Driver nel caso di due asset

Introduzione all'analisi di portafoglio in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

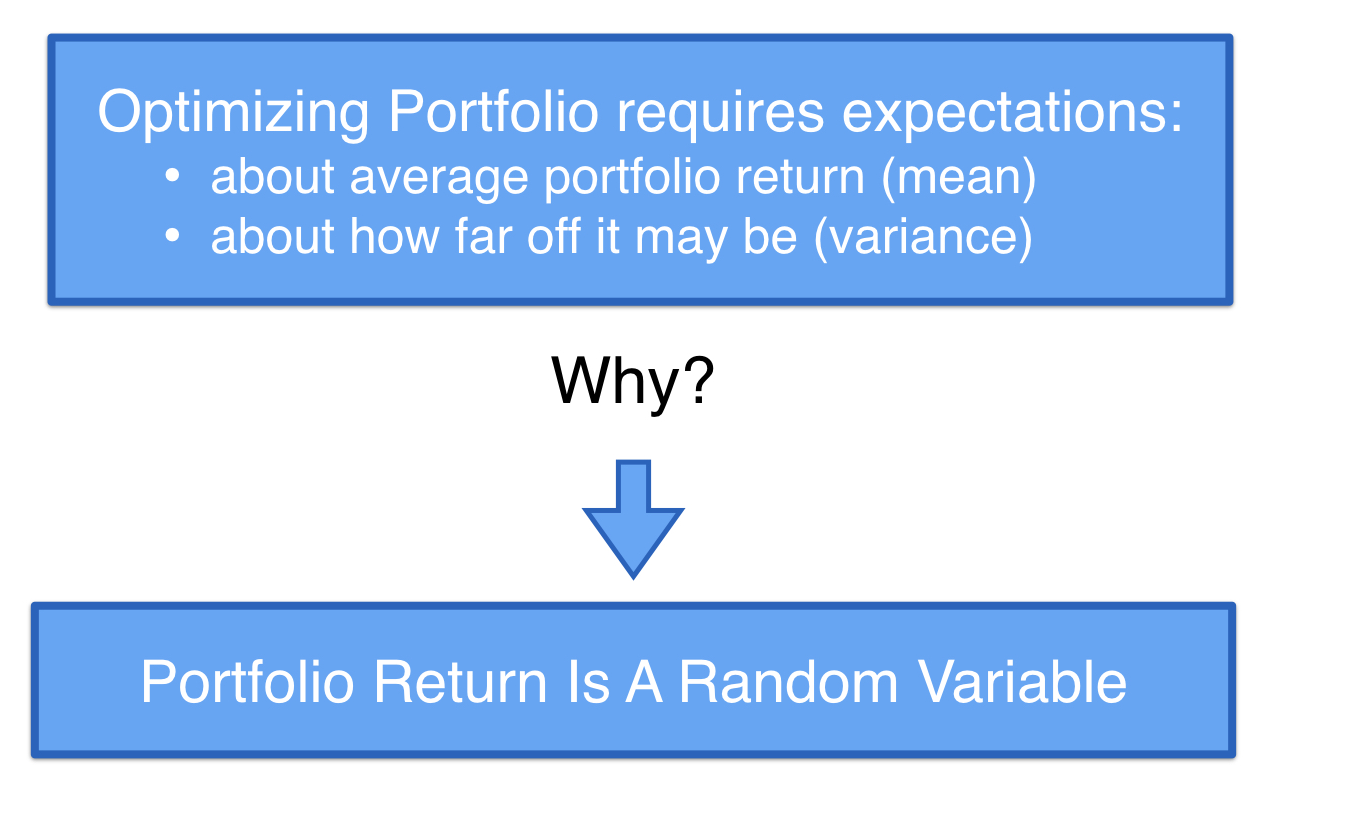

I rendimenti futuri sono per natura casuali

I rendimenti futuri sono per natura casuali

I rendimenti futuri sono per natura casuali

I rendimenti futuri sono per natura casuali

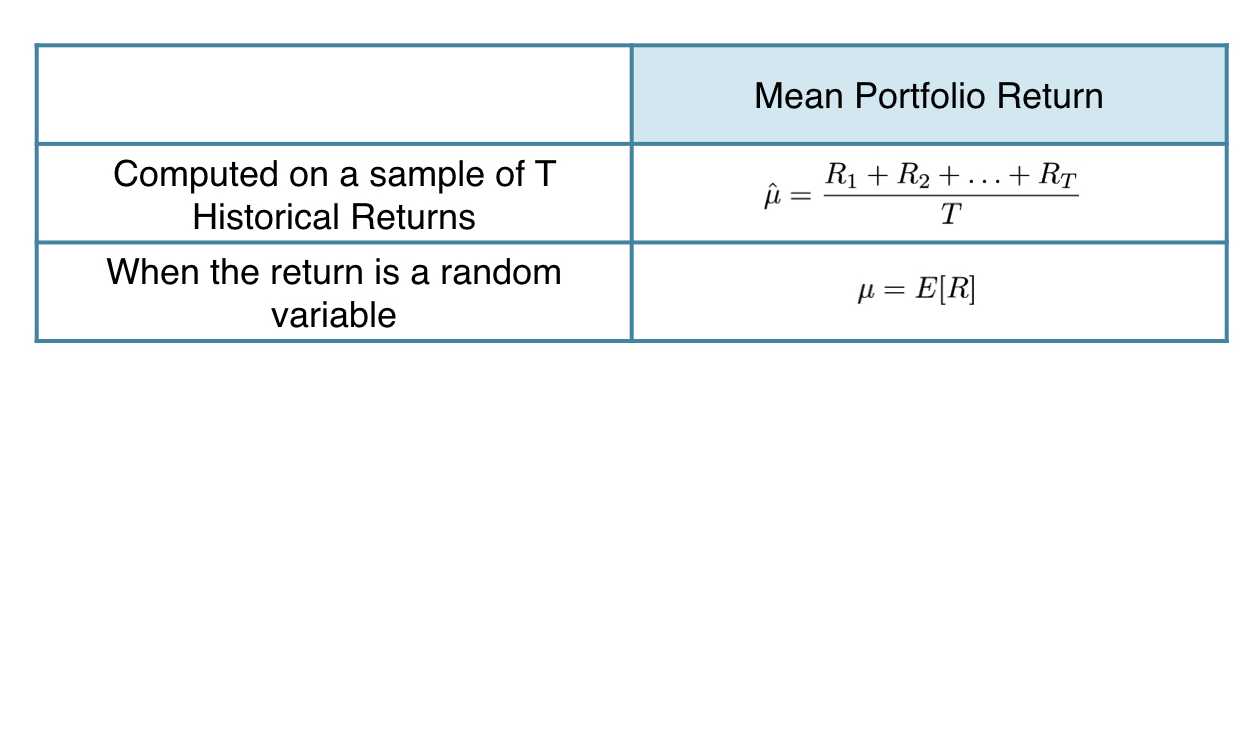

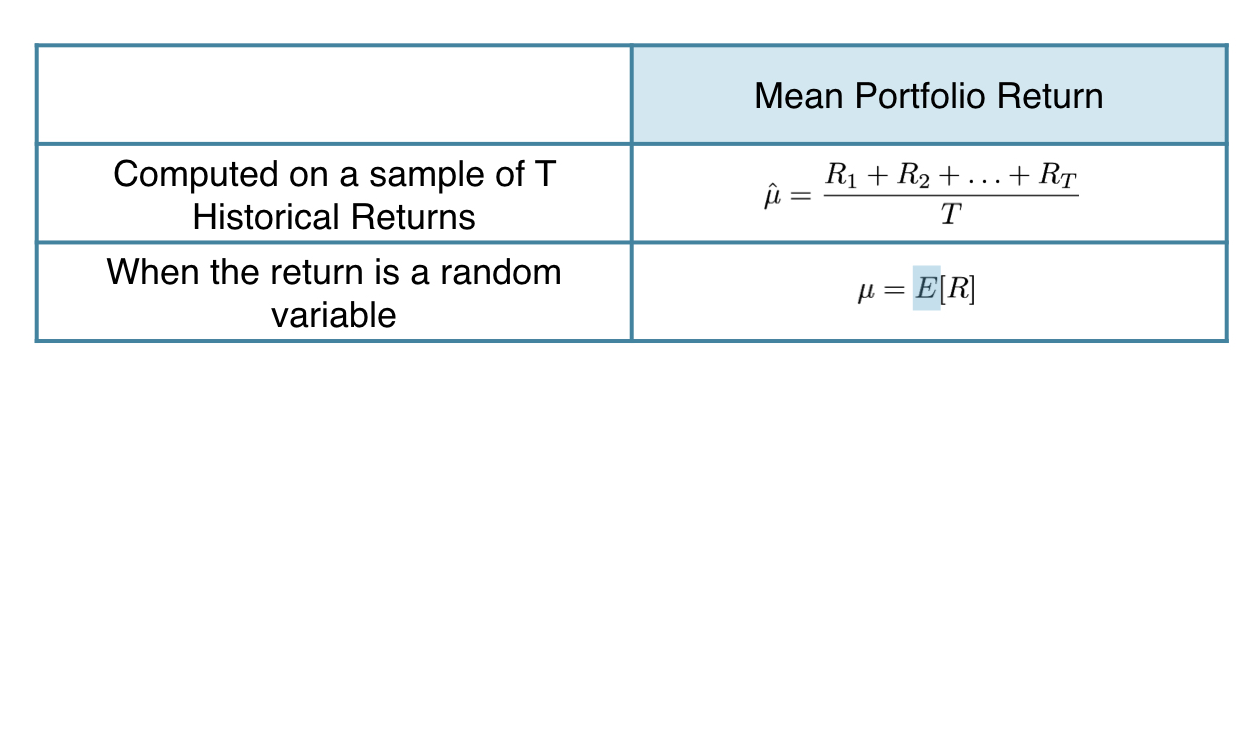

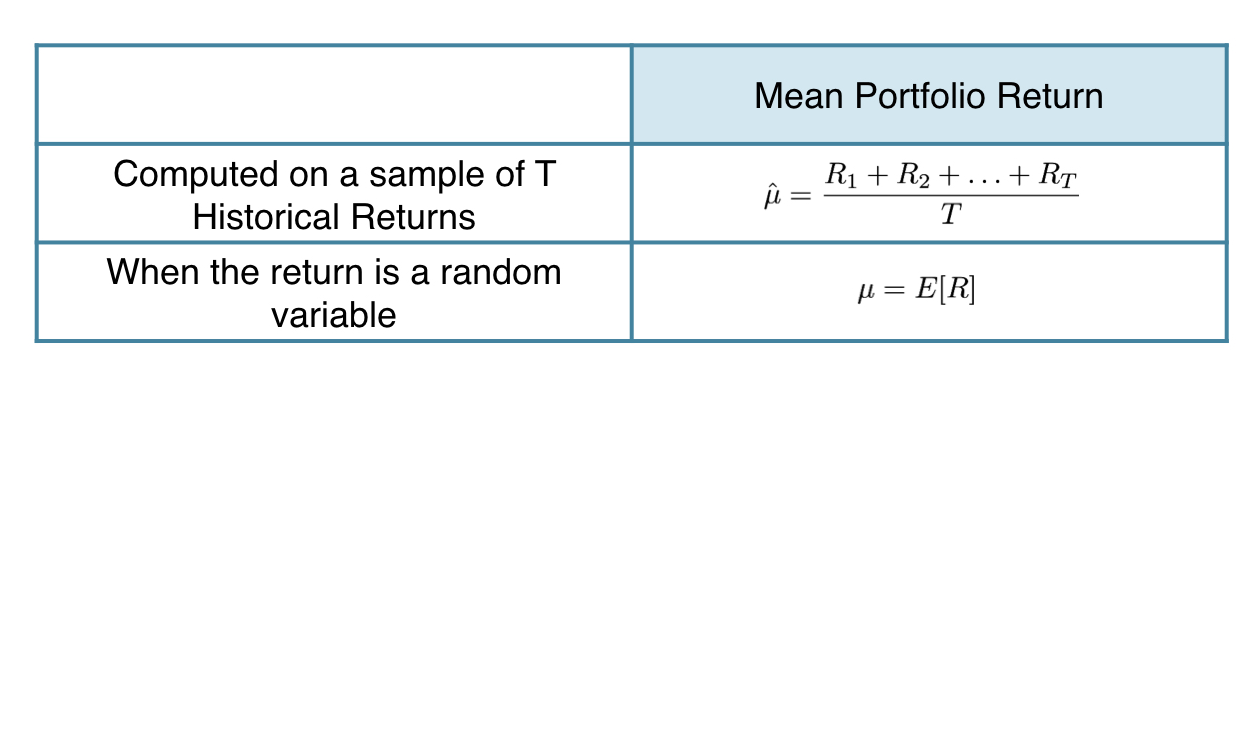

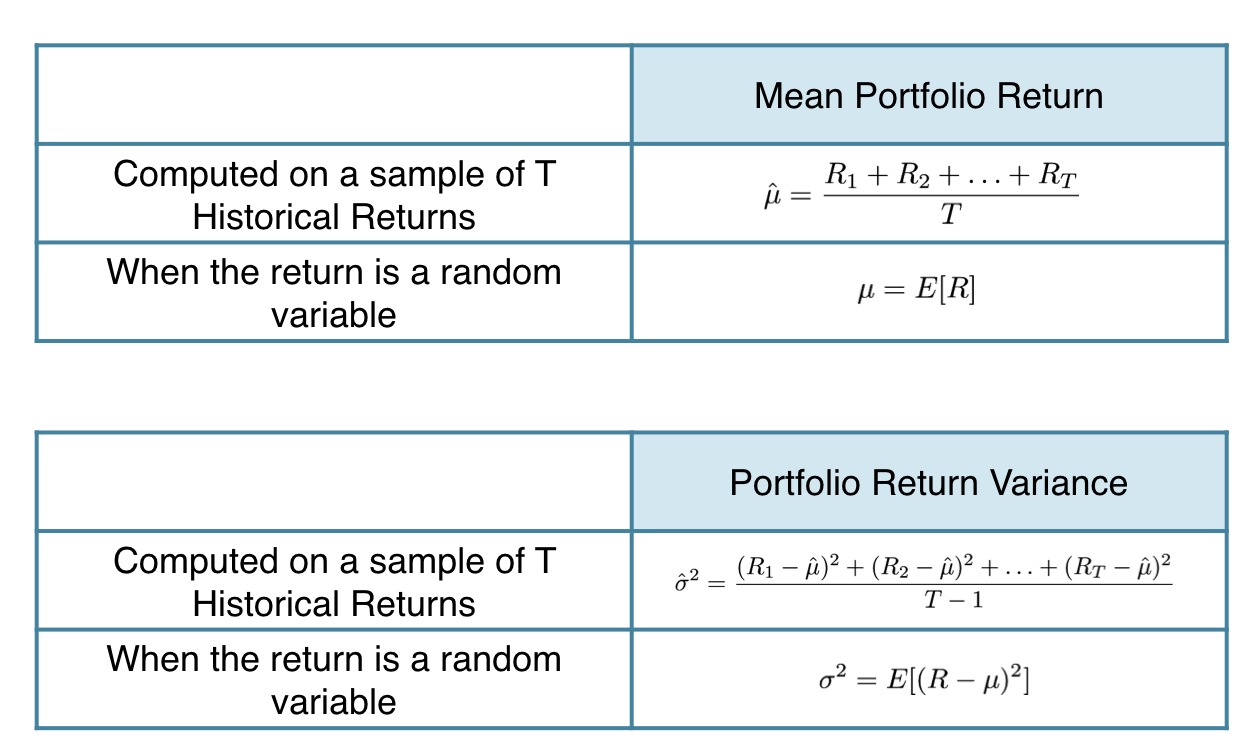

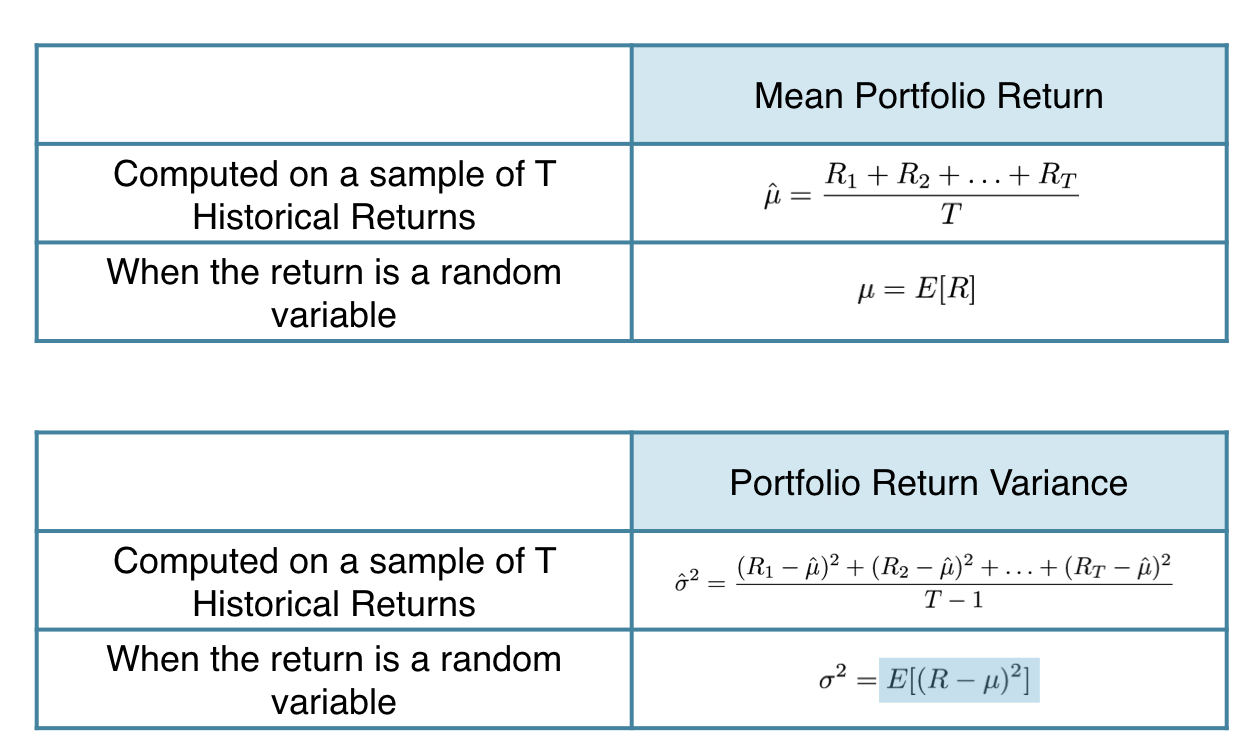

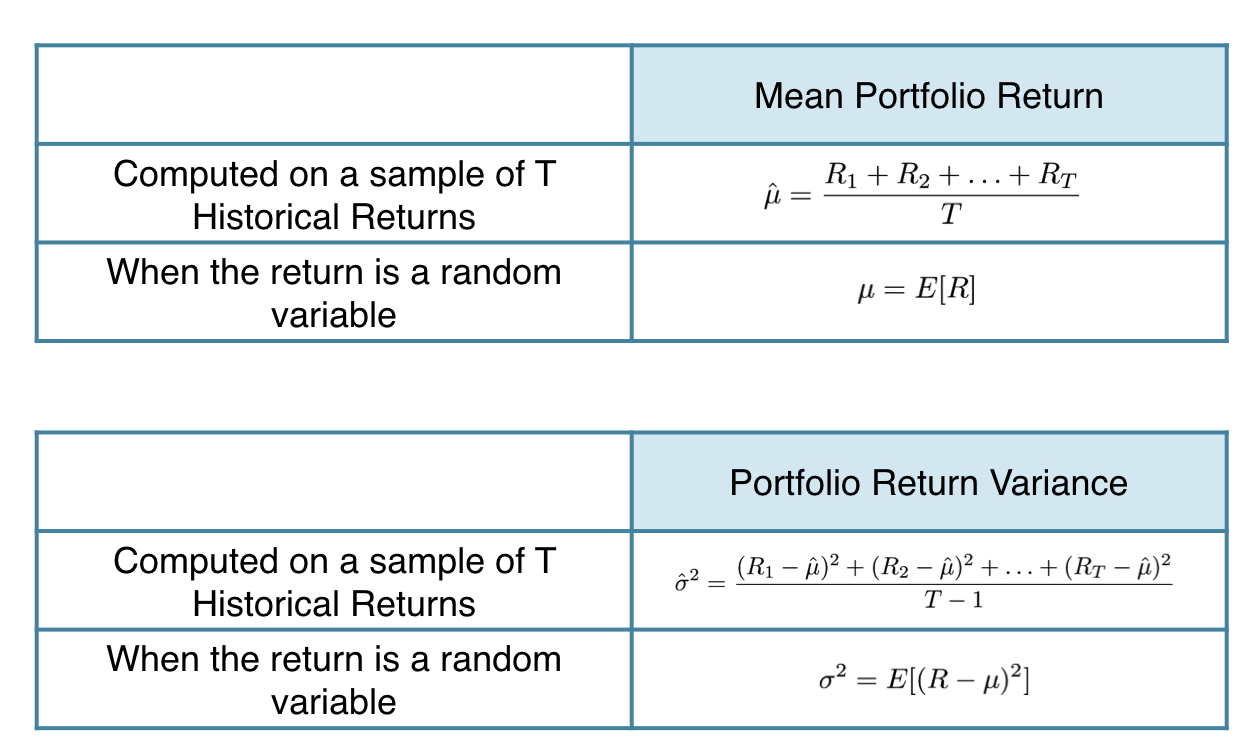

Dalla performance passata alle previsioni

Dalla performance passata alle previsioni

Dalla performance passata alle previsioni

Dalla performance passata alle previsioni

Dalla performance passata alle previsioni

Dalla performance passata alle previsioni

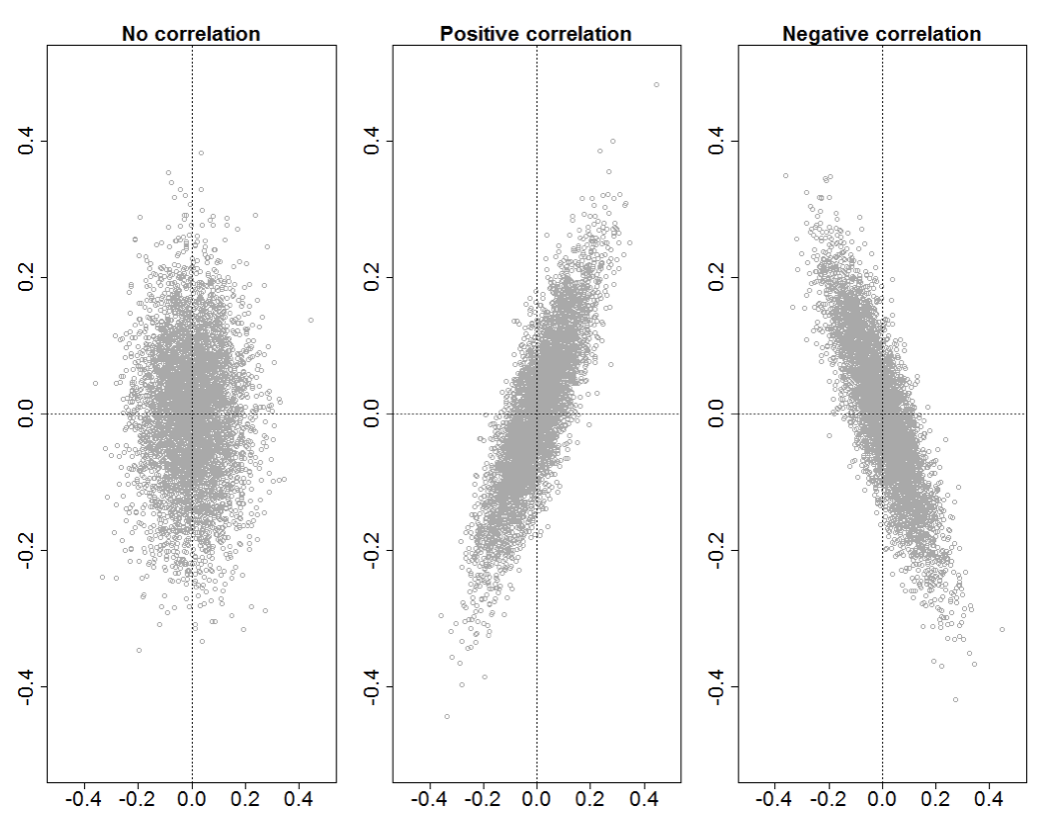

Correlazioni