Portfolio composition and backtesting

Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

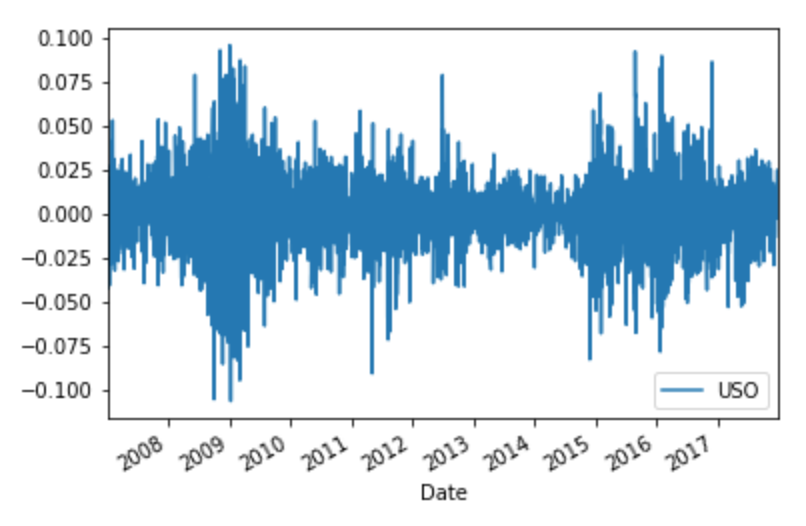

Plotting portfolio returns in Python

To plot the daily returns in Python:

StockPrices["Returns"] = StockPrices["Adj Close"].pct_change()

StockReturns = StockPrices["Returns"]

StockReturns.plot()

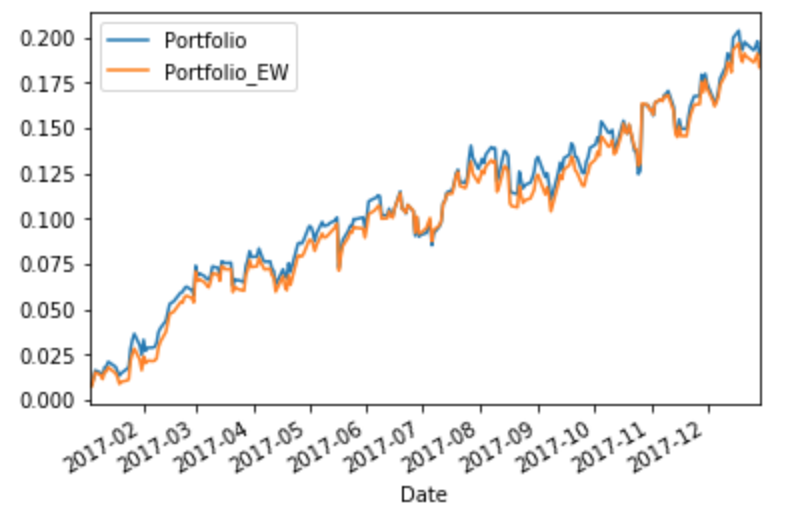

Plotting portfolio cumulative returns

In order to plot the cumulative returns of multiple portfolios:

import matplotlib.pyplot as plt

CumulativeReturns = ((1 + StockReturns).cumprod() - 1)

CumulativeReturns[["Portfolio","Portfolio_EW"]].plot()

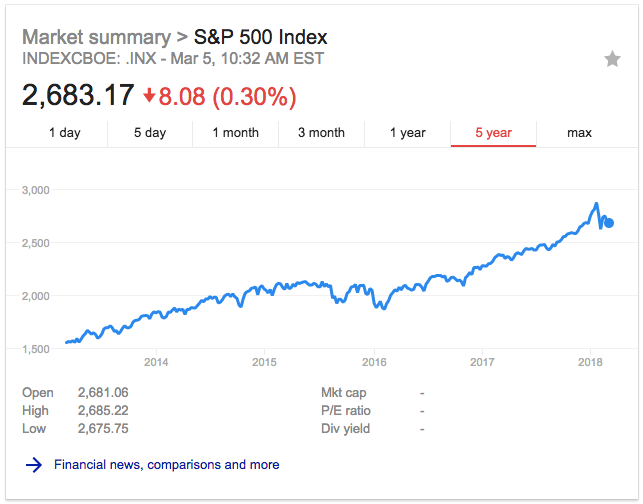

Market capitalization