Metodi di shrinkage

Feature Engineering in R

Jorge Zazueta

Research Professor and Head of the Modeling Group at the School of Economics, UASLP

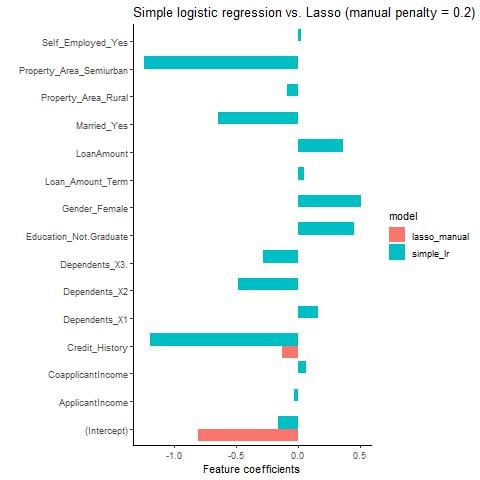

Logistica semplice vs. Lasso

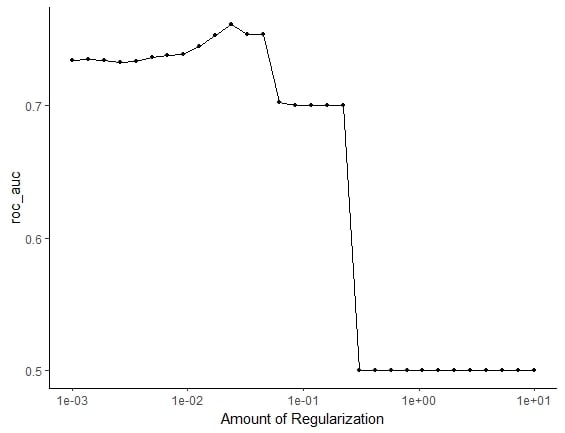

Tuning degli iperparametri

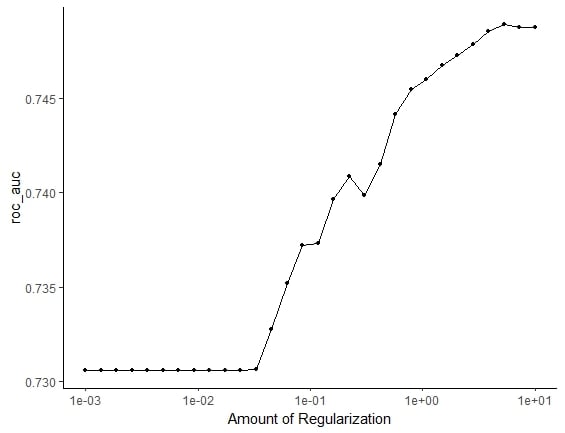

Esaminare l'output del tuning

tune_output <- tune_grid(

workflow_lasso_tuned,

resamples = vfold_cv(train, v = 5),

metrics = metric_set(roc_auc),

grid = penalty_grid)

autoplot(tune_output)

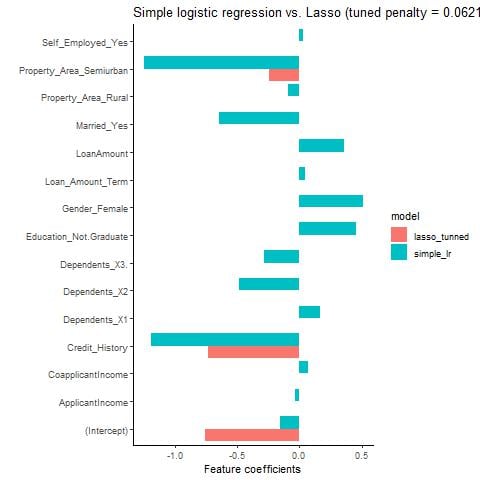

Logistica semplice vs. Lasso ottimizzato

Regolarizzazione Ridge

tune_output <- tune_grid(

workflow_ridge_tuned,

resamples = vfold_cv(train, v = 5),

metrics = metric_set(roc_auc),

grid = penalty_grid)

autoplot(tune_output)

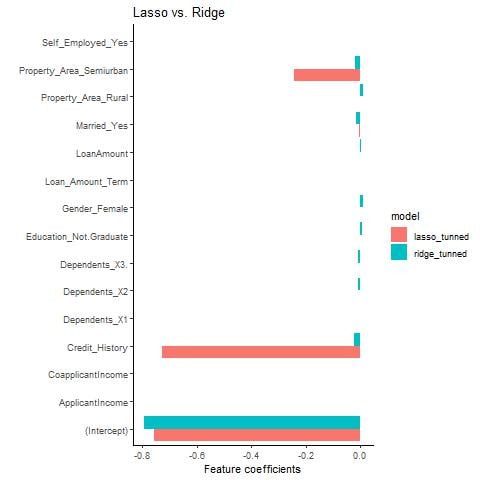

Ridge vs. Lasso