Stima e previsione di modelli AR

Analisi delle serie temporali in R

David S. Matteson

Associate Professor at Cornell University

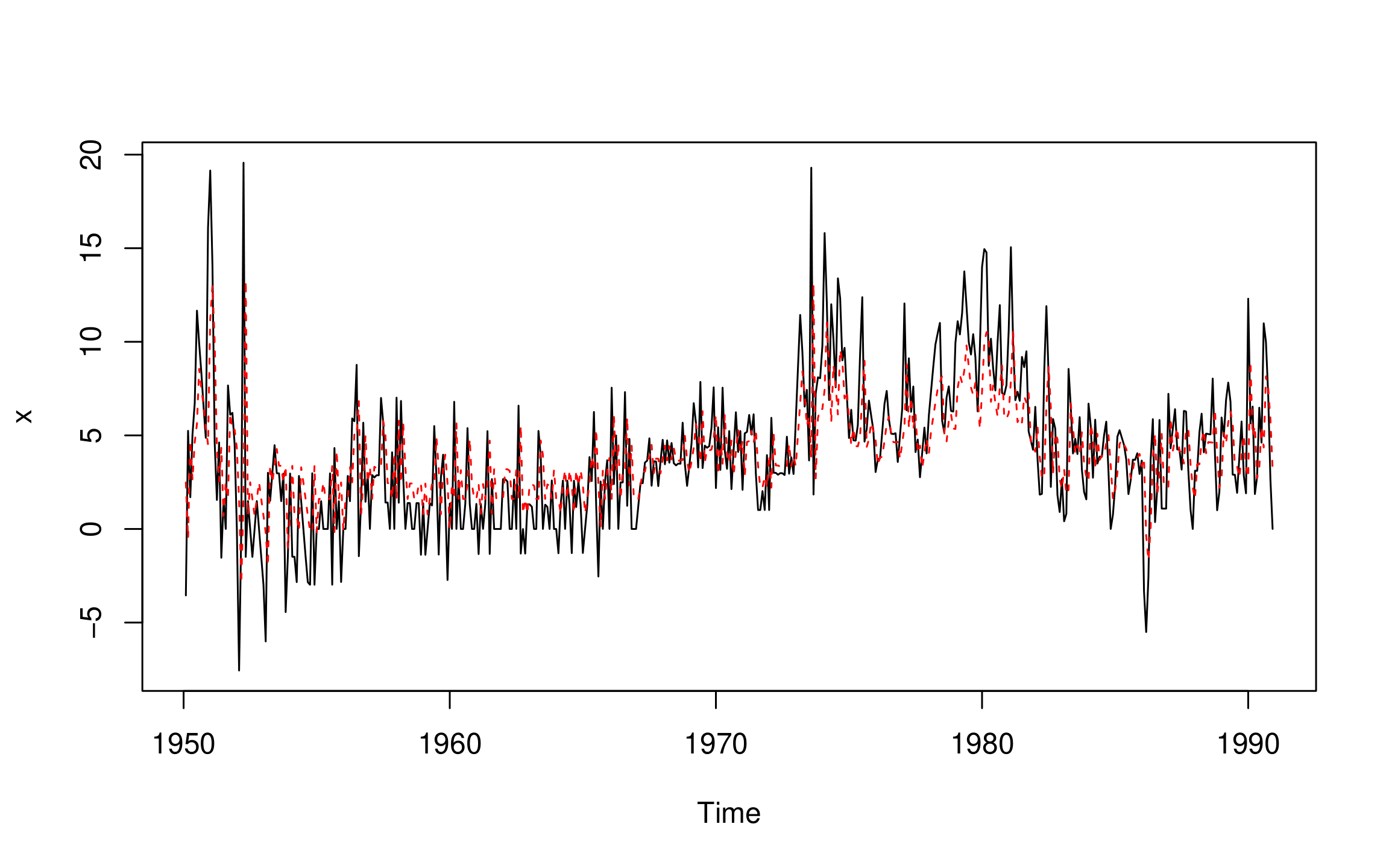

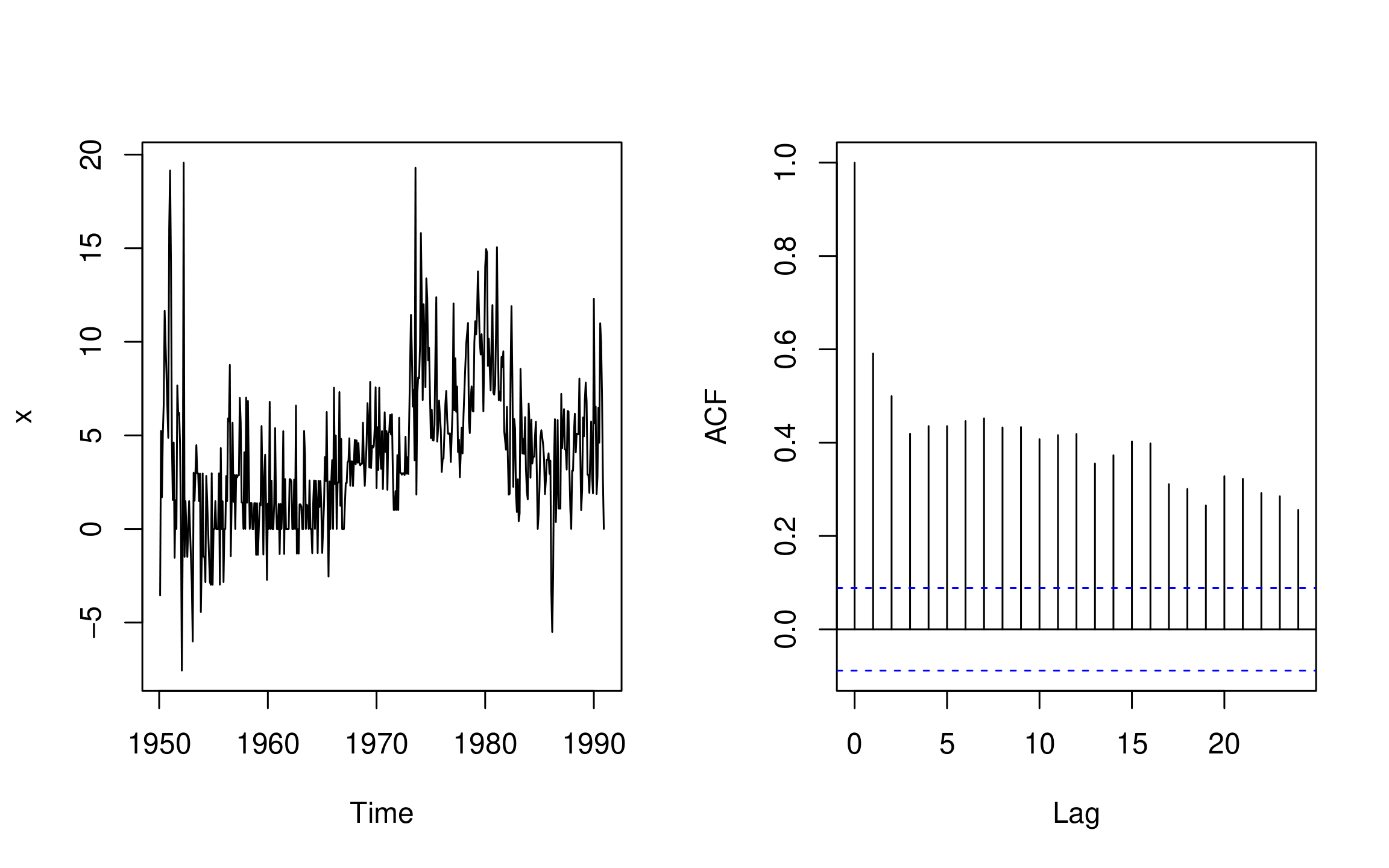

Processi AR: tasso d'inflazione

- Tasso d'inflazione USA mensile (in percento, tasso annuo).

- Osservazioni mensili dal 1950 al 1990

data(Mishkin, package = "Ecdat")inflation <- as.ts(Mishkin[, 1])ts.plot(inflation) ; acf(inflation)

Processi AR: valori adattati - I

- Valori adattati AR:

$$\hat{Y_t} = \hat{\mu} + \hat{\phi}(Y_{t-1} - \hat{\mu})$$

- Residui =

$$ \hat{\epsilon_t} = Y_t - \hat{Y_t}$$

Processi AR: valori adattati - II

ts.plot(inflation)AR_inflation_fitted <- inflation - residuals(AR_inflation)points(AR_inflation_fitted, type = "l" col = "red", lty = 2)