The Capital Asset Pricing Model

Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

Linear regressions

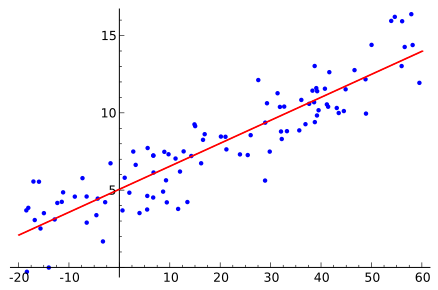

Example of a linear regression:

Regression formula in matrix notation:

Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

Example of a linear regression:

Regression formula in matrix notation: