Drijfveren bij twee assets

Introductie tot portefeuilleanalyse in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

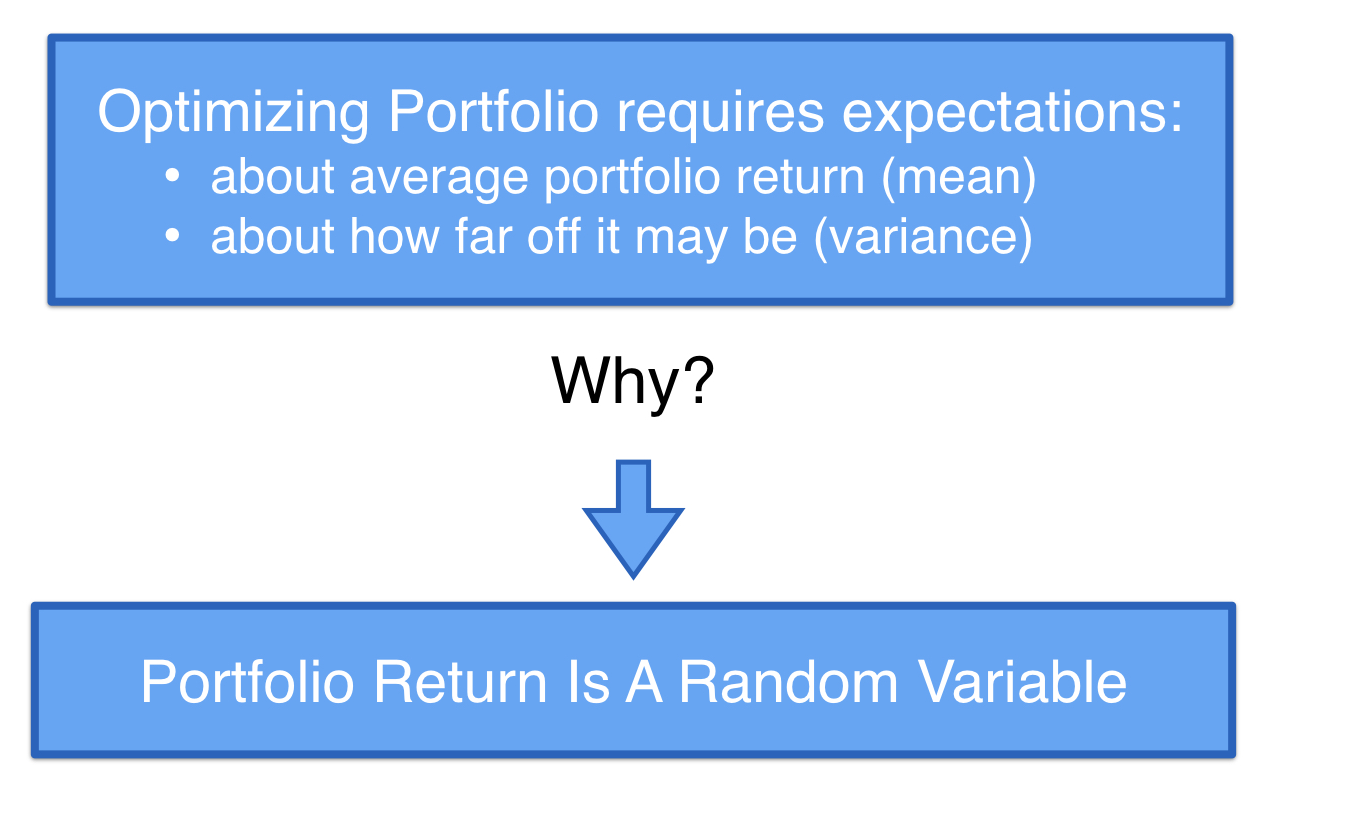

Toekomstige rendementen zijn willekeurig

Toekomstige rendementen zijn willekeurig

Toekomstige rendementen zijn willekeurig

Toekomstige rendementen zijn willekeurig

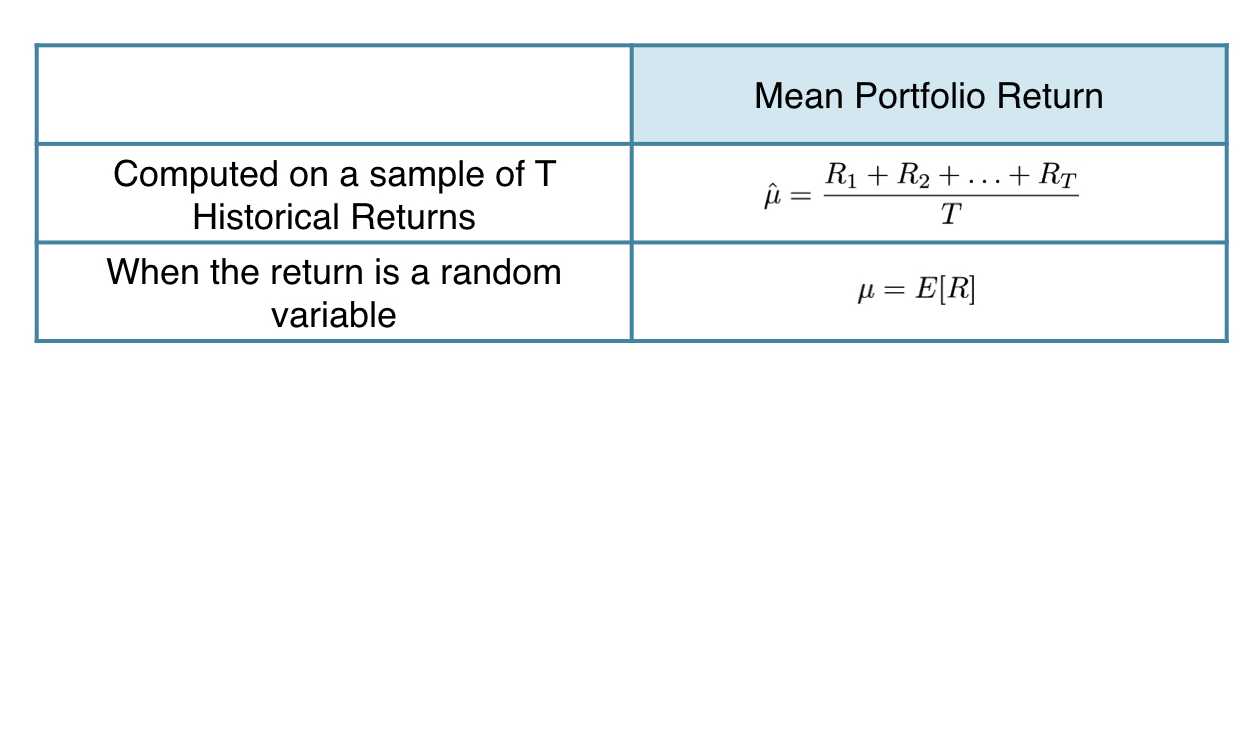

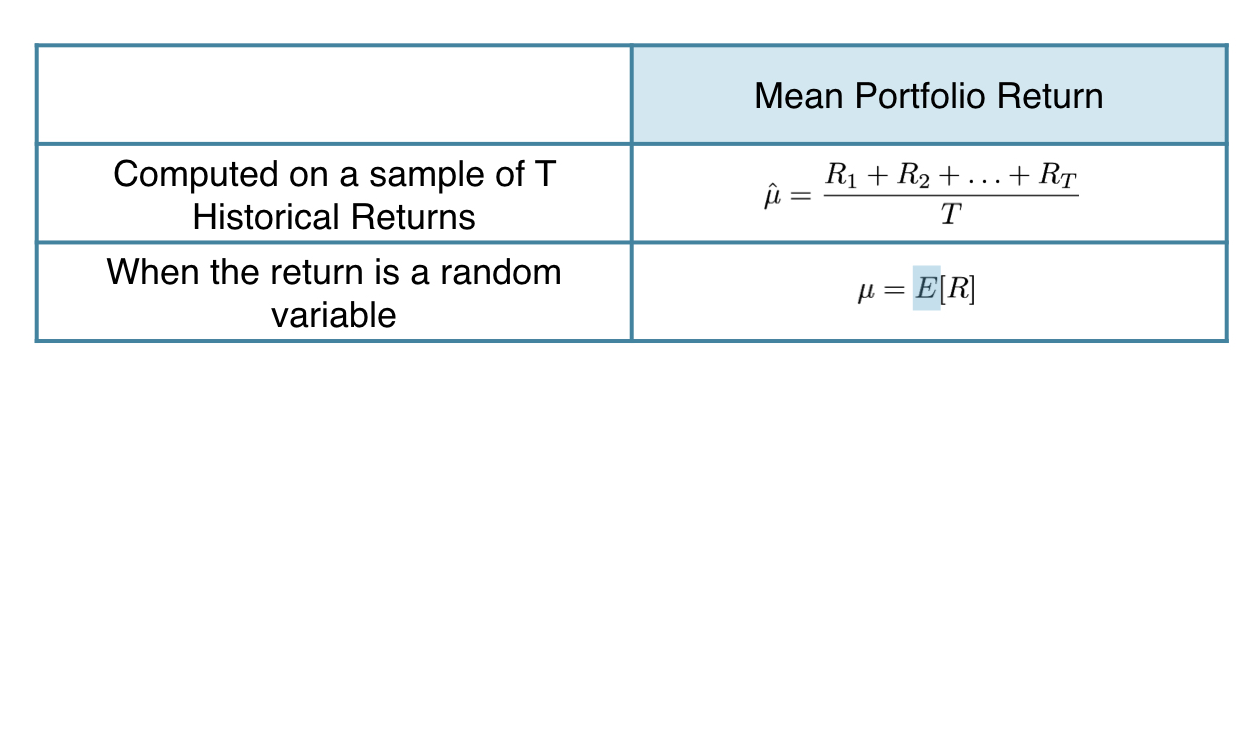

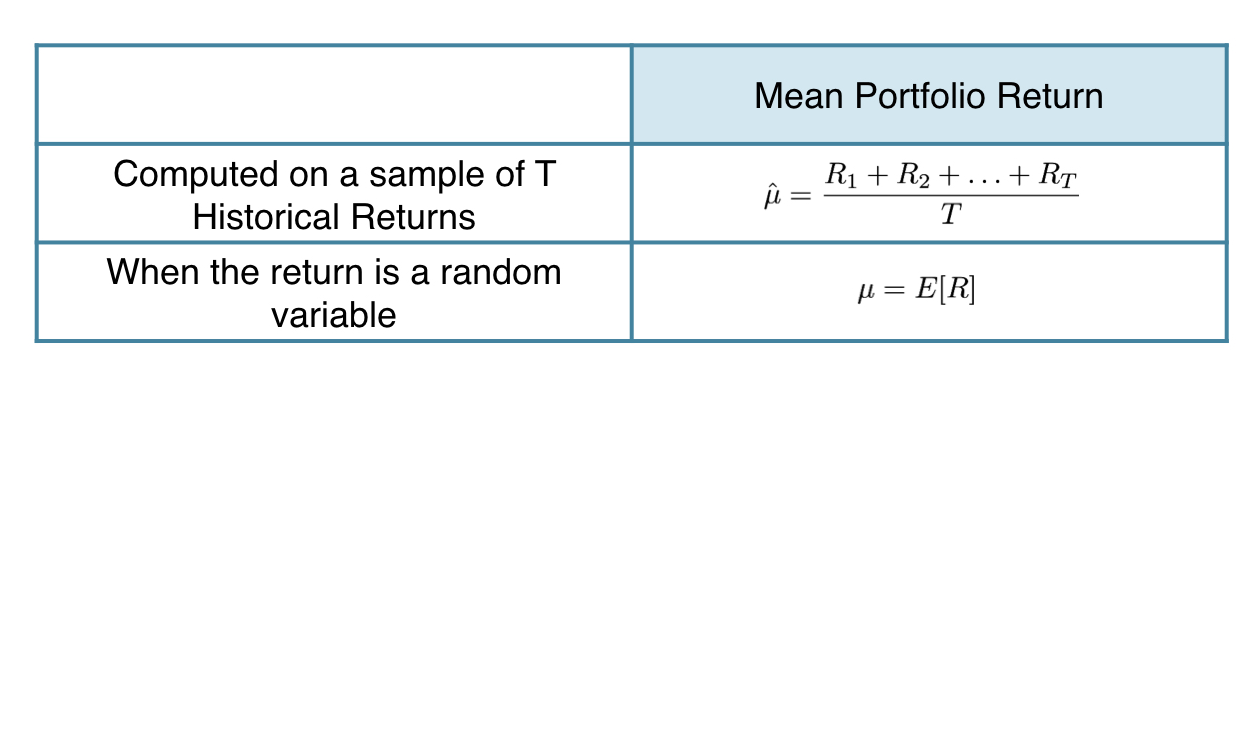

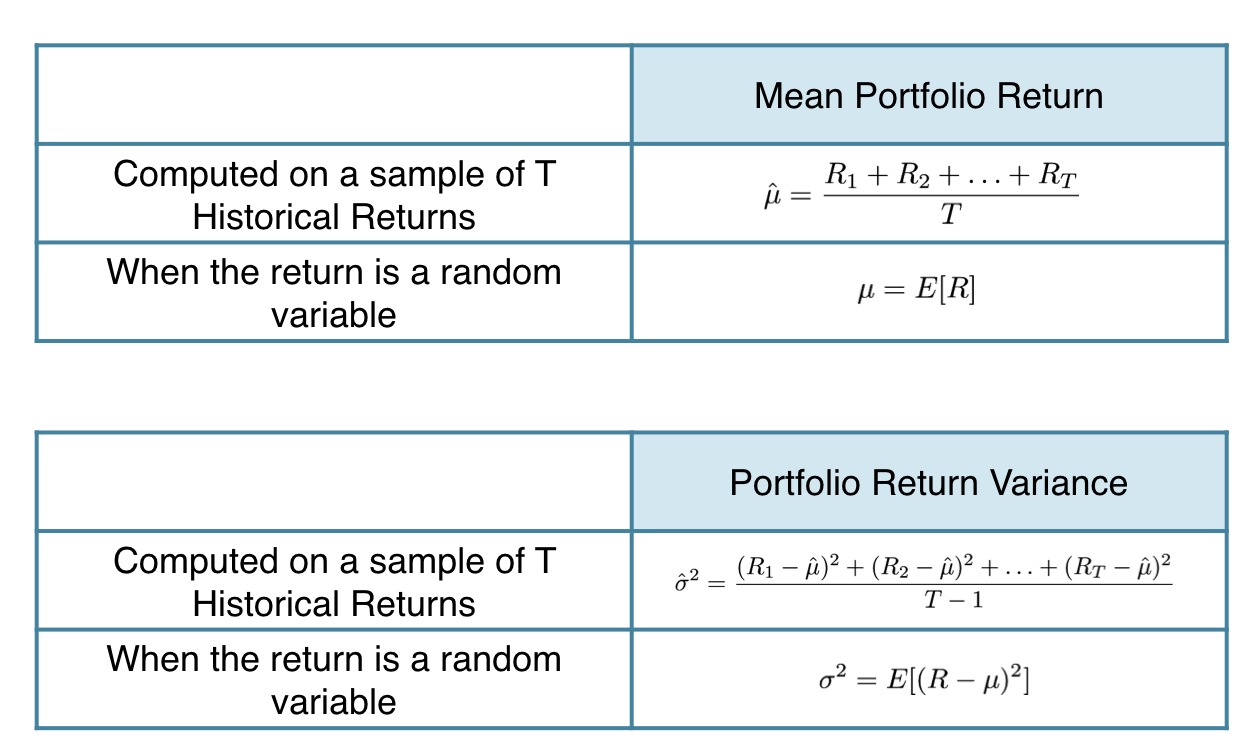

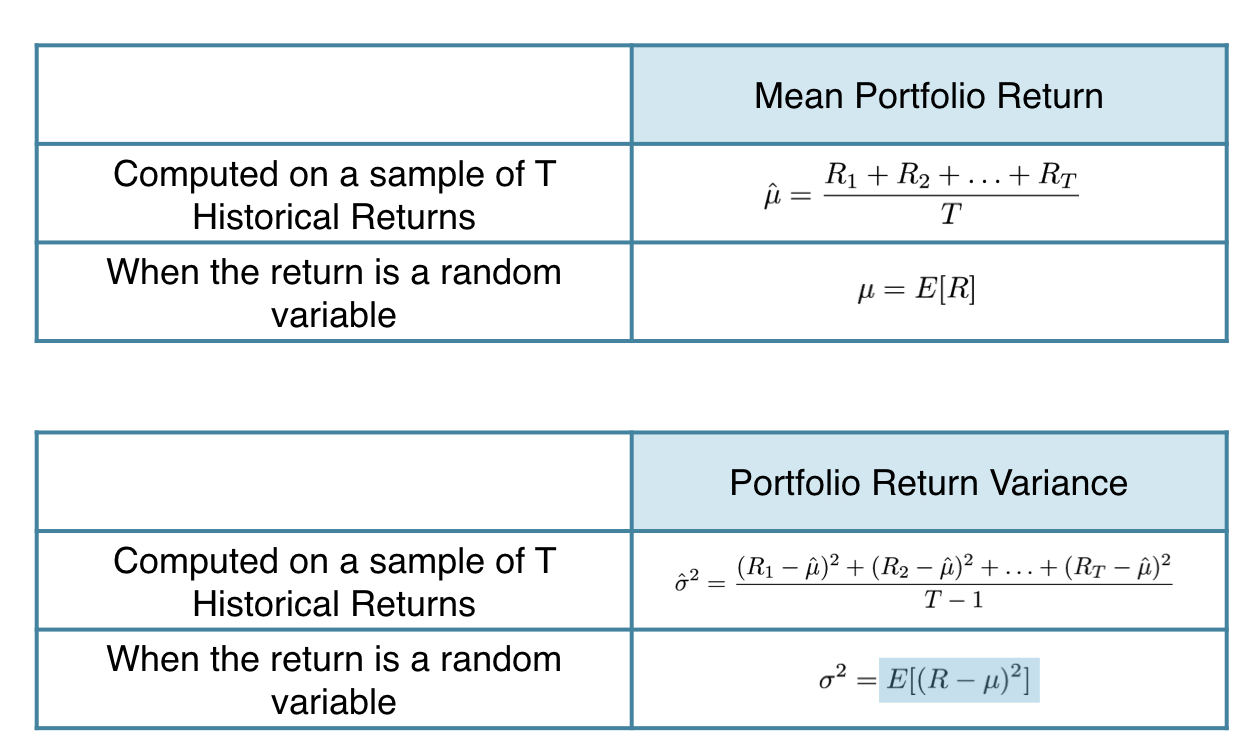

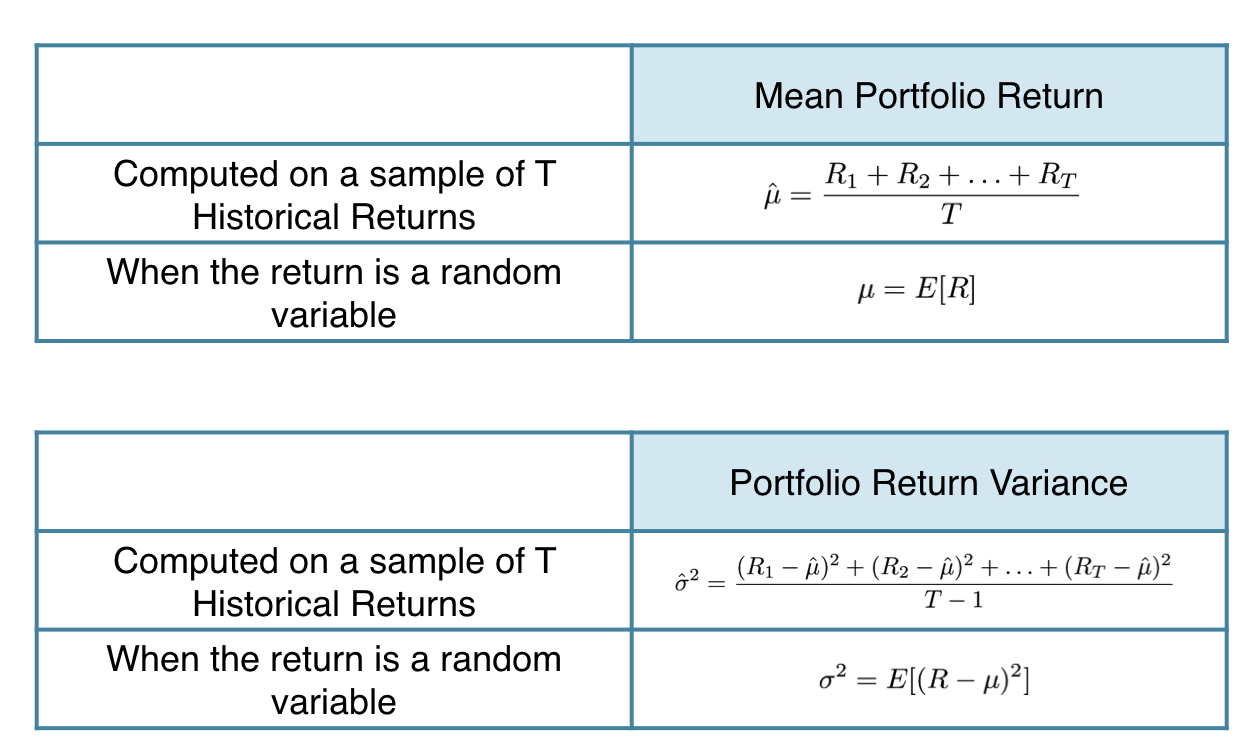

Van prestaties naar voorspellingen

Van prestaties naar voorspellingen

Van prestaties naar voorspellingen

Van prestaties naar voorspellingen

Van prestaties naar voorspellingen

Van prestaties naar voorspellingen

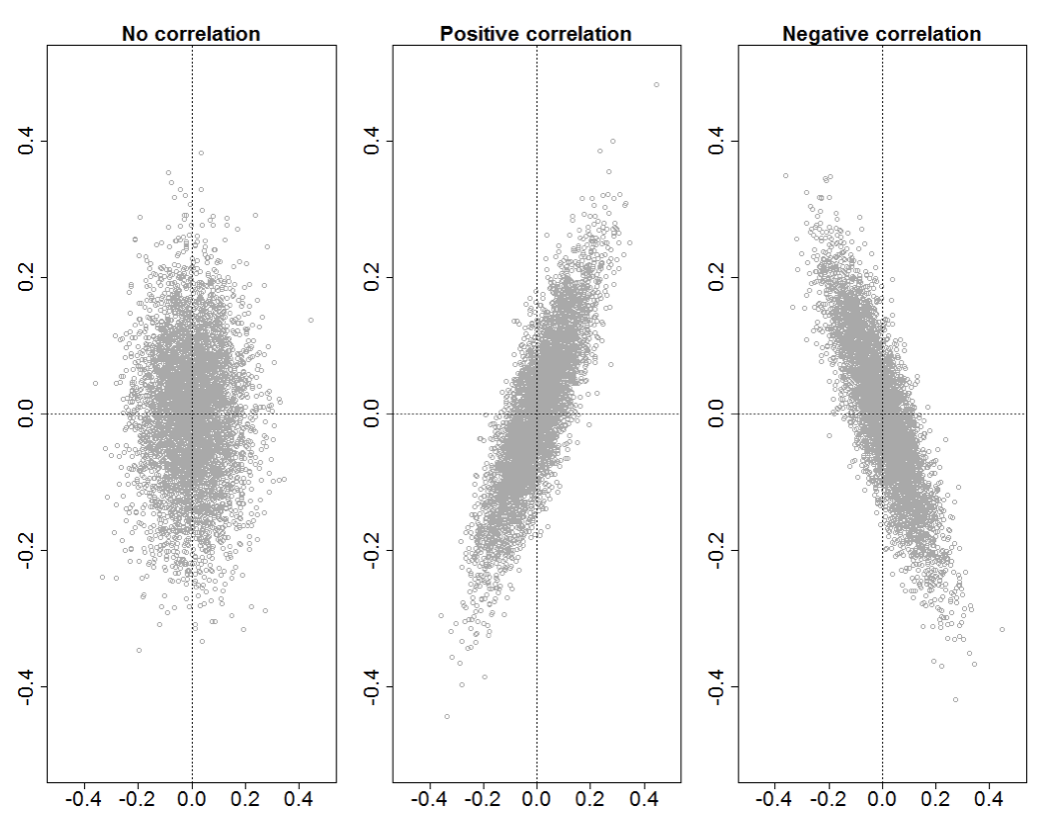

Correlaties