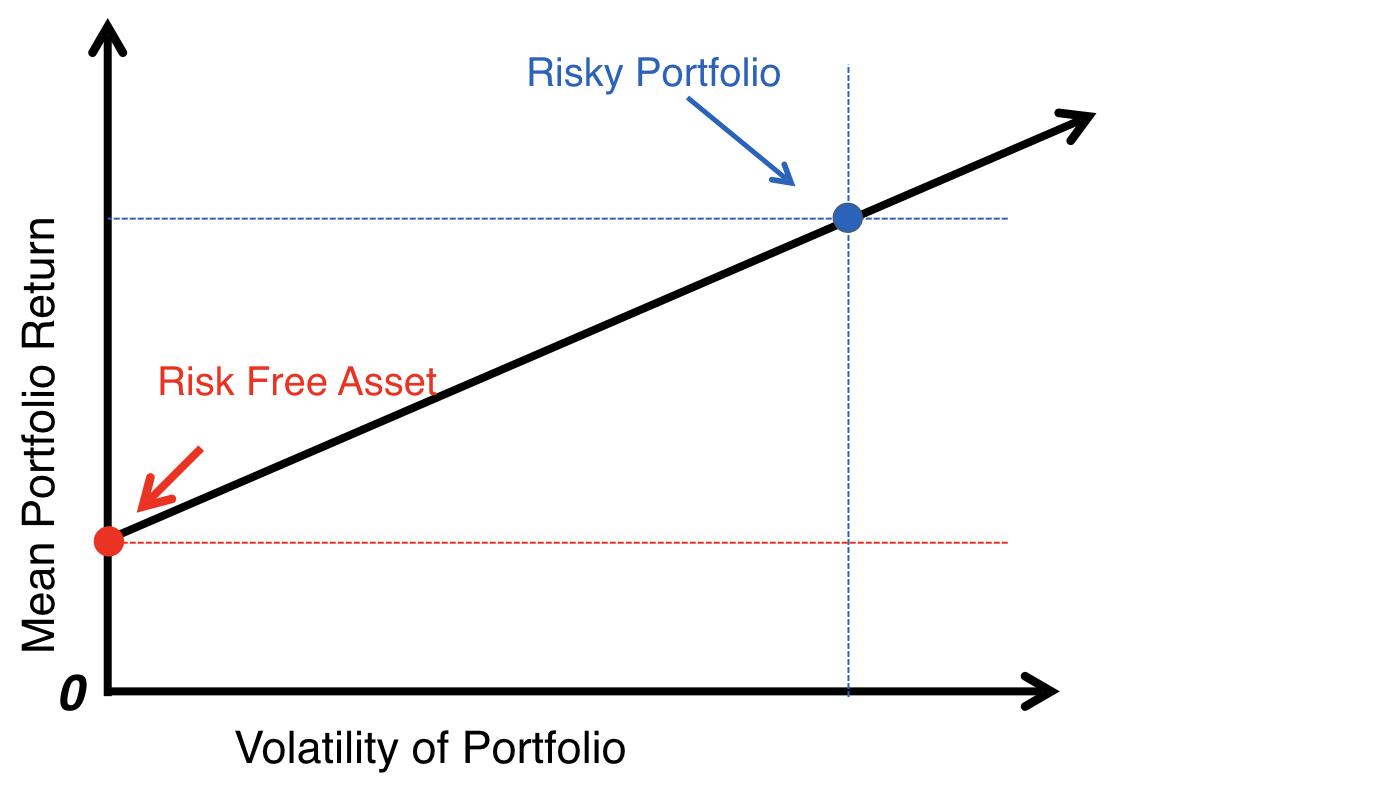

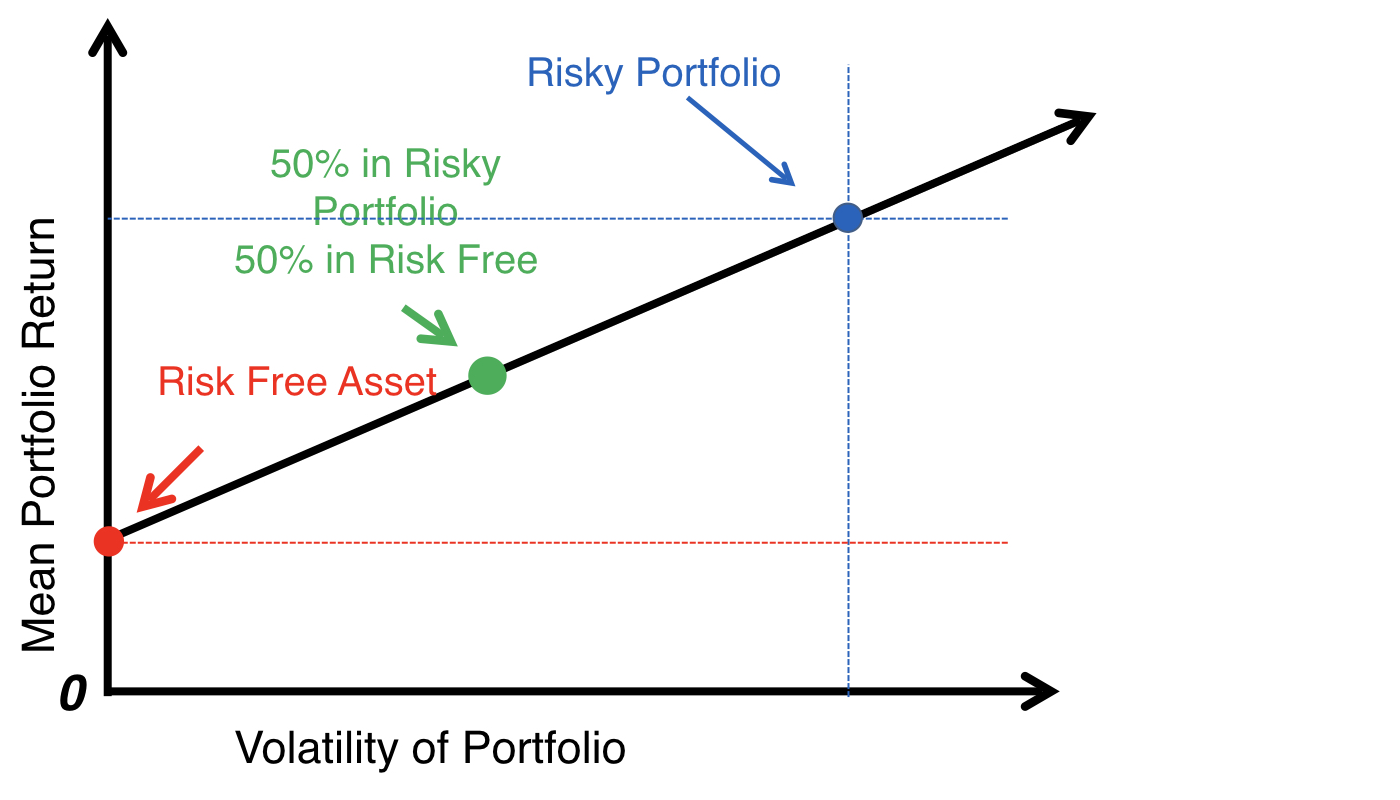

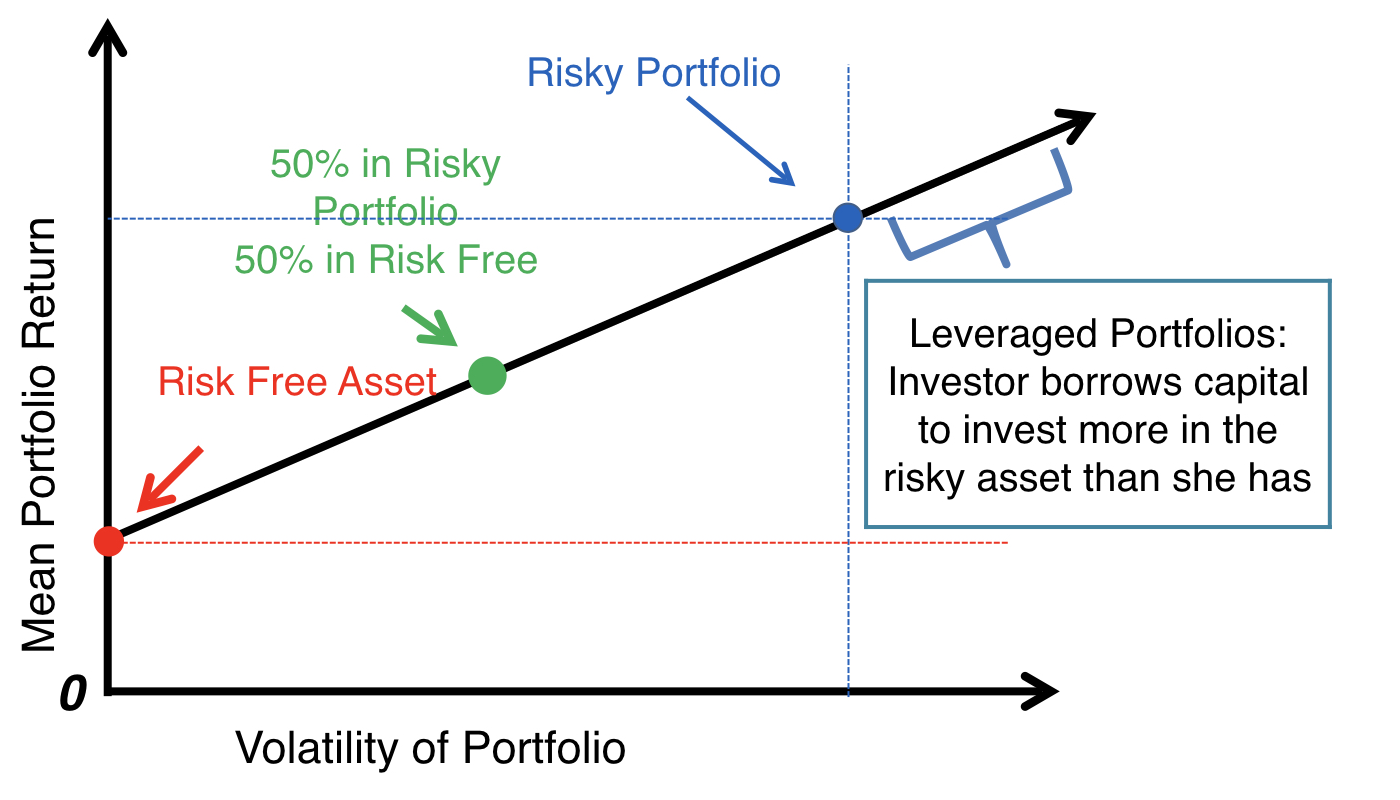

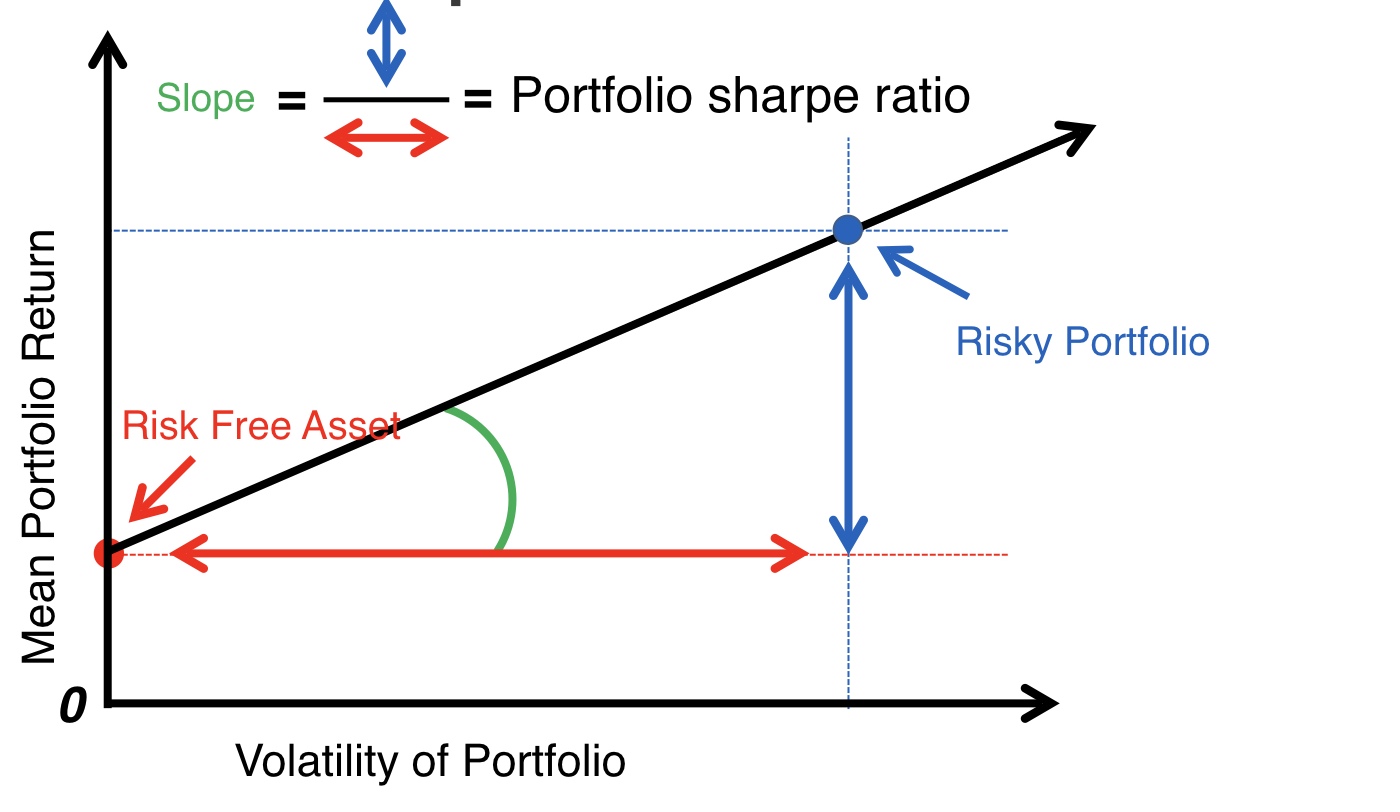

Kapitaalallocatielijn

Kapitaalallocatielijn

Kapitaalallocatielijn

Kapitaalallocatielijn

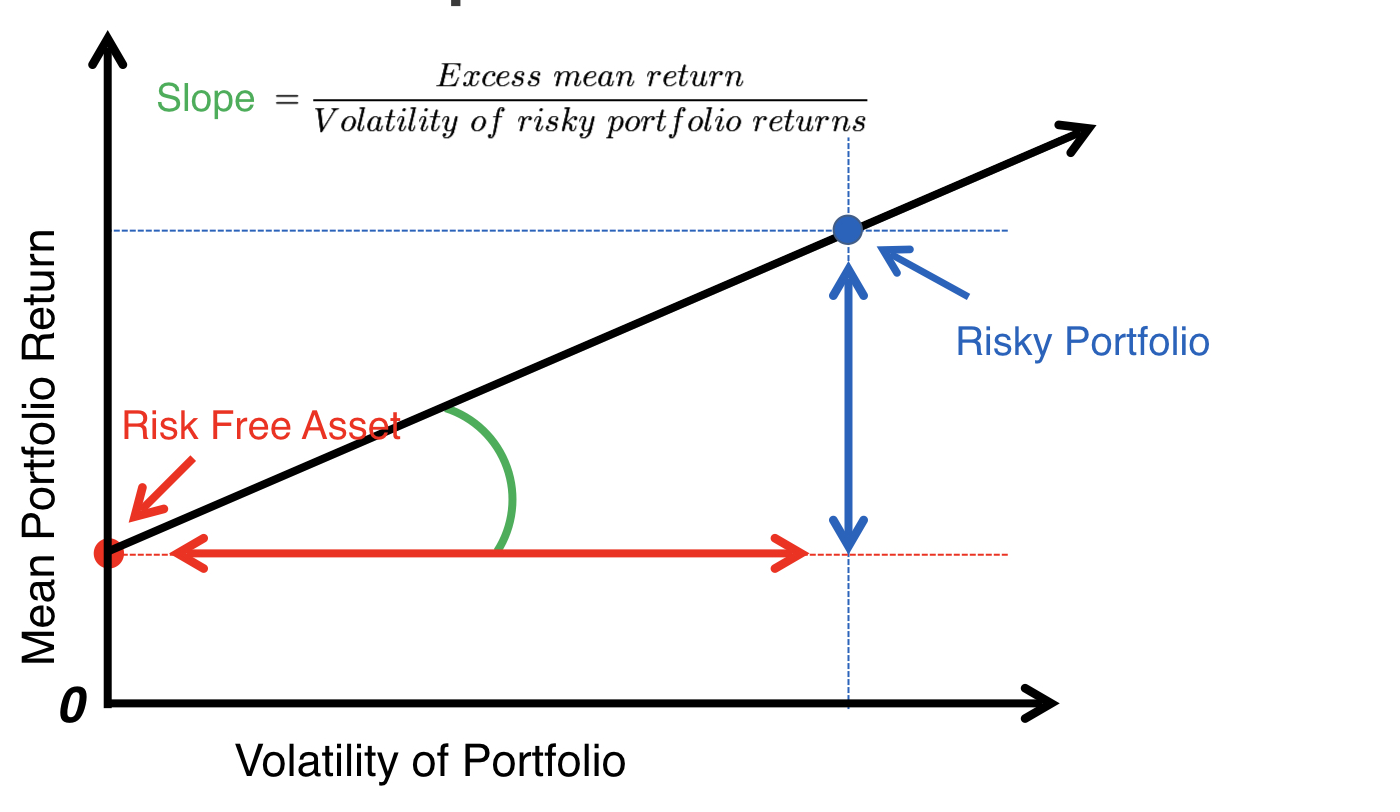

De Sharpe-ratio

De Sharpe-ratio

De Sharpe-ratio

De Sharpe-ratio

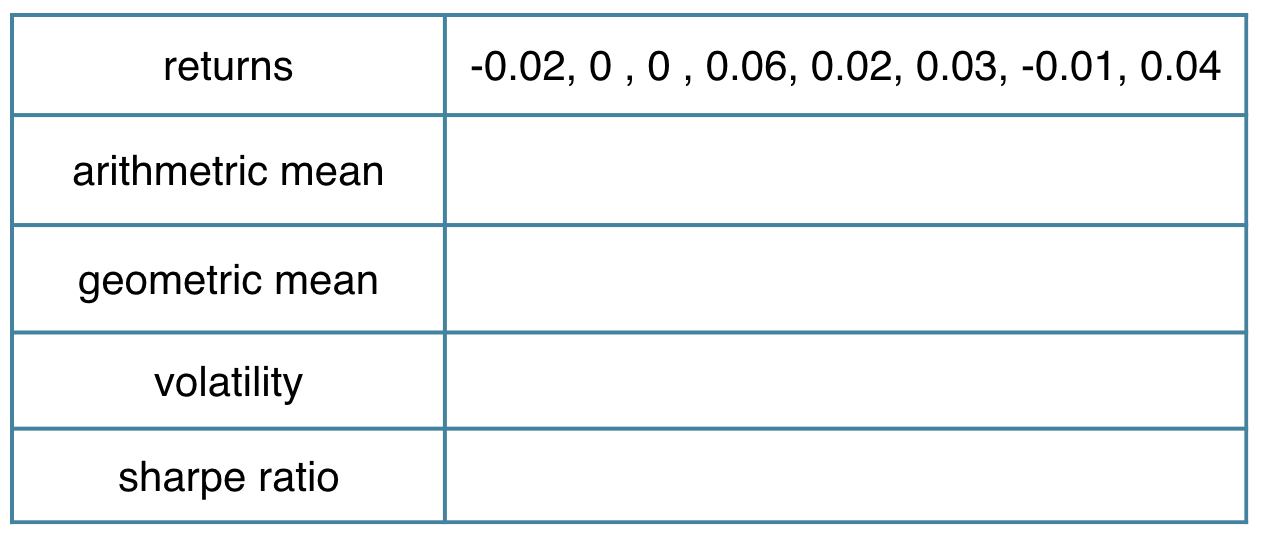

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c(-0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c(-0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

mean(sample_returns)

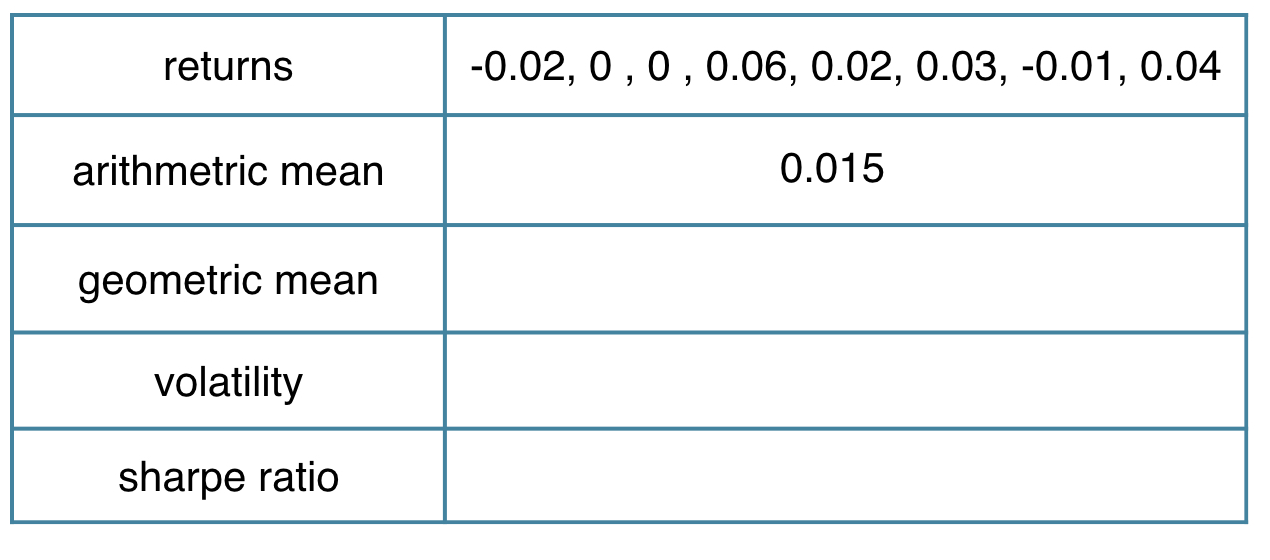

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c(-0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

mean.geometric(sample_returns)

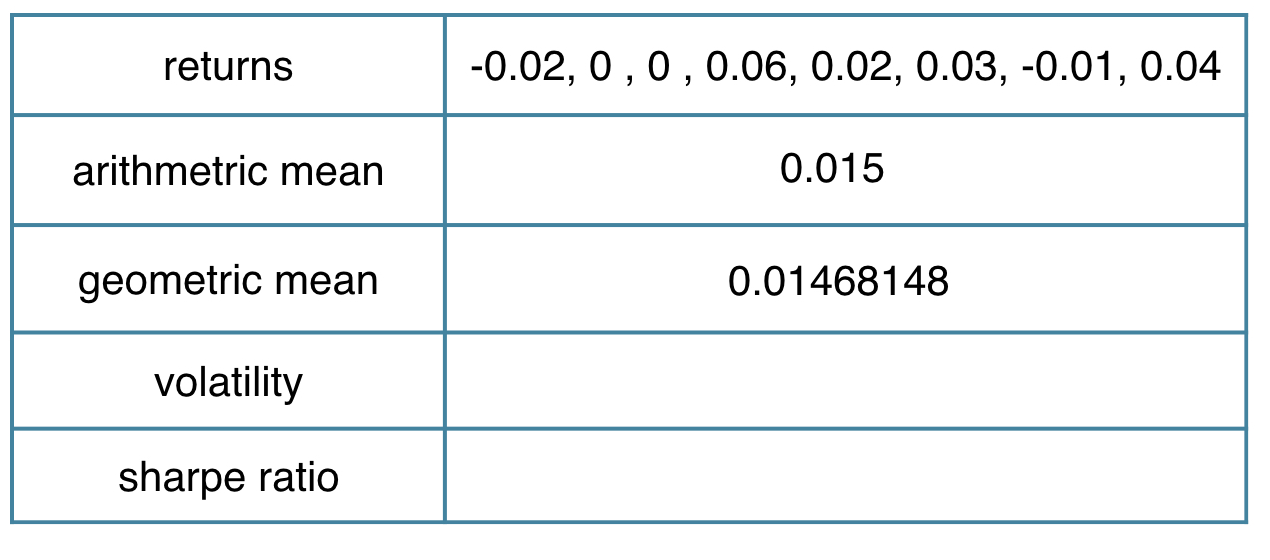

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c(-0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

StdDev(sample_returns)

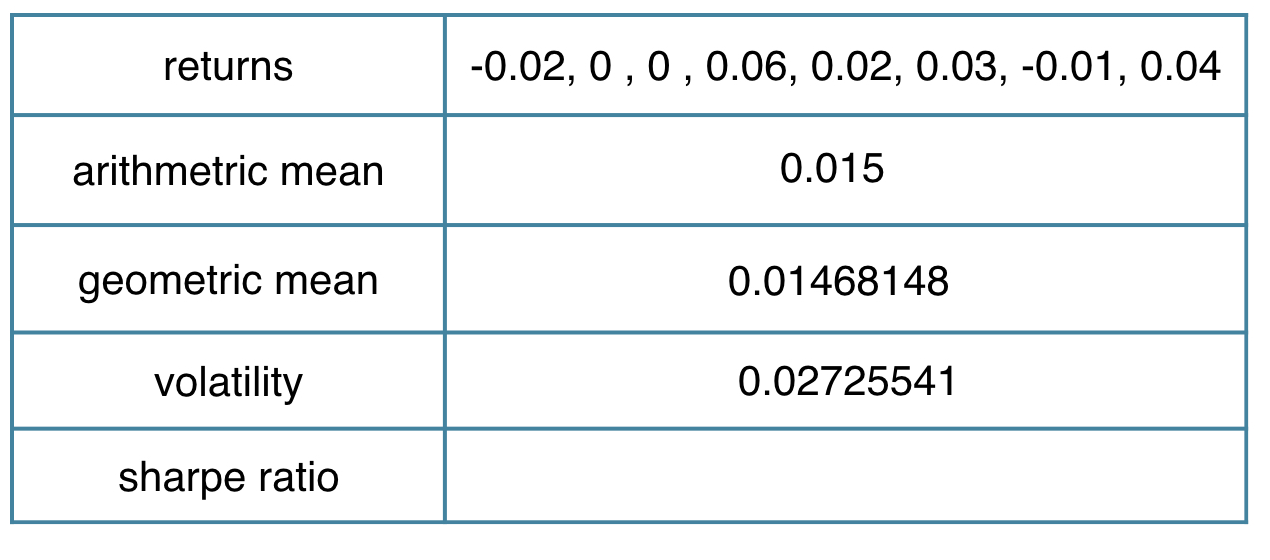

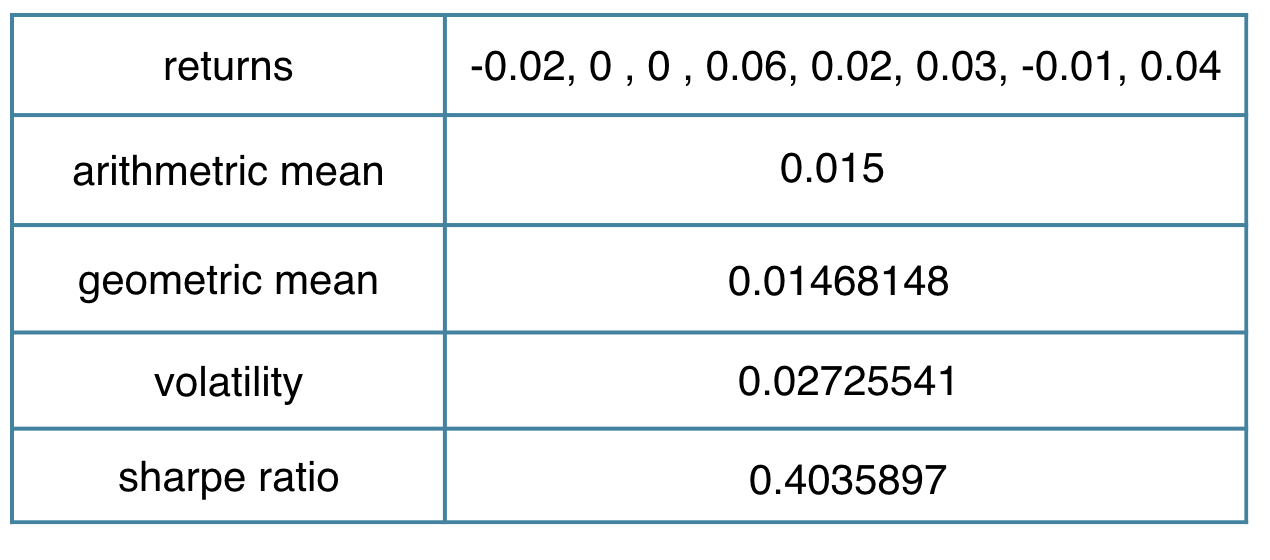

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c(-0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

(mean(sample_returns)-0.004)/StdDev(sample_returns)

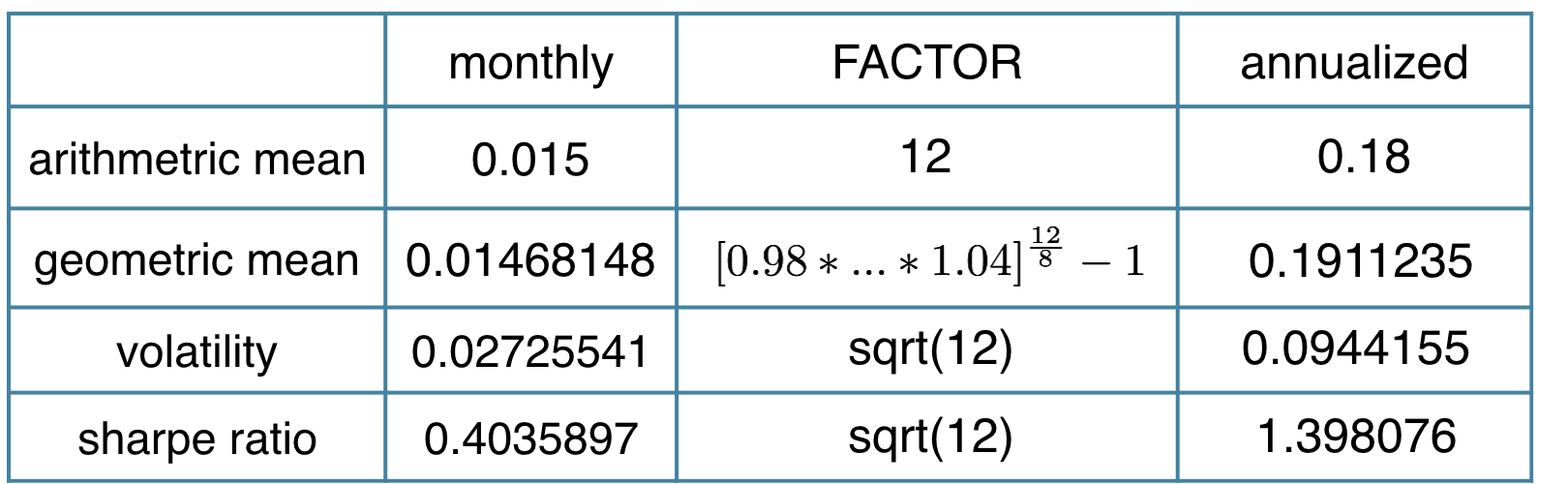

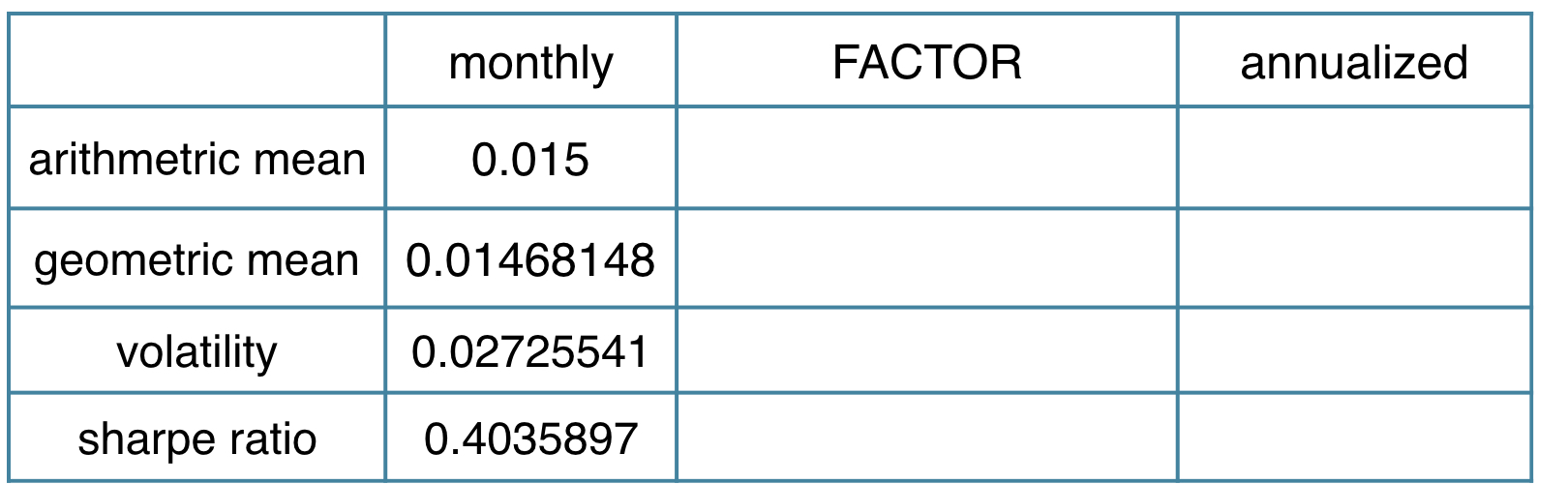

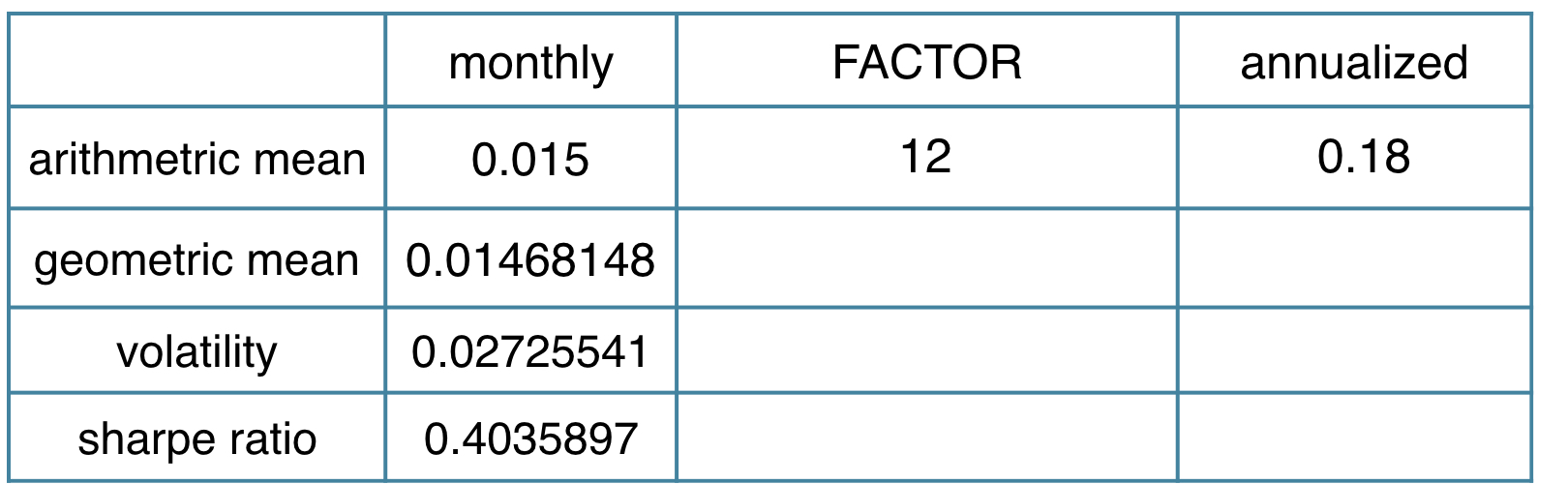

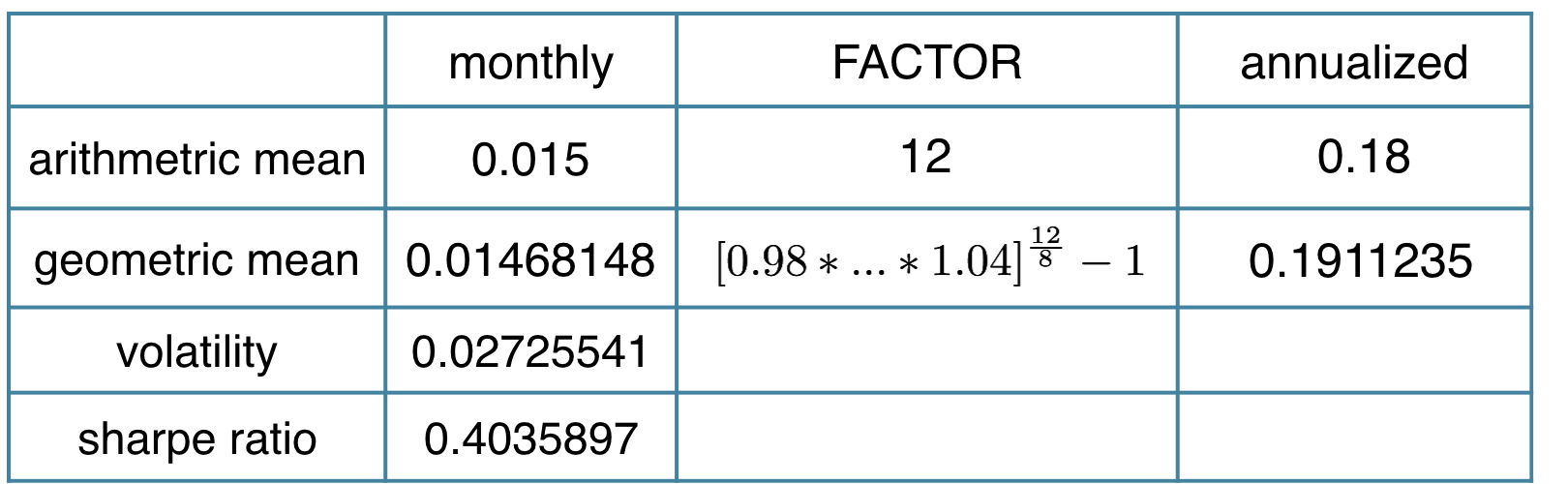

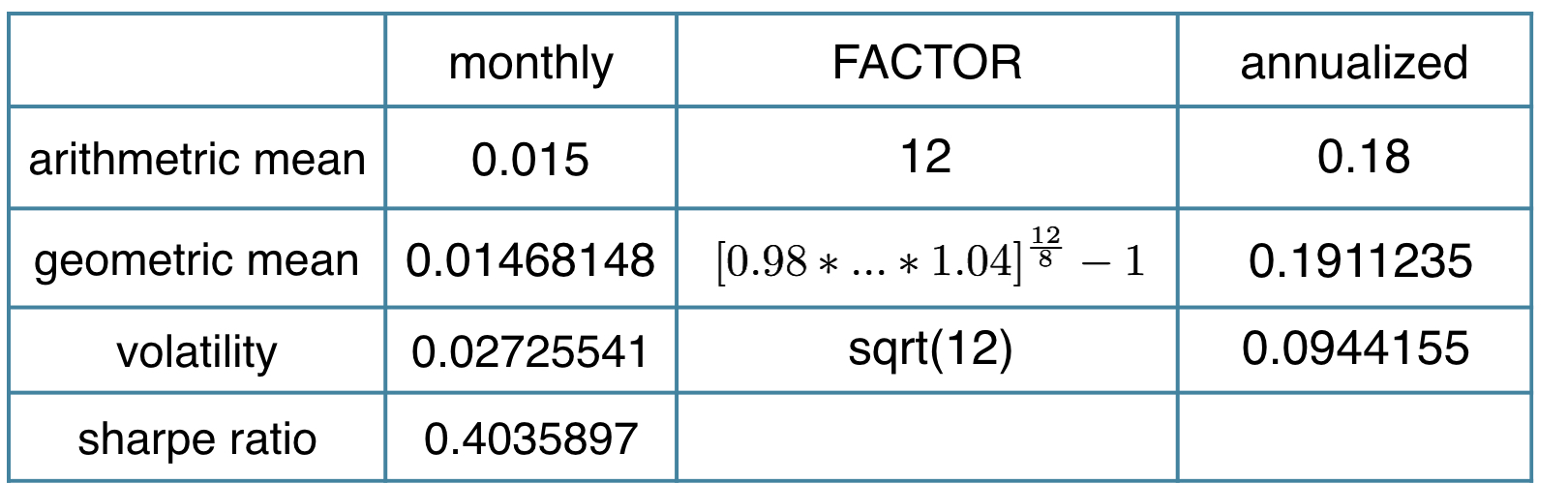

Maandprestaties annualiseren

- Rekenkundig gemiddelde: maandgemiddelde * 12

- Meetkundig gemiddelde, als $R_i$ maandrendementen zijn:

- $[(1+R_1)\cdot(1+R_2)\cdot...\cdot(1+R_T)]^{12/T} -1$

- Volatiliteit: maandvolatiliteit * sqrt(12)

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c( -0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c( -0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

Return.annualized(sample_returns, scale = 12, geometric = FALSE)

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c( -0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

Return.annualized(sample_returns, scale = 12, geometric = TRUE)

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c( -0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

Std.Dev.annualized(sample_returns, scale = 12)

Prestatiestatistieken in actie

library(PerformanceAnalytics)

sample_returns <- c( -0.02, 0.00, 0.00, 0.06, 0.02, 0.03, -0.01, 0.04)

Return.annualized(sample_returns, scale = 12)/

Std.Dev.annualized(sample_returns, scale = 12)