Random walks

Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

Random walks

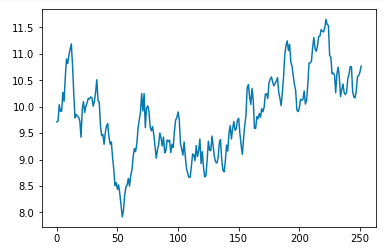

Most often, random walks in finance are rather simple compared to physics:

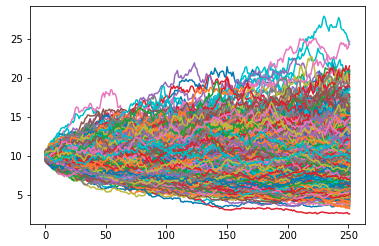

Monte Carlo simulations

A series of Monte Carlo simulations of a single asset starting at stock price $10 at T0. Forecasted for 1 year (252 trading days along the x-axis):