Convexiteit

Waardering en analyse van obligaties in Python

Joshua Mayhew

Options Trader

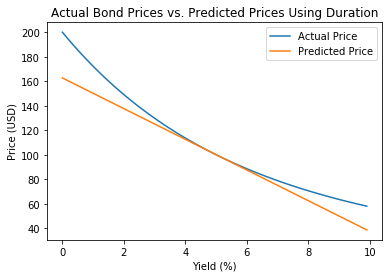

Voorspelde vs. werkelijke prijzen plotten

Beperkingen van duration

Wat is convexiteit?

- Meet de kromming van obligatieprijzen

- Verbetert prijsvoorspelling en risicometing

- Hogere convexiteit = meer gekromde prijs/yield-relatie