Financial returns

Introduzione alla gestione del rischio di portafoglio in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

Financial risk

Returns

Probability

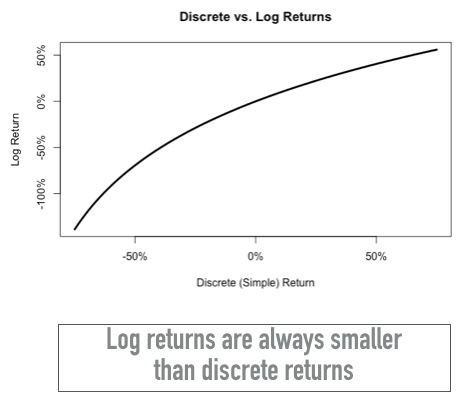

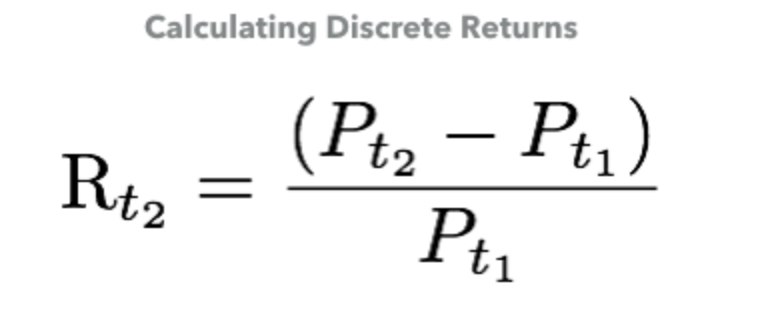

A tale of two returns

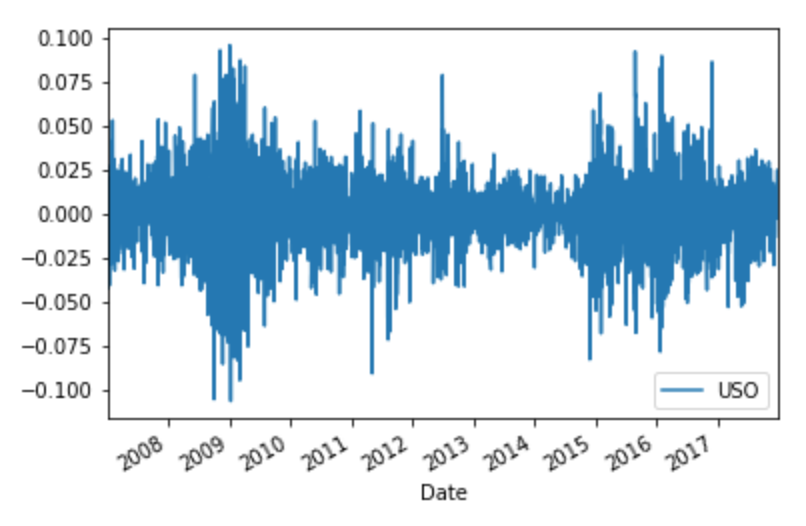

Calculating stock returns

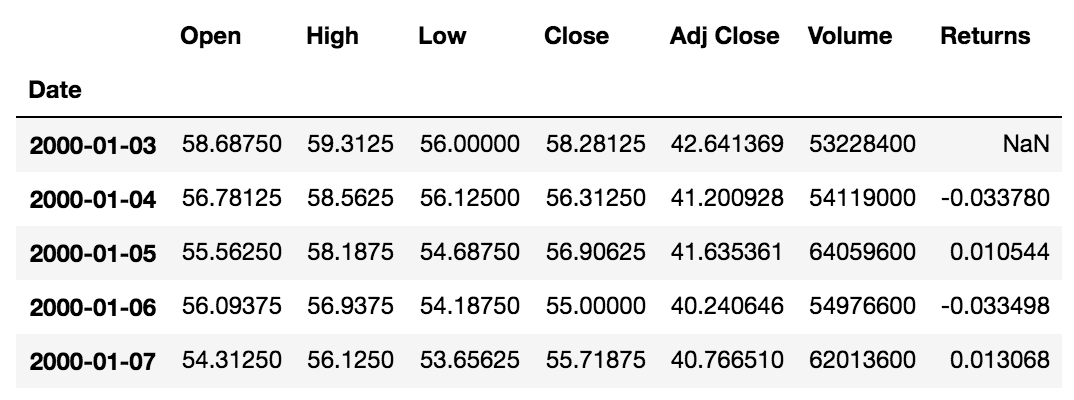

Calculating stock Returns in Python

Step 2:

Calculate daily returns of the adjusted close prices and append the returns as a new column in the DataFrame.

StockPrices["Returns"] = StockPrices["Adj Close"].pct_change()

StockPrices["Returns"].head()

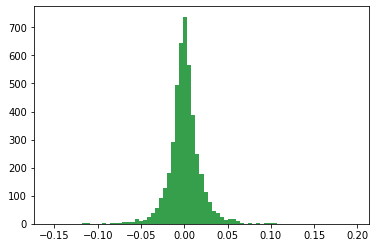

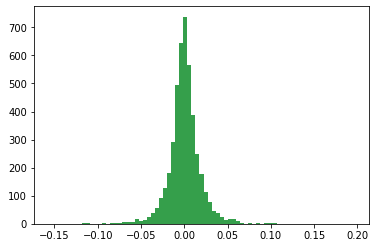

Visualizing return distributions

import matplotlib.pyplot as plt

plt.hist(StockPrices["Returns"].dropna(), bins=75, density=False)

plt.show()