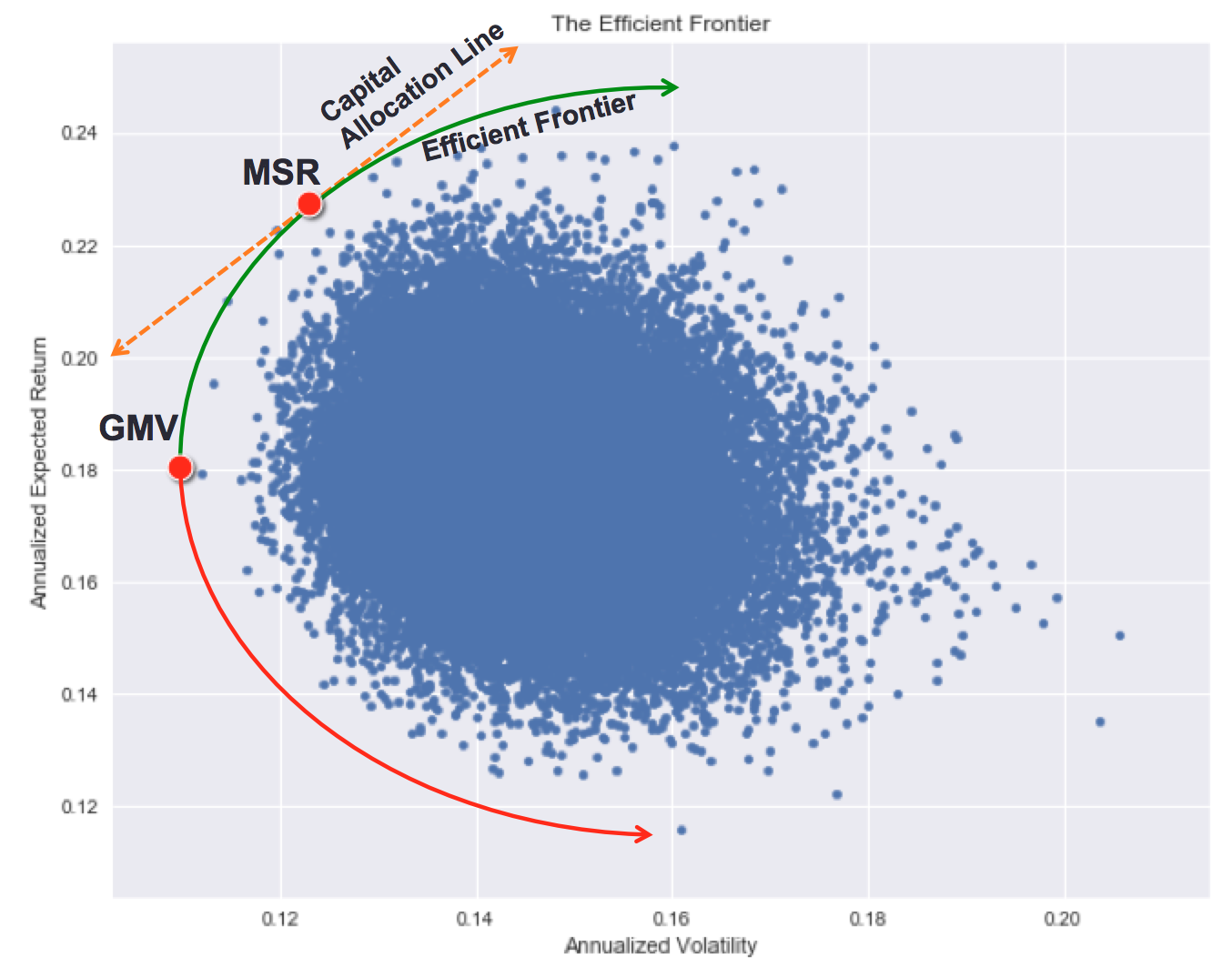

Markowitz portfolios

Introduzione alla gestione del rischio di portafoglio in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

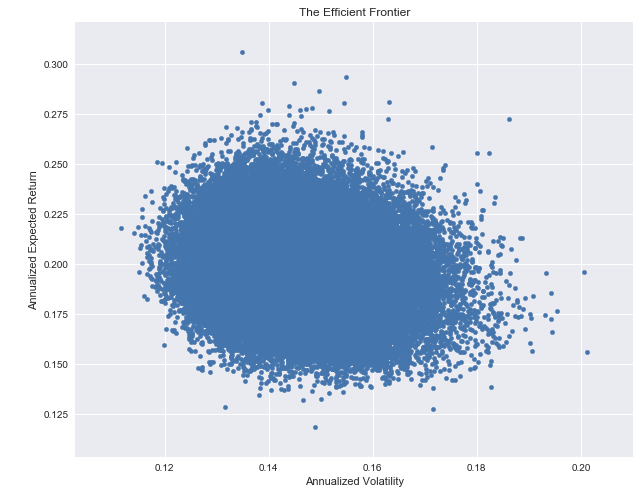

100,000 randomly generated portfolios

The efficient frontier

The Markowitz portfolios

Introduzione alla gestione del rischio di portafoglio in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com