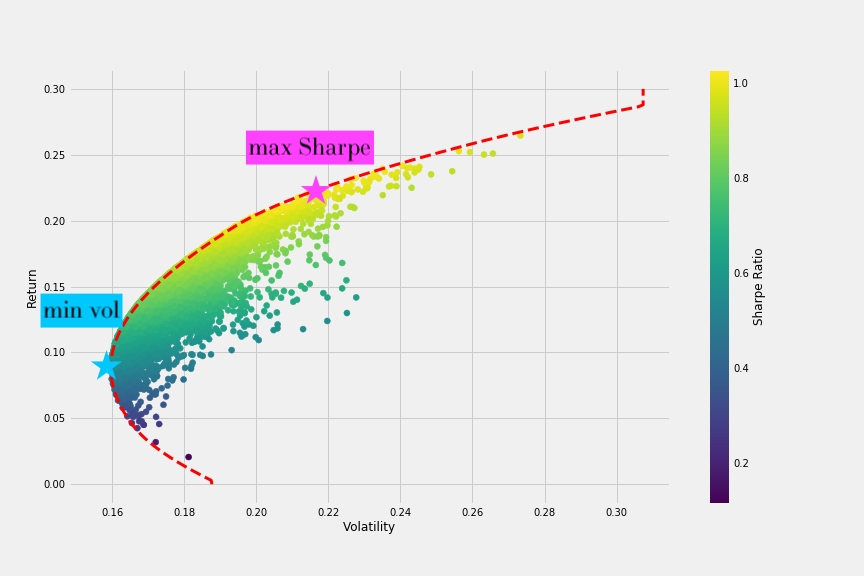

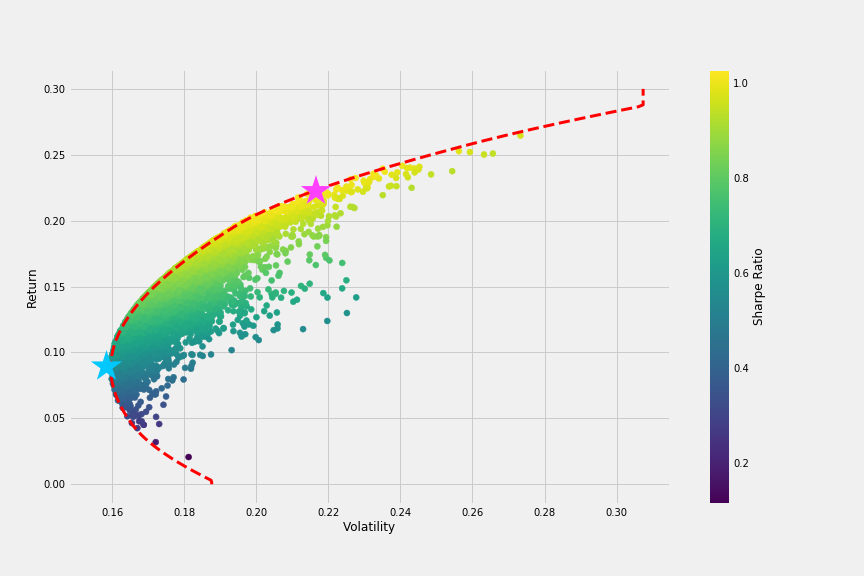

Sharpe maksimum vs. volatilitas minimum

Pengantar Analisis Portofolio dengan Python

Charlotte Werger

Data Scientist

Masih ingat Efficient Frontier?

$$

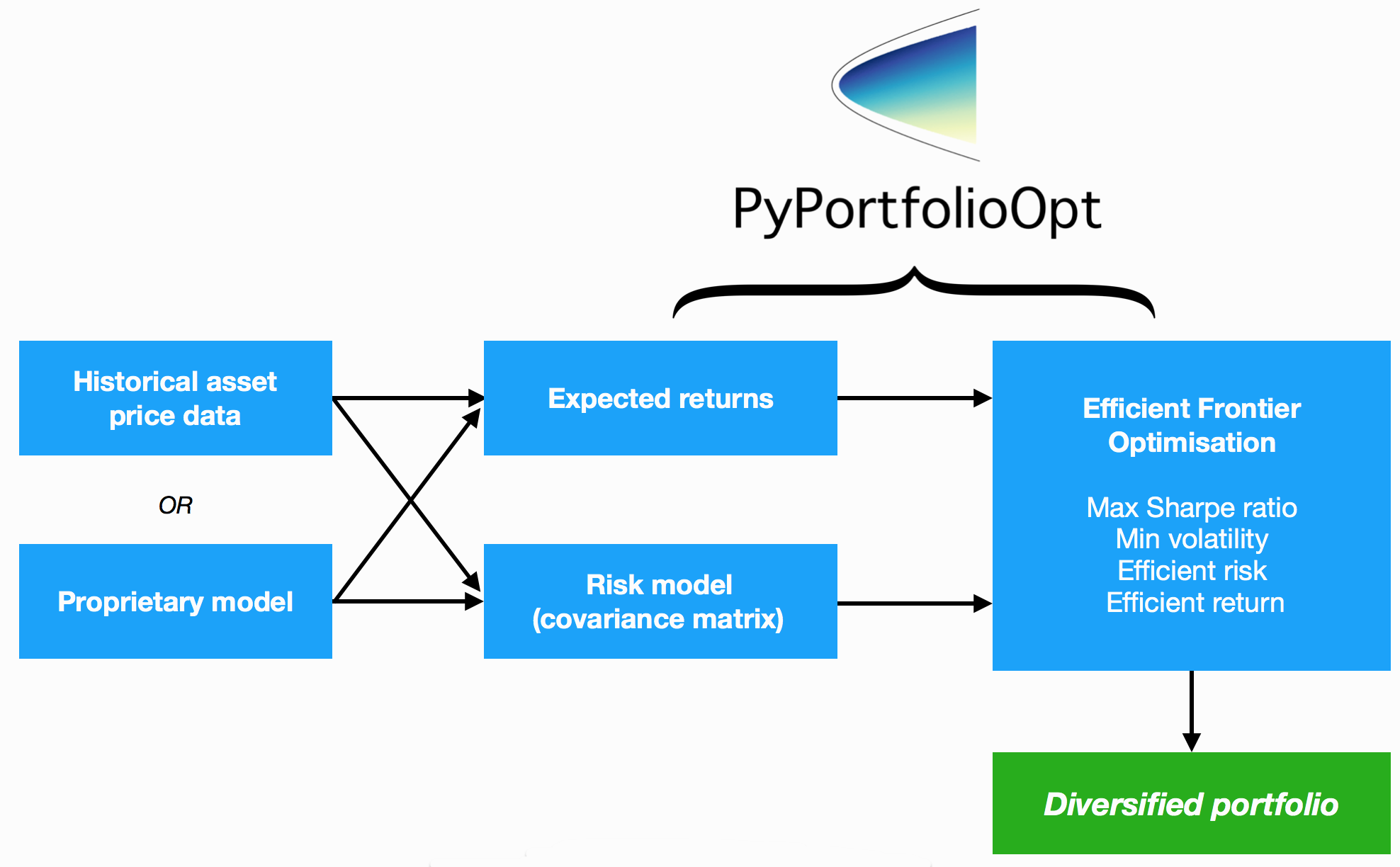

Menyesuaikan optimisasi PyPortfolioOpt

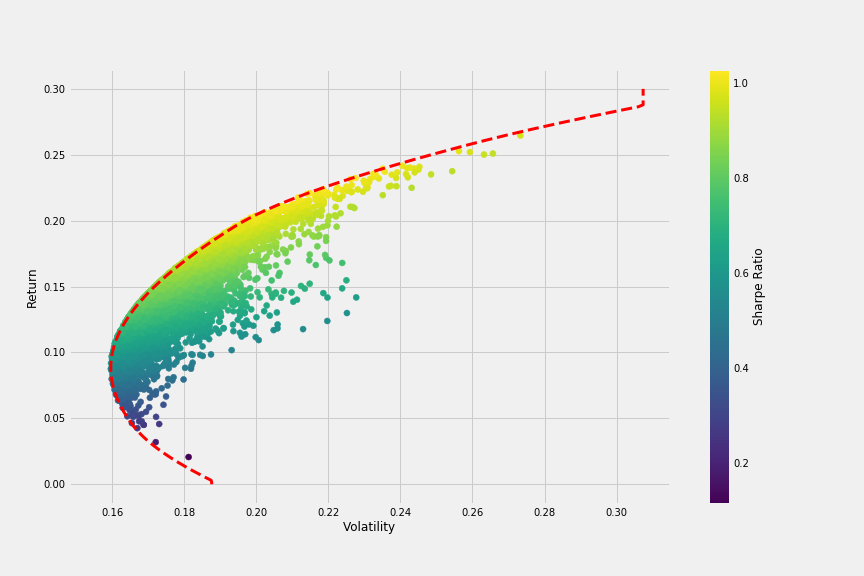

Mari lihat kembali Efficient Frontier

Sharpe maksimum vs. Volatilitas minimum