Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

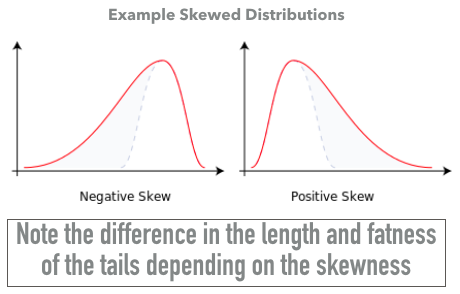

Skewness is the third moment of a distribution.

Negative Skew: The mass of the distribution is concentrated on the right. Usually a right-leaning curve

Positive Skew: The mass of the distribution is concentrated on the left. Usually a left-leaning curve

In finance, you would tend to want positive skewness

Skewness in Python

Assume you have pre-loaded stock returns data in the StockData object.

To calculate the skewness of returns:

from scipy.stats import skew

skew(StockData["Returns"].dropna())

0.225

Note that the skewness is higher than 0 in this example, suggesting non-normality.

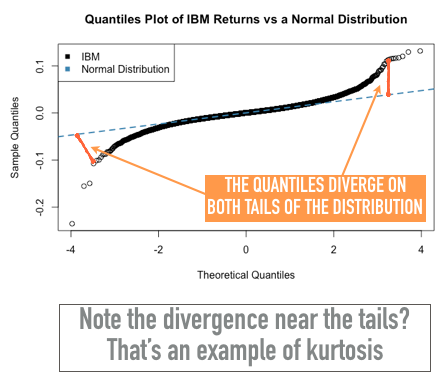

Kurtosis is a measure of the thickness of the tails of a distribution

Most financial returns are leptokurtic

Leptokurtic: When a distribution has positive excess kurtosis (kurtosis greater than 3)

Excess Kurtosis: Subtract 3 from the sample kurtosis to calculate "Excess Kurtosis"

Excess kurtosis in Python

Assume you have pre-loaded stock returns data in the StockData object. To calculate the excess kurtosis of returns:

from scipy.stats import kurtosis

kurtosis(StockData["Returns"].dropna())

2.44

Note the excess kurtosis greater than 0 in this example, suggesting non-normality.

Testing for normality in Python

How do you perform a statistical test for normality?

The null hypothesis of the Shapiro-Wilk test is that the data are normally distributed.

# Run the Shapiro-Wilk normality test in Python

from scipy import stats

p_value = stats.shapiro(StockData["Returns"].dropna())[1]

if p_value <= 0.05:

print("Null hypothesis of normality is rejected.")

else:

print("Null hypothesis of normality is accepted.")

The p-value is the second variable returned in the list. If the p-value is less than 0.05, the null hypothesis is rejected because the data are most likely non-normal.

Let's practice!

Introduction to Portfolio Risk Management in Python