Confronta modelli AR e MA

Analisi delle serie temporali in R

David S. Matteson

Associate Professor at Cornell University

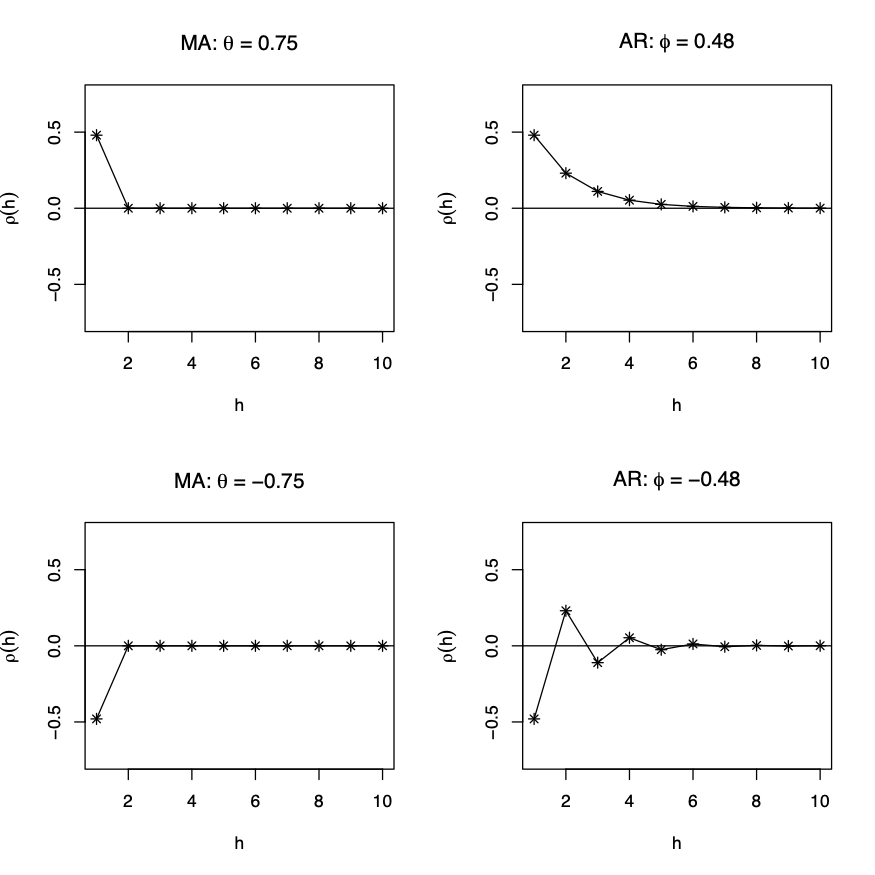

Processi MA e AR: autocorrelazioni

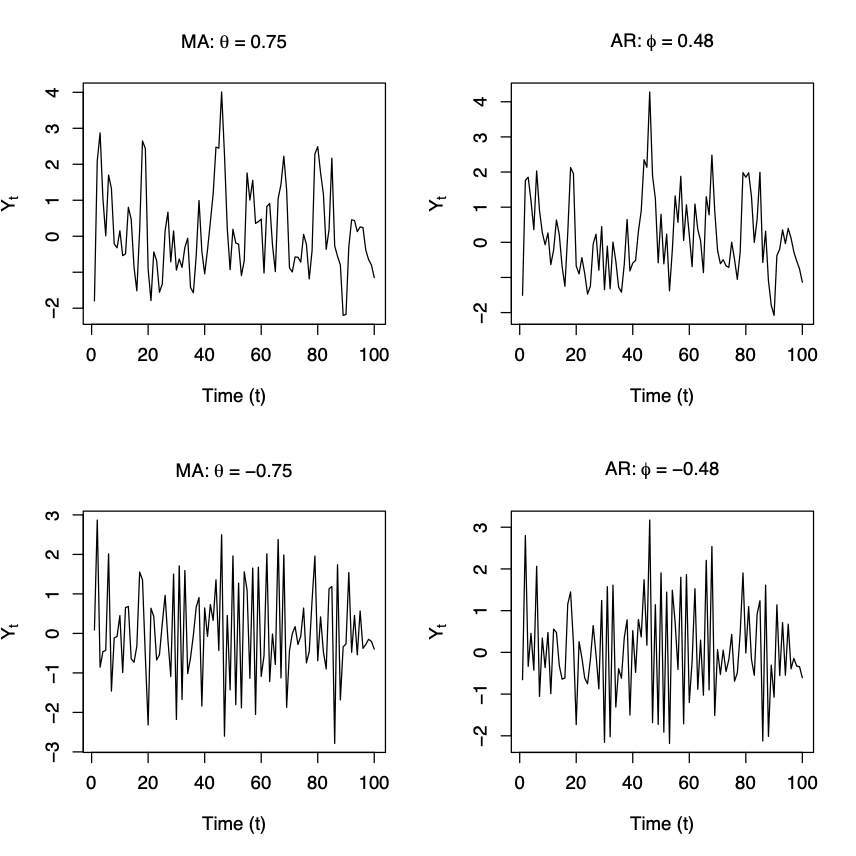

Processi MA e AR: simulazioni

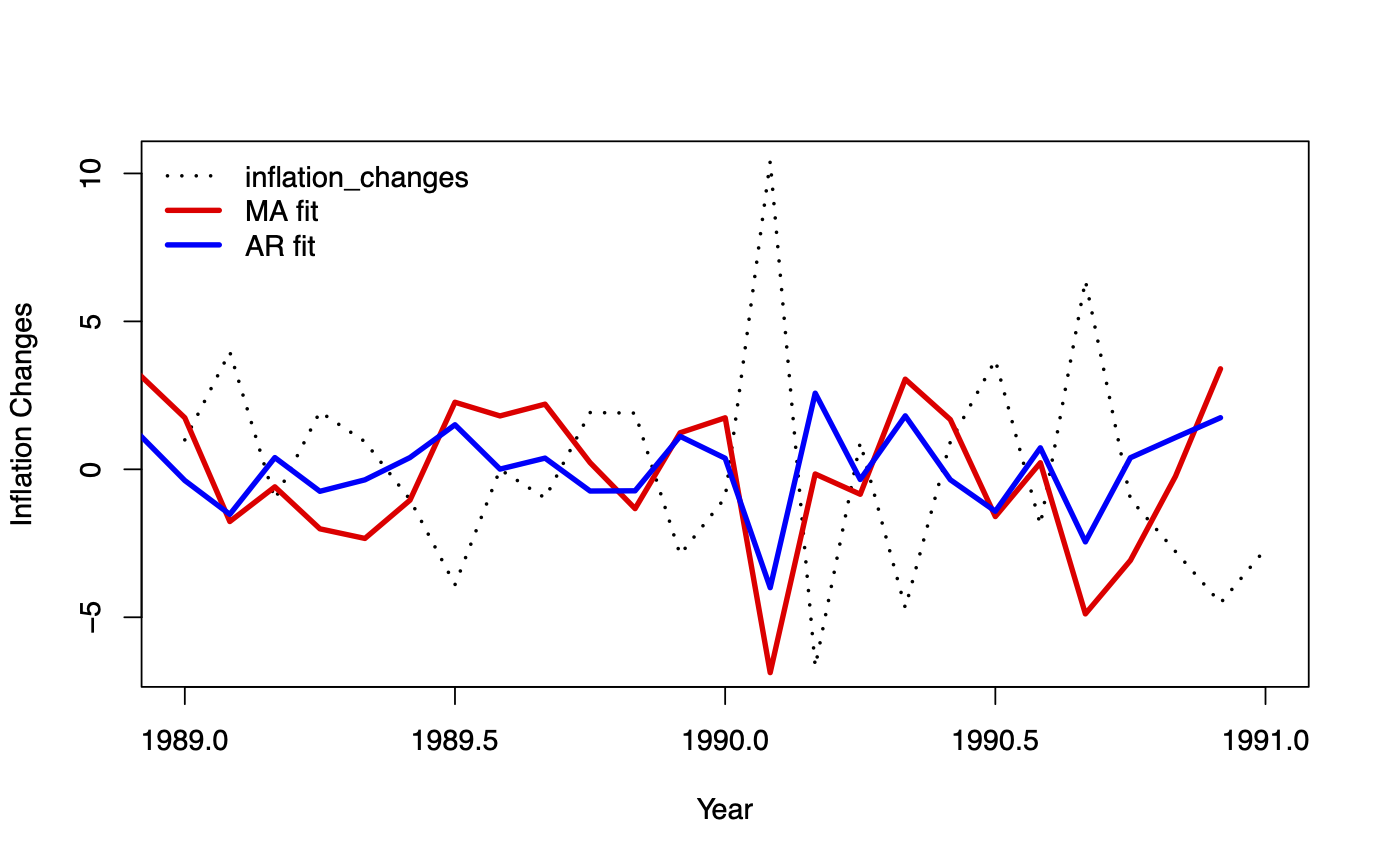

Processi MA e AR: valori adattati

- Variazioni dell’inflazione USA mensile

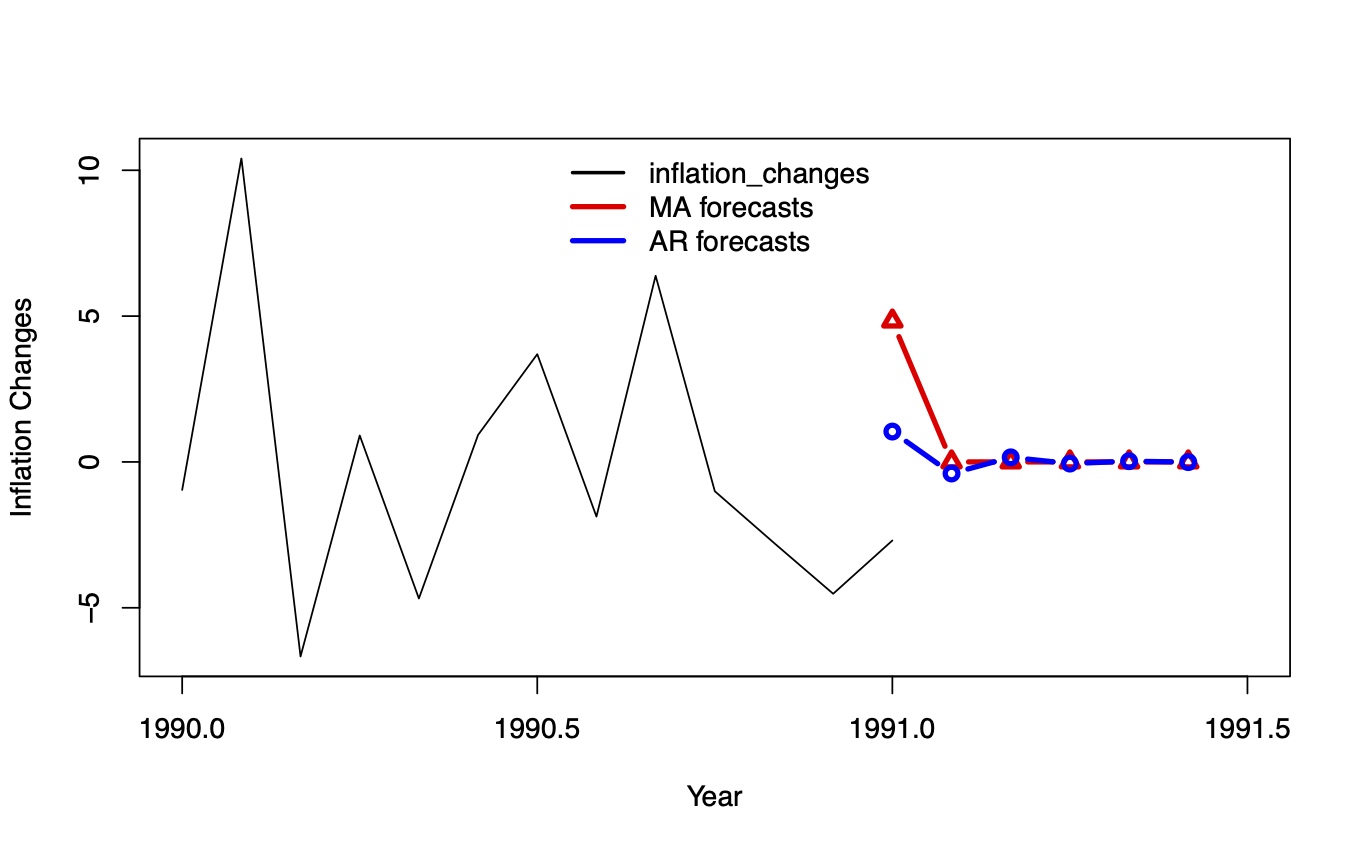

Processi MA e AR: previsioni

- Variazioni dell’inflazione USA mensile