Gunakan model GARCH tervalidasi di produksi

Model GARCH di R

Kris Boudt

Professor of finance and econometrics

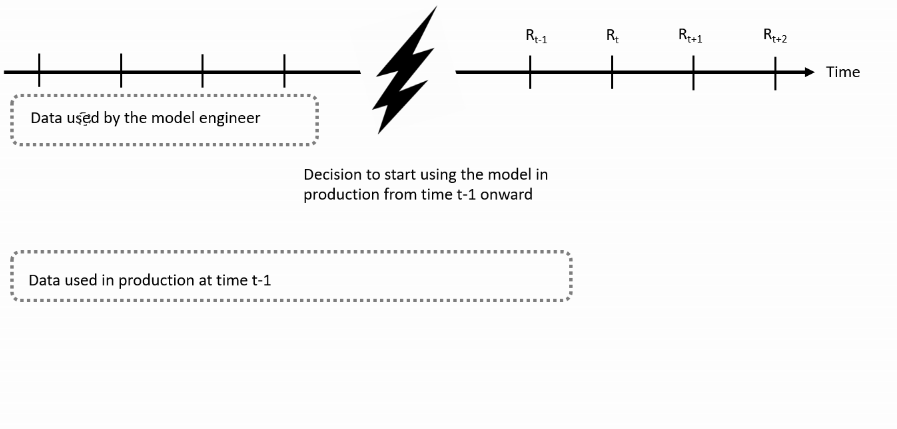

Penggunaan di produksi

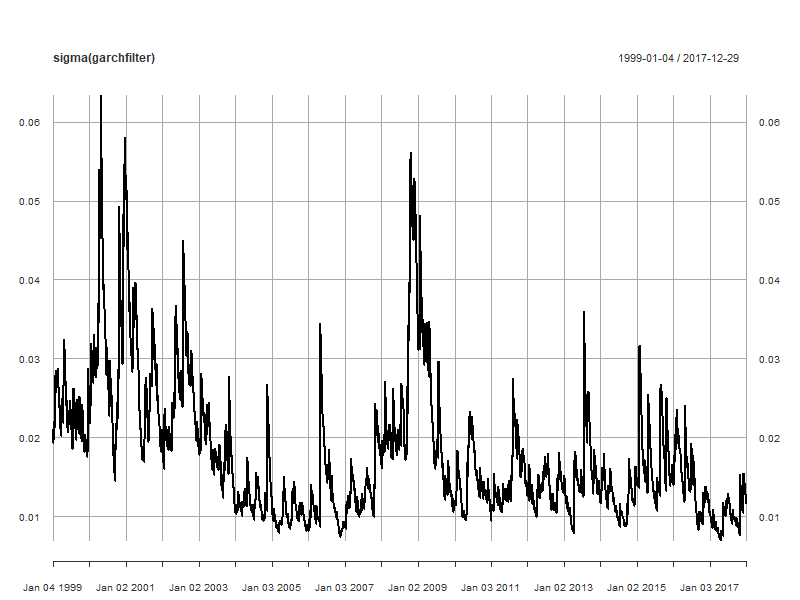

Langkah 2: Analisis dinamika mean dan volatilitas

Gunakan fungsi ugarchfilter():

garchfilter <- ugarchfilter(data = msftret, spec = progarchspec)

plot(sigma(garchfilter))

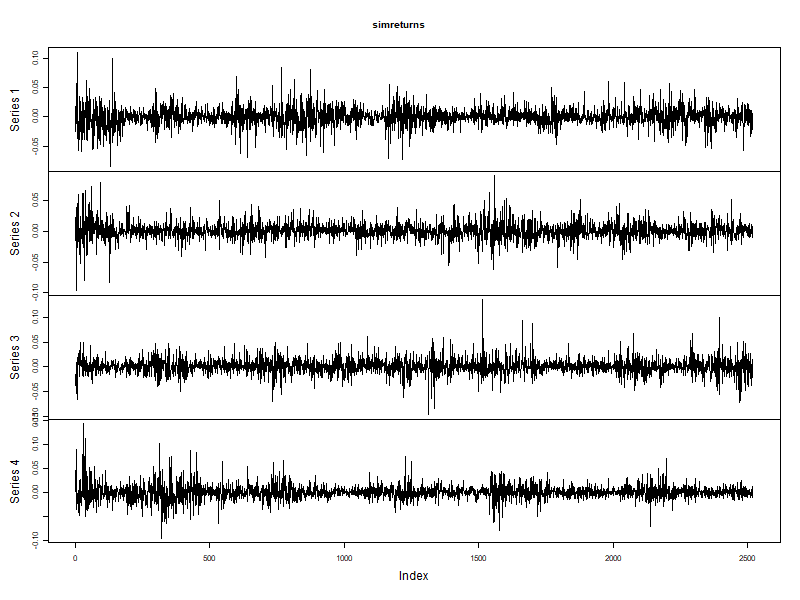

Langkah 3: Analisis return tersimulasikan

Metode fitted() memberikan return tersimulasikan:

simret <- fitted(simgarch)

plot.zoo(simret)

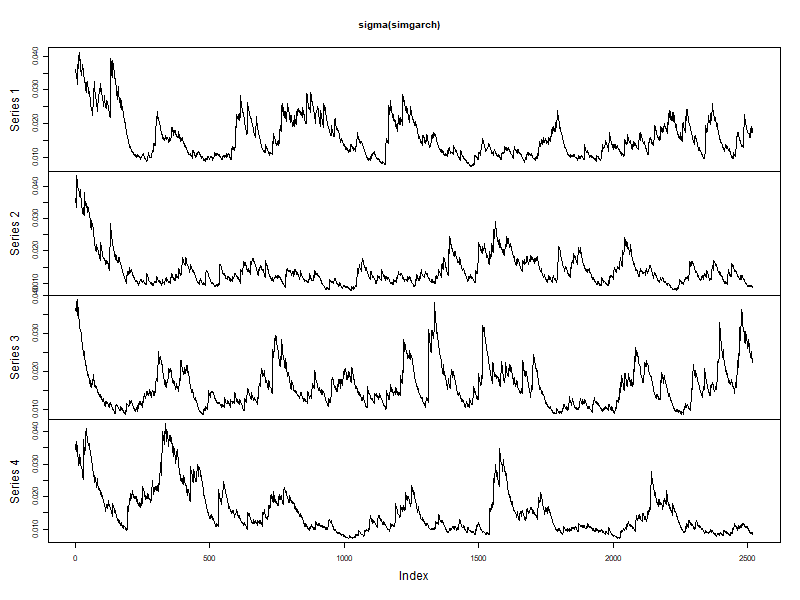

Analisis volatilitas tersimulasikan

plot.zoo(sigma(simgarch))

Analisis harga tersimulasikan

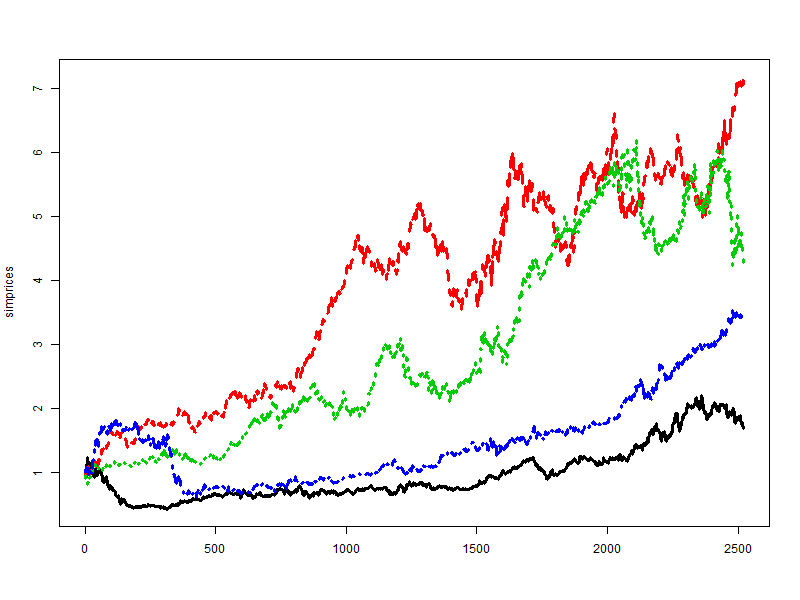

Memplot 4 simulasi harga saham selama 10 tahun, dengan harga awal 1:

simprices <- exp(apply(simret, 2, "cumsum"))

matplot(simprices, type = "l", lwd = 3)