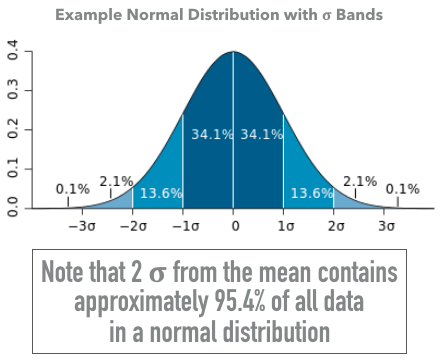

Mean, variance, and normal distribution

Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

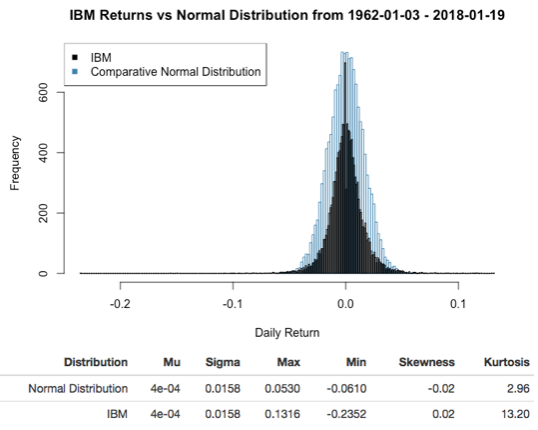

Comparing against a normal distribution

Standard deviation and variance

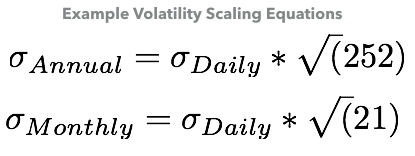

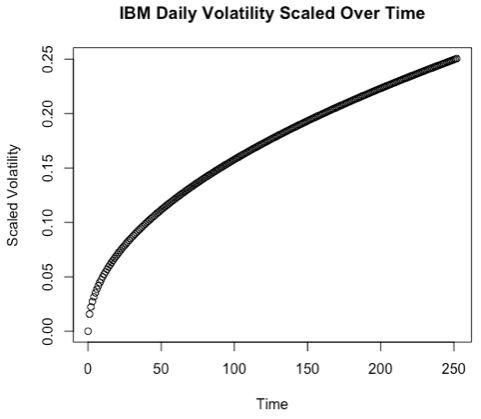

Scaling volatility

- Volatility scales with the square root of time

- You can normally assume 252 trading days in a given year, and 21 trading days in a given month