Previsioni con ARIMA stagionale

Modelli ARIMA in R

David Stoffer

Professor of Statistics at the University of Pittsburgh

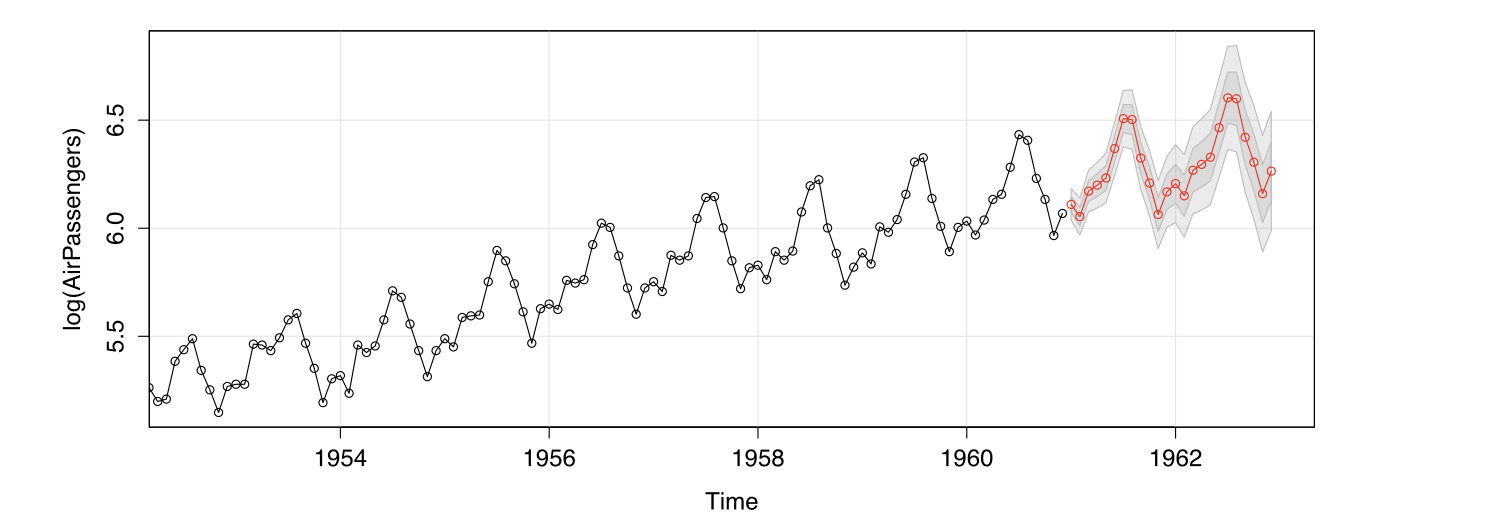

Previsioni per Air Passengers

- Nel video precedente abbiamo deciso che un modello

SARIMA$(0,1,1) \times (0,1,1)_{12}$ era adeguato

sarima.for(log(AirPassengers), n.ahead = 24,

0, 1, 1, 0, 1, 1, 12)